Invested Capital - Definition, Uses, How To Calculate

Invested capital is the investment made by both shareholders and debtholders in a company. When a company needs capital to expand,| Corporate Finance Institute

Invested capital is the investment made by both shareholders and debtholders in a company. When a company needs capital to expand,| Corporate Finance Institute

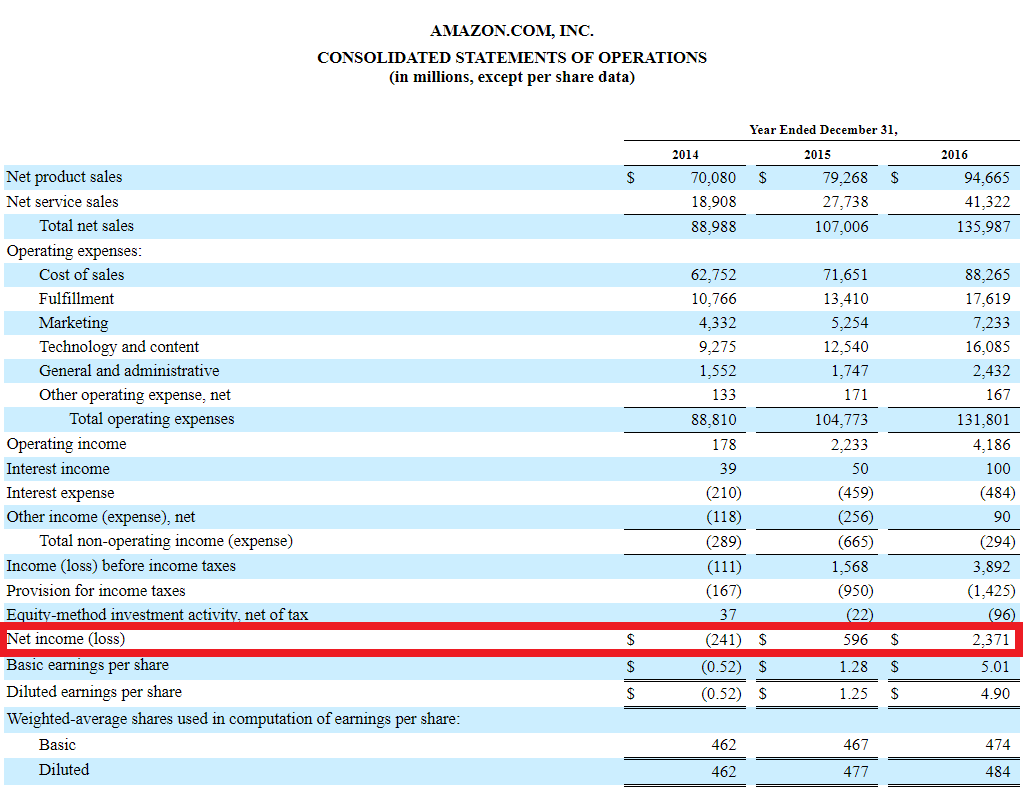

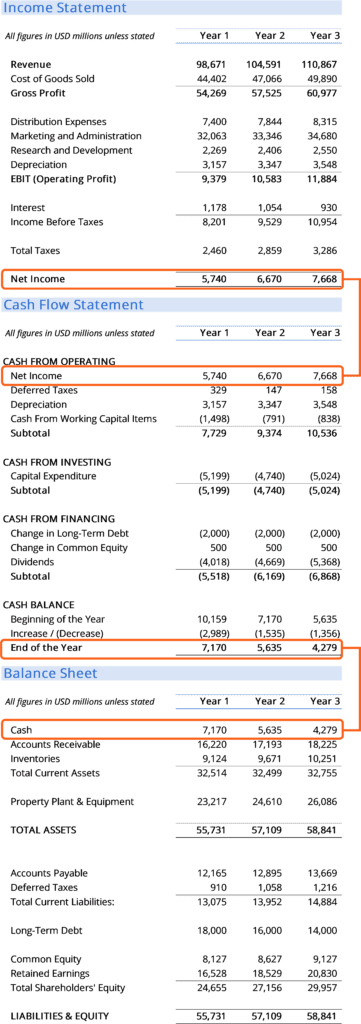

Net Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through| Corporate Finance Institute

Net interest income is defined as the the difference between interest revenues and interest expenses.For financial institutions, interest revenues represent| Corporate Finance Institute

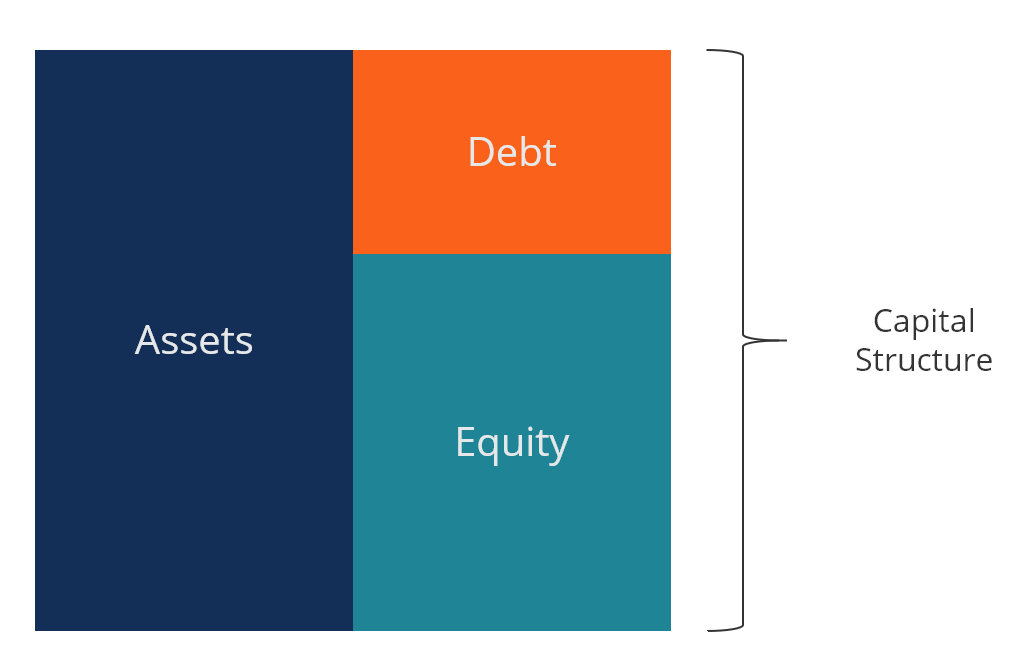

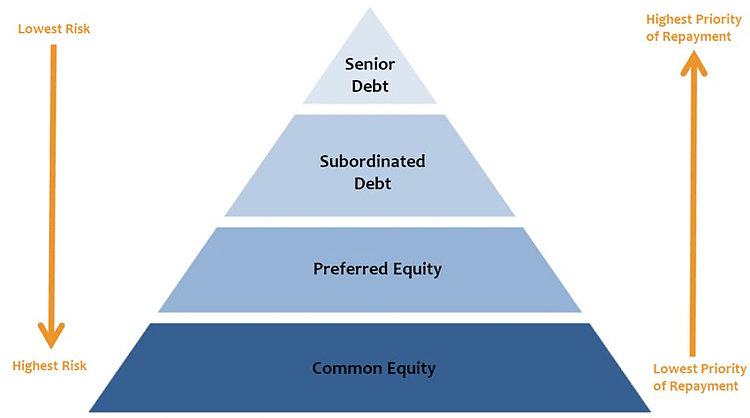

Capital structure refers to the amount of debt and/or equity employed by a firm to fund its operations and finance its assets. A firm's capital structure| Corporate Finance Institute

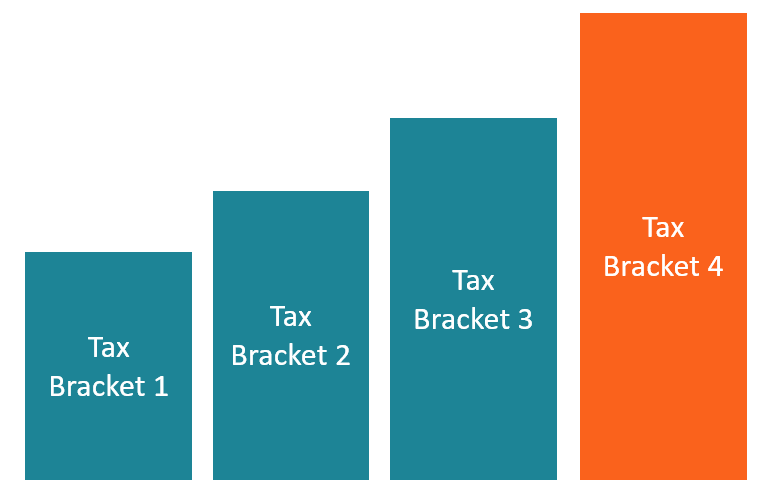

A progressive tax is a tax rate that increases as the taxable value goes up. It is usually segmented into tax brackets that progress to| Corporate Finance Institute

The Annualized Income Installment Method (AIIM) is a method used to calculate the amount of taxes payable by a business during a tax year| Corporate Finance Institute

Lower of cost or market (LCM) is an inventory valuation method required for companies that follow U.S. GAAP. In the lower of cost or market| Corporate Finance Institute

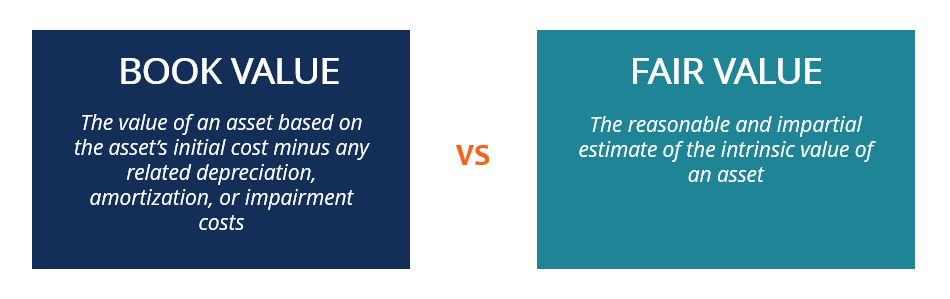

In accounting and finance, it is important to understand the differences between book value vs fair value. Both concepts are used in the| Corporate Finance Institute

Treasury stock, or reacquired stock, is a portion of previously issued, outstanding shares of stock that a company repurchased from shareholders.| Corporate Finance Institute

Senior term debt is a loan with a priority repayment status in case of bankruptcy, and typically carries lower interest rates and lower risk.| Corporate Finance Institute

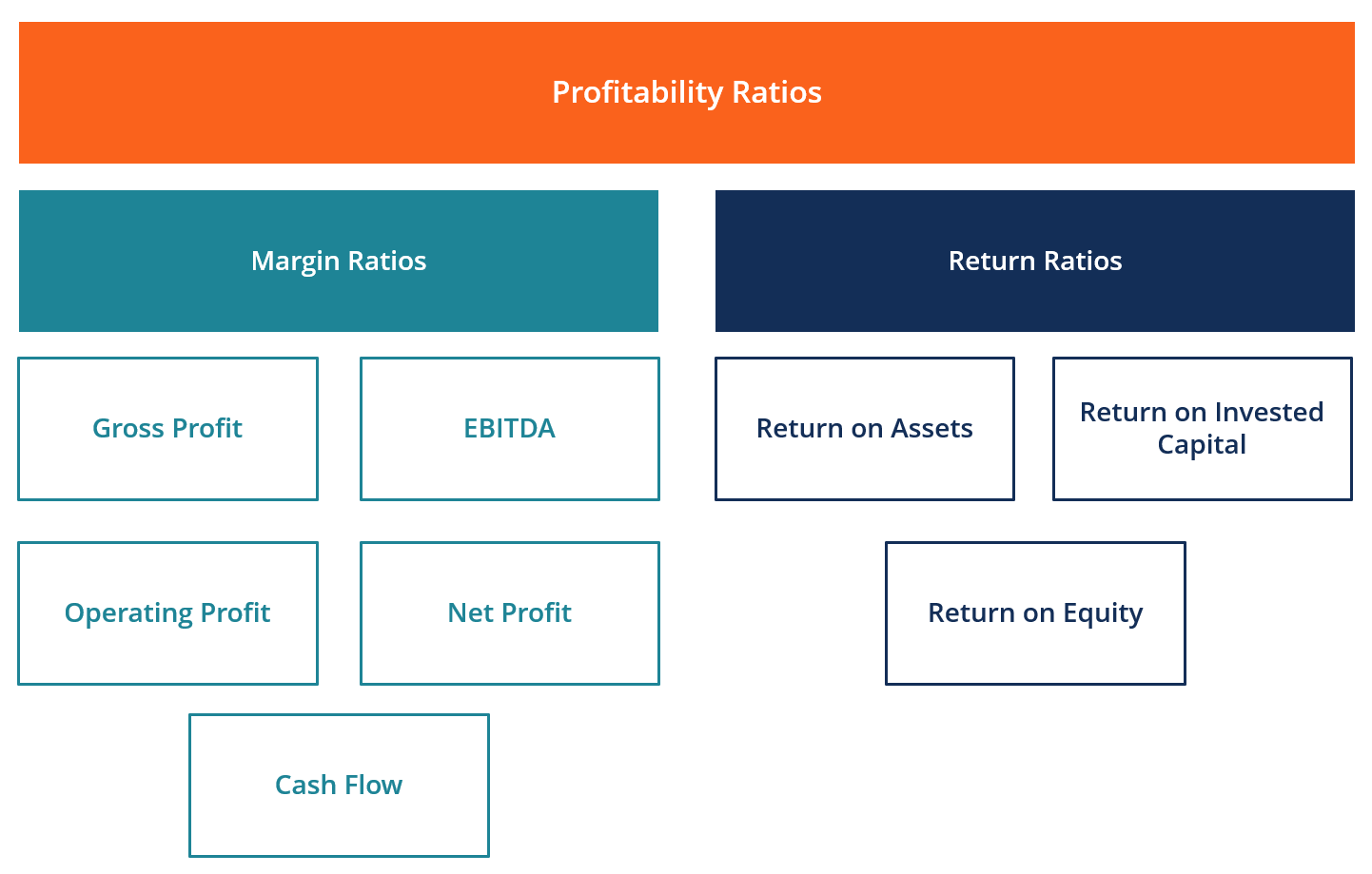

Explore key profitability ratios—learn how to assess a company's ability to generate income relative to revenue, assets, and equity for financial analysis.| Corporate Finance Institute

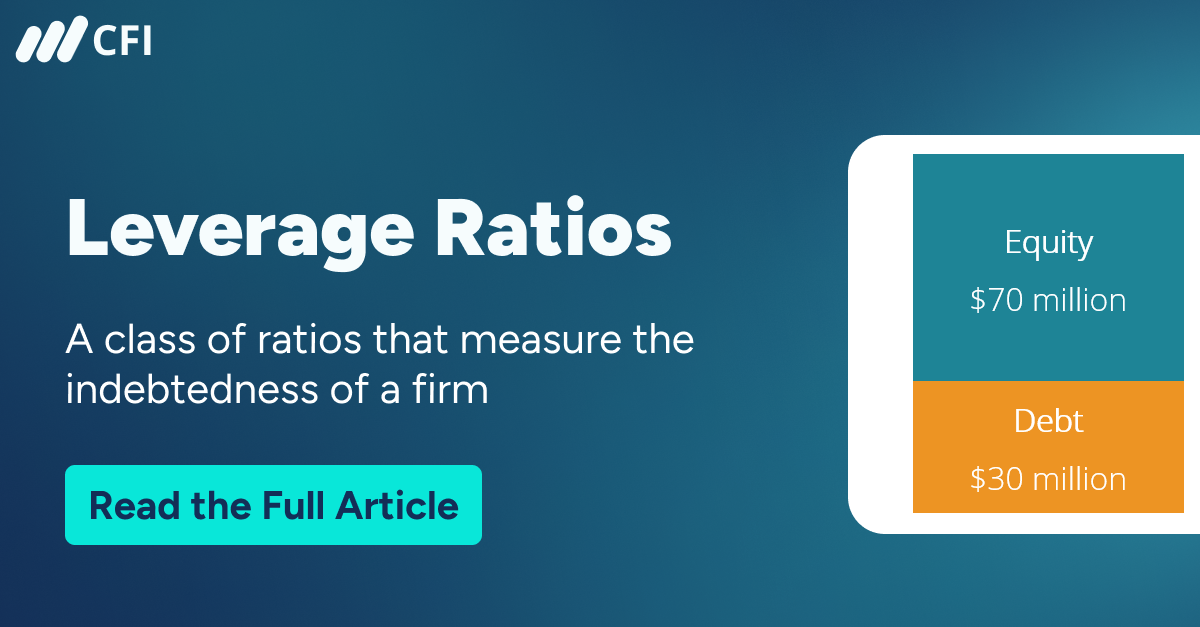

A leverage ratio indicates the level of debt incurred by a business entity against several other accounts in its balance sheet, income statement, or cash flow statement.| Corporate Finance Institute

Contributed surplus is an account in the shareholders’ equity section of the balance sheet that reflects excess amounts collected from the| Corporate Finance Institute

The key difference between additional paid-in capital vs. contributed capital is that the latter is referred to as the total value of cash| Corporate Finance Institute

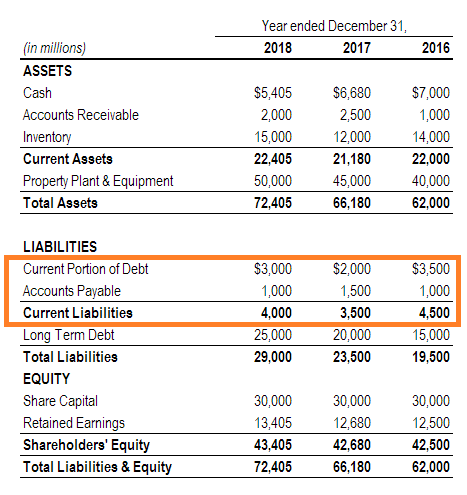

Current liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the| Corporate Finance Institute

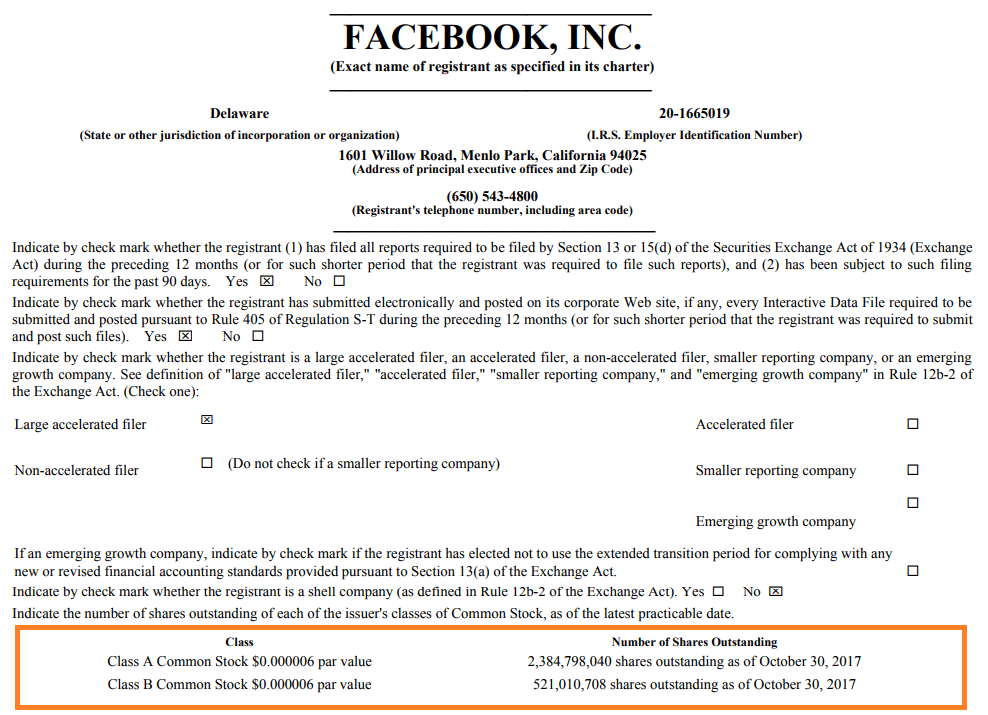

Share capital (shareholders' capital, equity capital, contributed capital, or paid-in capital) is the amount invested by a company’s| Corporate Finance Institute

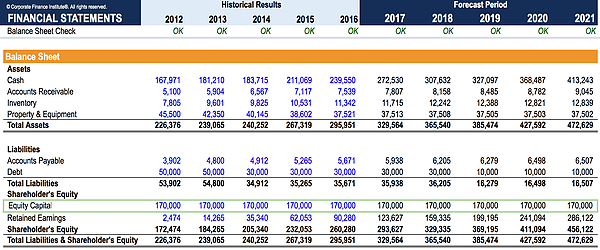

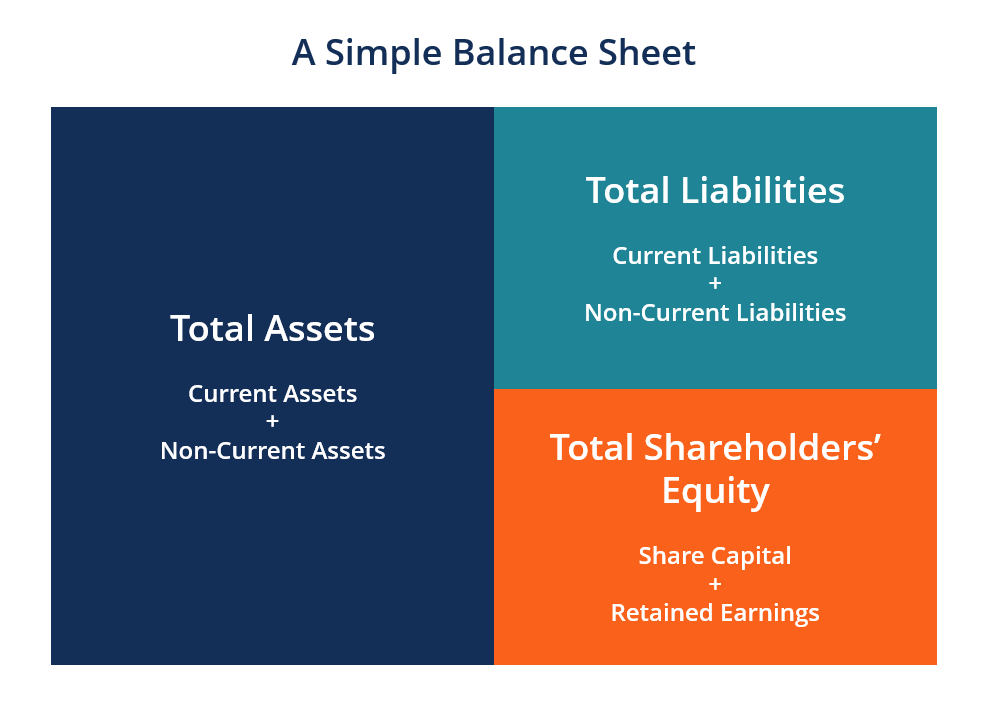

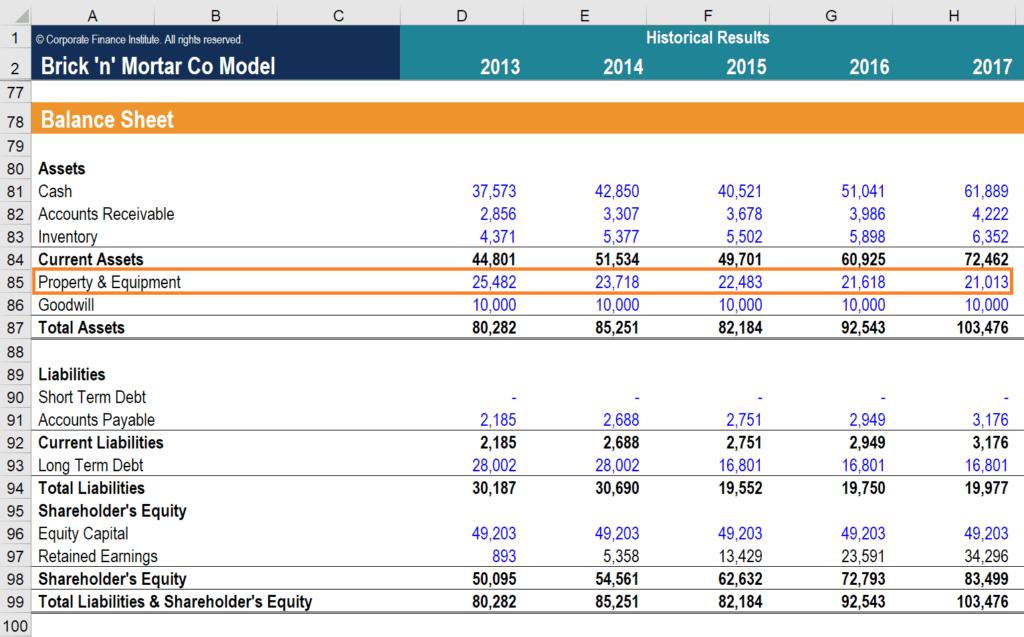

The balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting.| Corporate Finance Institute

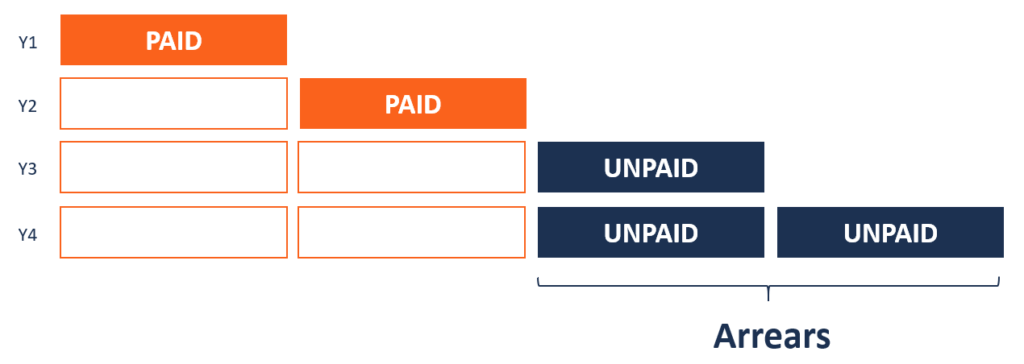

Arrears refers to payments that are overdue and that are supposed to be made at the end of a given period after missing out on the required payments.| Corporate Finance Institute

Common types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and| Corporate Finance Institute

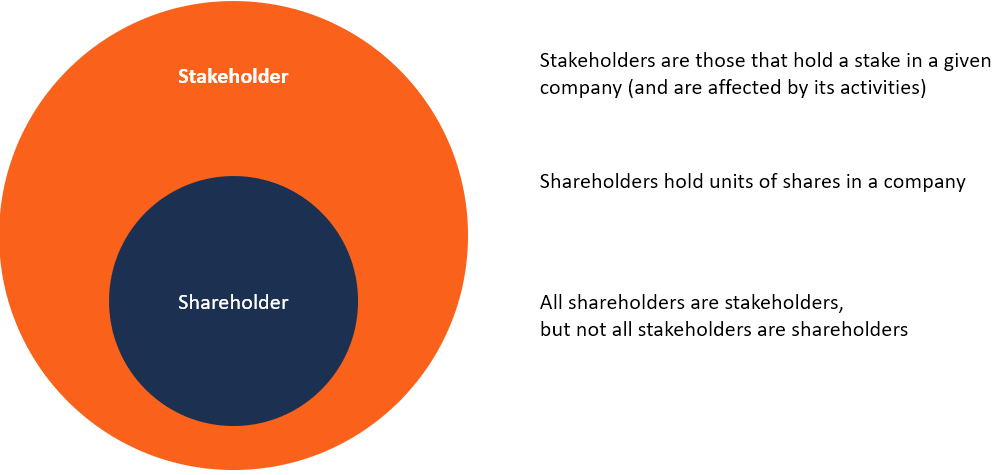

Generally, a shareholder is a stakeholder of the company, while a stakeholder is not necessarily a shareholder.| Corporate Finance Institute

Explore CFI's free resource library of Excel templates, interview prep, and deep dives into the topics you need to know for a career in finance and banking.| Corporate Finance Institute

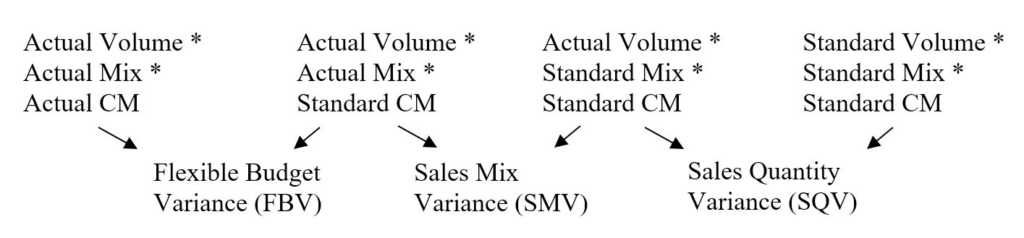

Revenue Variance Analysis is used to measure differences between actual sales and expected sales, based on sales volume metrics, sales mix| Corporate Finance Institute

Quarterly revenue growth refers to an increase in the company's sales from one quarter to the next. The sales figure for the current quarter| Corporate Finance Institute

Proceeds refer to the cash received from the sale of goods or assets during a particular period. The total is obtained by multiplying the quantities sold by the| Corporate Finance Institute

Ancillary revenue is income a company generates from selling goods and services that are not a primary revenue stream or core business| Corporate Finance Institute

Return on Investment (ROI) is a performance measure used to evaluate the returns of an investment or compare efficiency of different investments.| Corporate Finance Institute

Return on Invested Capital (ROIC) is a profitability or performance measure of the return earned by those who provide capital, i.e., bondholders and stockholders.| Corporate Finance Institute

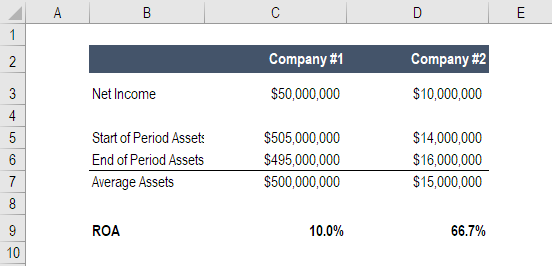

ROA Formula. Return on Assets (ROA) is a type of return on investment (ROI) metric that measures the profitability of a business in relation to its total assets.| Corporate Finance Institute

The treasury stock method is a way for companies to compute the number of additional shares that can possibly be created by un-exercised,| Corporate Finance Institute

Taxable income refers to any individual's or business’ compensation that is used to determine tax liability.| Corporate Finance Institute

The fair market value (of a good or service being exchanged) refers to the price at which both transacting parties agreed to independently.| Corporate Finance Institute

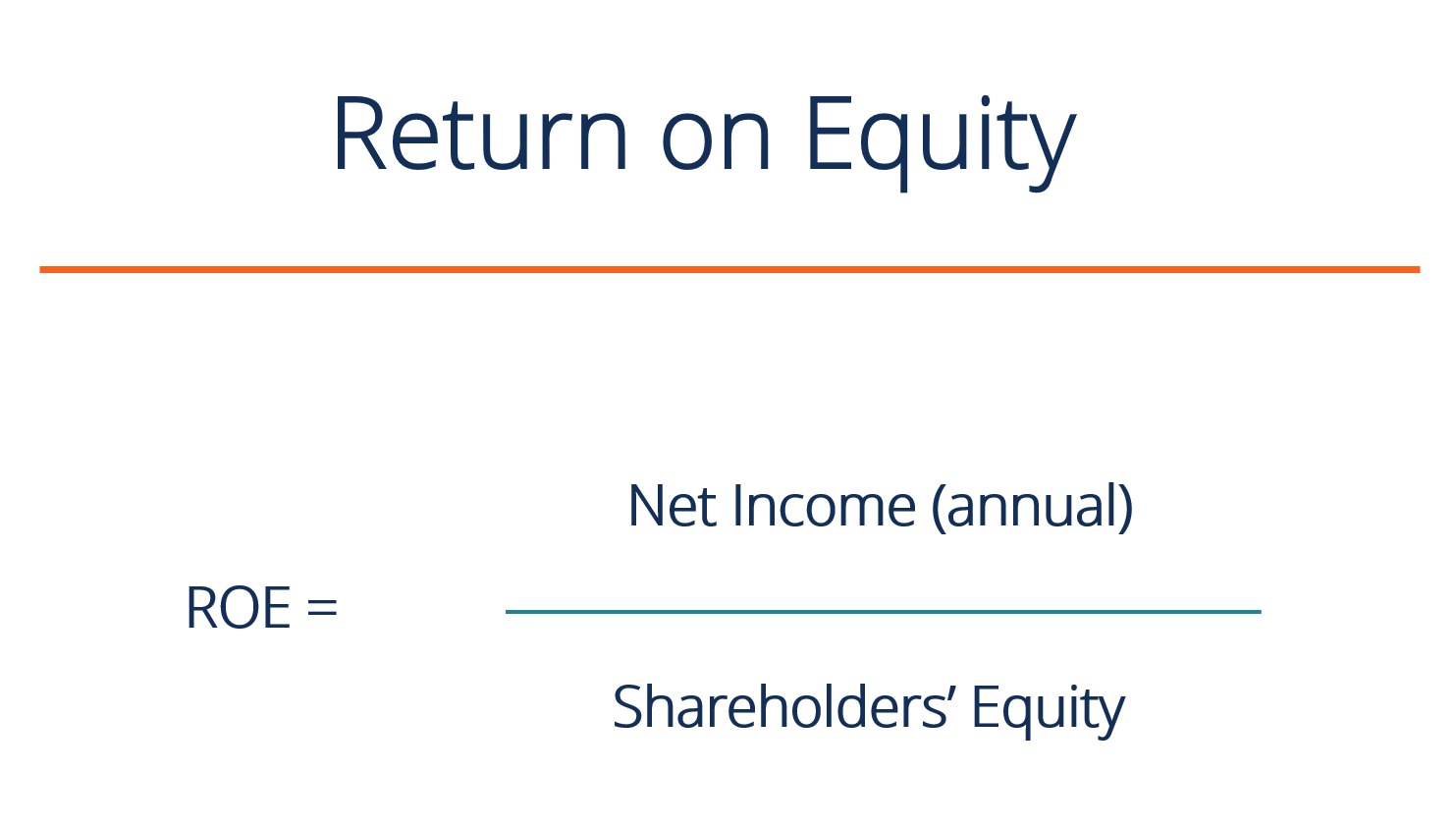

Return on Equity (ROE) is a measure of a company’s profitability that takes a company’s annual return (net income) divided by the value of its total shareholders' equity.| Corporate Finance Institute

Senior Debt is money owed by a company that has first claims on the company’s cash flows. It is more secure than any other debt, such as subordinated debt| Corporate Finance Institute

Par Value is the nominal or face value of a bond, or stock, or coupon as indicated on a bond or stock certificate. It is a static value| Corporate Finance Institute

A subsidiary (sub) is a business entity or corporation that is fully owned or partially controlled by another company, termed as the parent, or holding, company.| Corporate Finance Institute

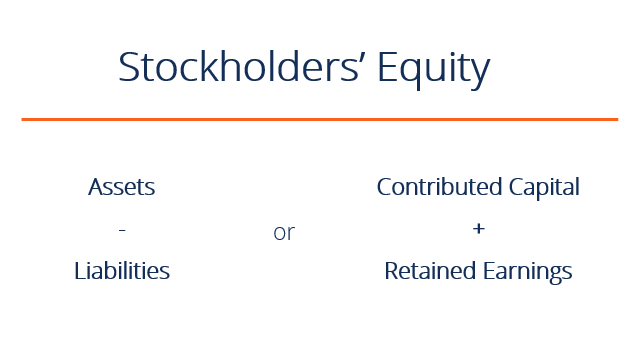

Stockholders Equity (also known as Shareholders Equity) is an account on a company's balance sheet that consists of share capital plus| Corporate Finance Institute

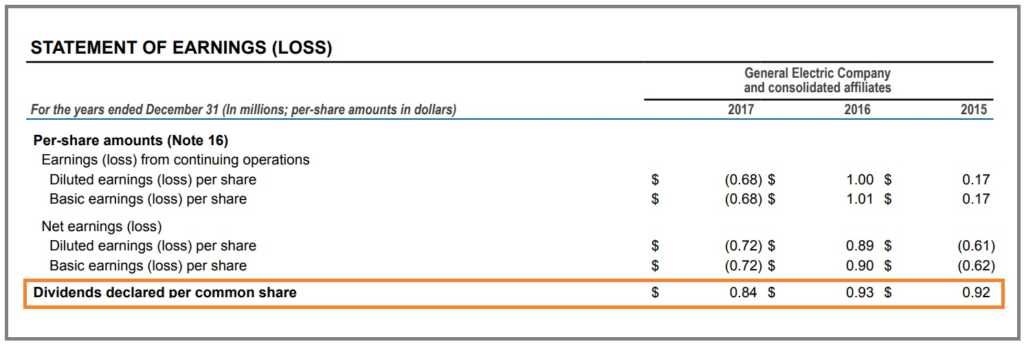

Discover what dividends are, how they work, and their impact on valuation. Learn about different types of dividends and explore real-world examples.| Corporate Finance Institute

Net Profit Margin is a financial ratio used to calculate the percentage of profit a company produces from its total revenue.| Corporate Finance Institute

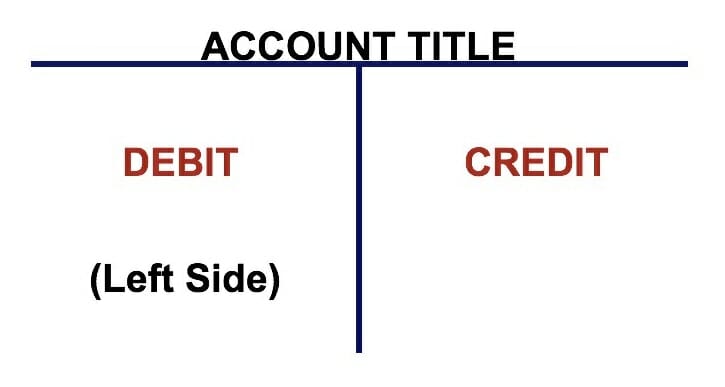

If you want a career in accounting, T Accounts may be your new best friend. The T Account is a visual representation of individual accounts| Corporate Finance Institute

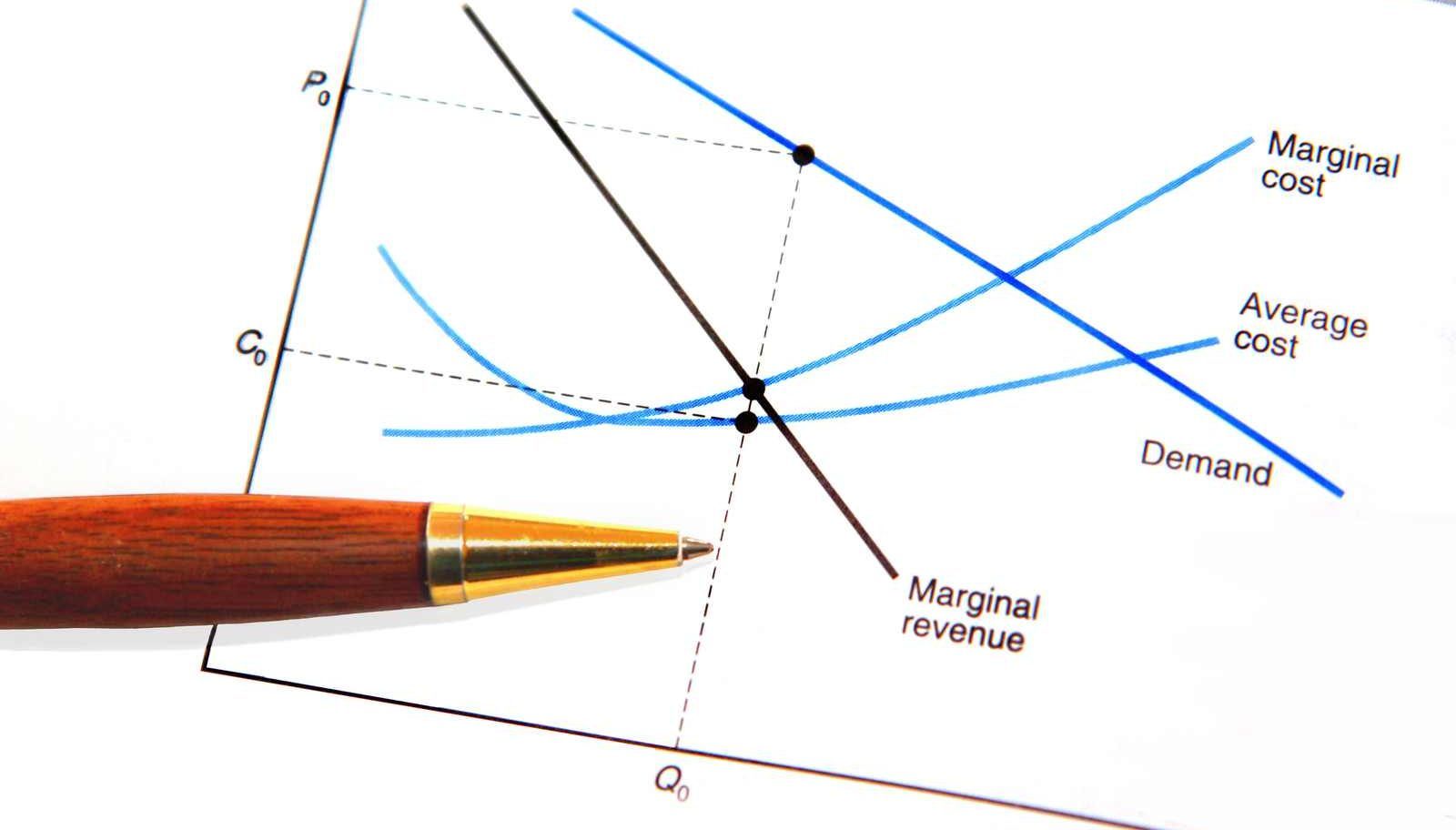

The marginal cost formula represents the incremental costs incurred when producing additional units of a good or service. The marginal cost| Corporate Finance Institute

Absorption costing is a costing system that is used in valuing inventory. It not only includes the cost of materials and labor, but also both| Corporate Finance Institute

Job order costing is used to allocate costs based on a specific job order. This guide provides the job order costing formula and how to calculate it.| Corporate Finance Institute

Activity-based costing is a more specific way of allocating overhead costs based on “activities” that actually contribute to overhead costs.| Corporate Finance Institute

Marketable securities are unrestricted short-term financial instruments that are issued either for equity securities or debt securities of a publicly listed company.| Corporate Finance Institute

A corporation is a legal entity created by individuals, stockholders, or shareholders, with the purpose of operating for profit. Corporations are allowed to enter| Corporate Finance Institute

Interest income is the amount paid to an entity for lending its money or letting another entity use its funds.| Corporate Finance Institute

Sales revenue is income received from sales of goods or services. In accounting, the terms “sales” and “revenue” are often used interchangeably.| Corporate Finance Institute

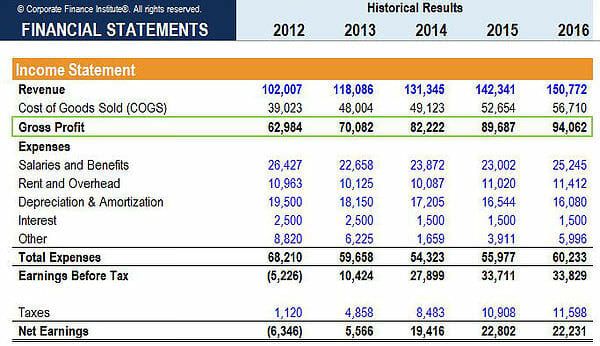

Gross profit is the direct profit left over after deducting the cost of goods sold, or cost of sales, from sales revenue. It's used to calculate the gross profit margin.| Corporate Finance Institute

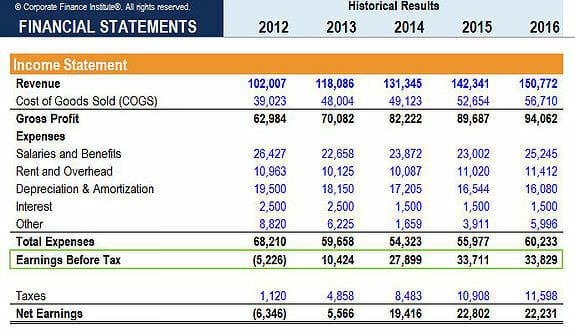

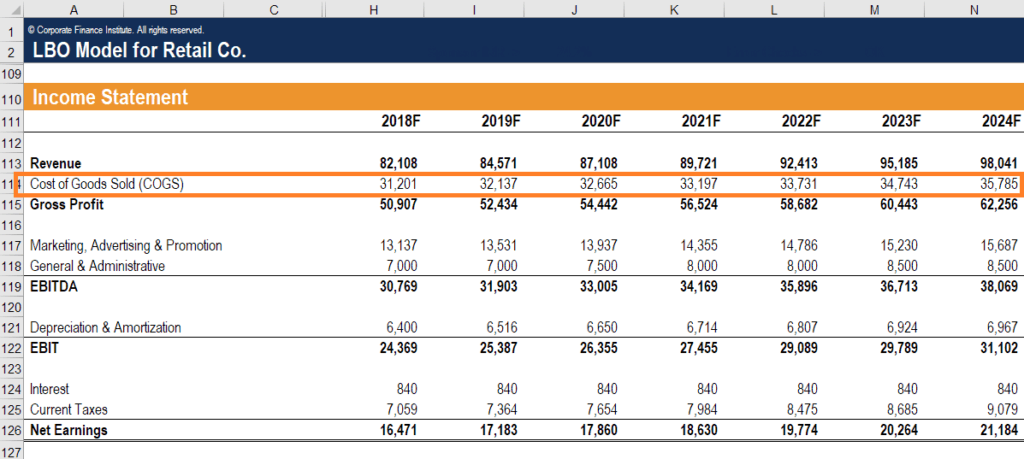

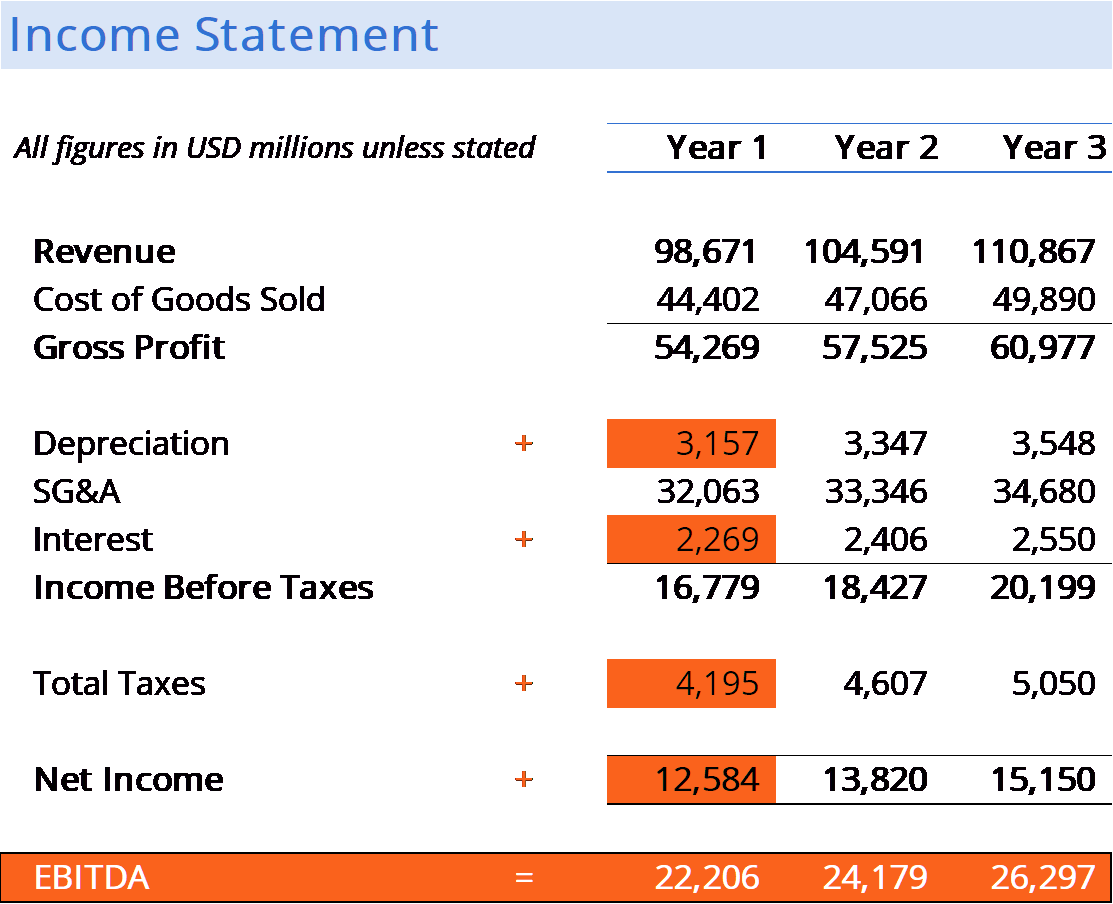

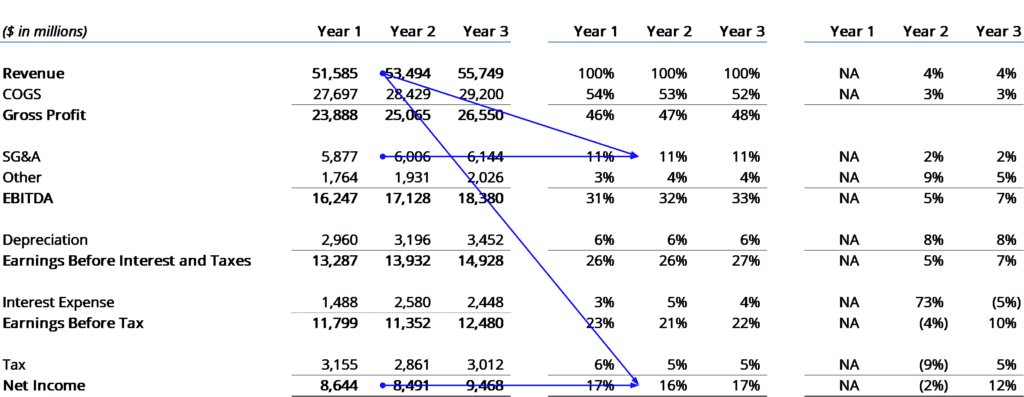

Earnings before tax, or pre-tax income, is the last subtotal found in the income statement before the net income line item. EBT is found| Corporate Finance Institute

The three financial statements are the income statement, the balance sheet, and the statement of cash flows. See them explained in detail.| Corporate Finance Institute

Journal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits)| Corporate Finance Institute

Gross means the total or whole amount of something, whereas net means what remains from the whole after certain deductions are made. This guide will compare gross vs net| Corporate Finance Institute

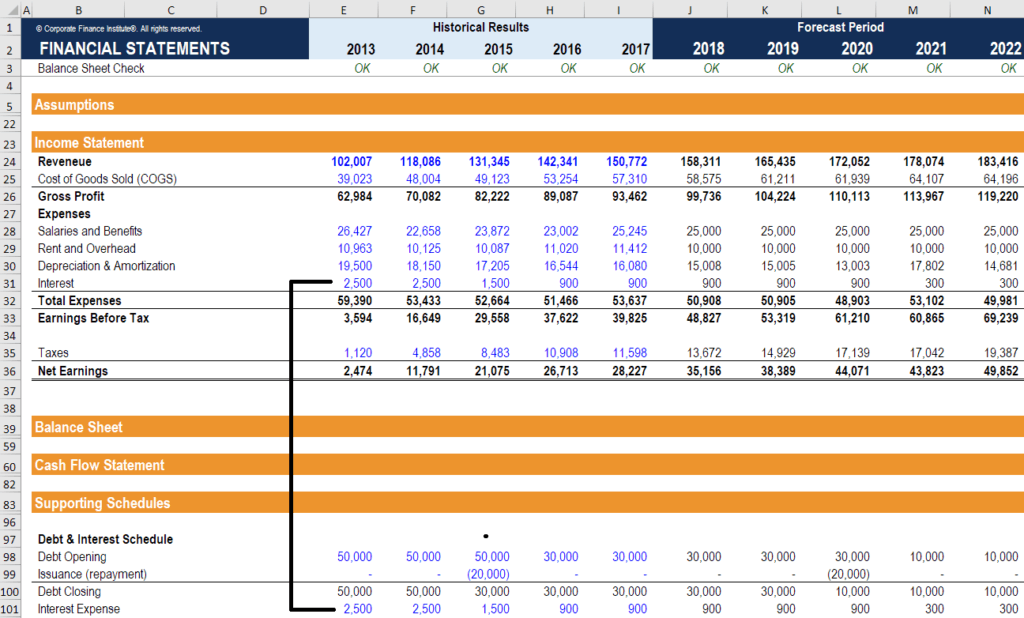

How are the 3 financial statements linked together? We explain how to link the 3 financial statements together for financial modeling and| Corporate Finance Institute

Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total| Corporate Finance Institute

Accounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow| Corporate Finance Institute

Interest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also| Corporate Finance Institute

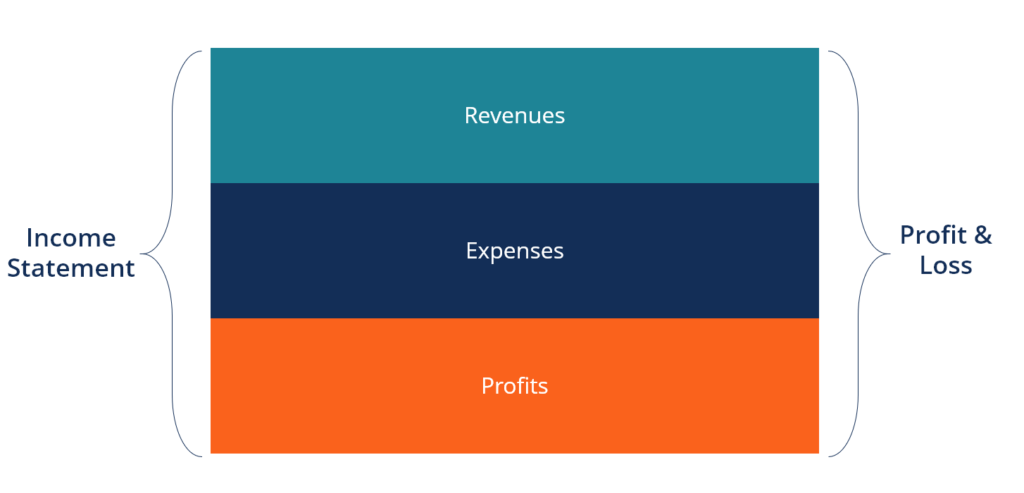

The Income Statement is one of a company's core financial statements that shows its profit and loss over a period of time.| Corporate Finance Institute

PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,| Corporate Finance Institute

Corporate structure refers to the organization of different departments or business units within a company. Depending on a company’s goals and the industry| Corporate Finance Institute

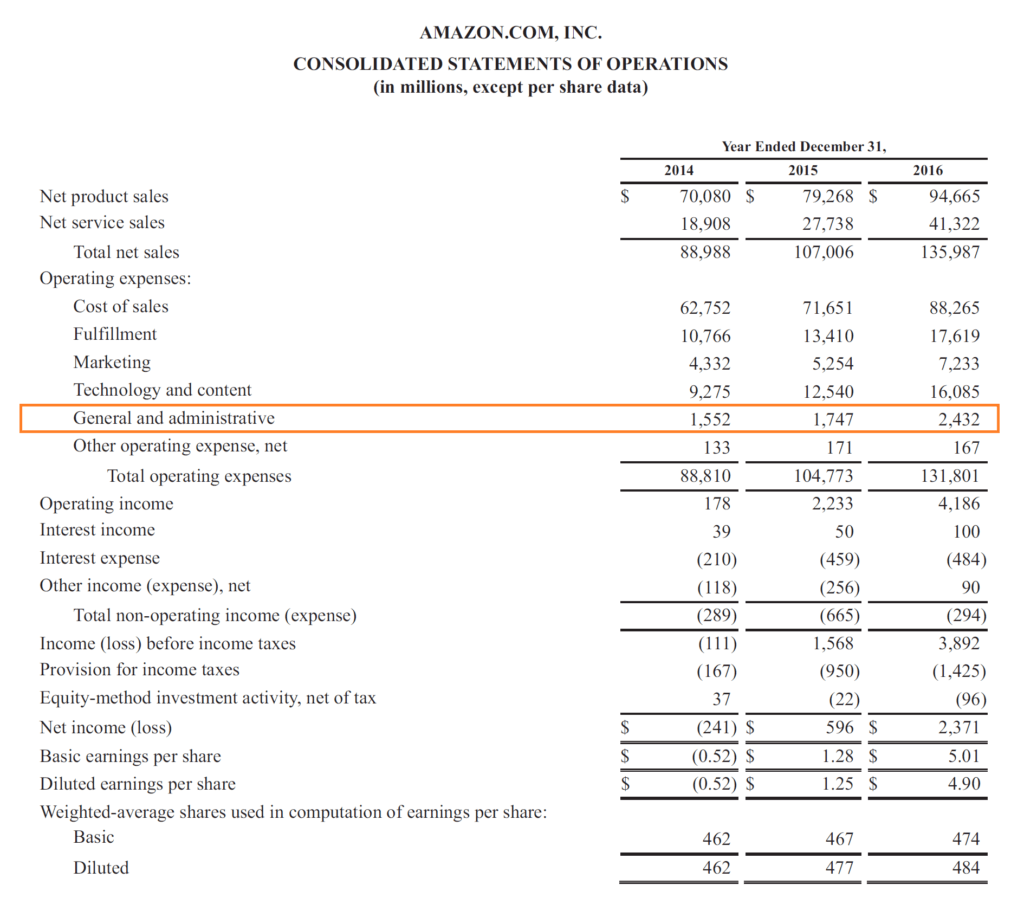

SG&A includes all non-production expenses incurred by a company in any given period. It includes expenses such as rent, advertising, marketing| Corporate Finance Institute

IFRS Standards consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements.| Corporate Finance Institute

Financial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will| Corporate Finance Institute

Cost of Goods Sold (COGS) measures the direct cost incurred in the production of any goods or services. It includes material cost, direct| Corporate Finance Institute

EBITDA or Earnings Before Interest, Tax, Depreciation, Amortization is a company's profits before any of these net deductions are made.| Corporate Finance Institute

Cash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. It is used to describe the amount of cash (currency).| Corporate Finance Institute

Explore cash equivalents, their examples, role in working capital and importance in financial modeling for accurate liquidity analysis and valuation.| Corporate Finance Institute

The revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a company's| Corporate Finance Institute

Learn the essentials of analyzing financial statements to understand a company's financial health. Discover key metrics, methods, and best practices.| Corporate Finance Institute

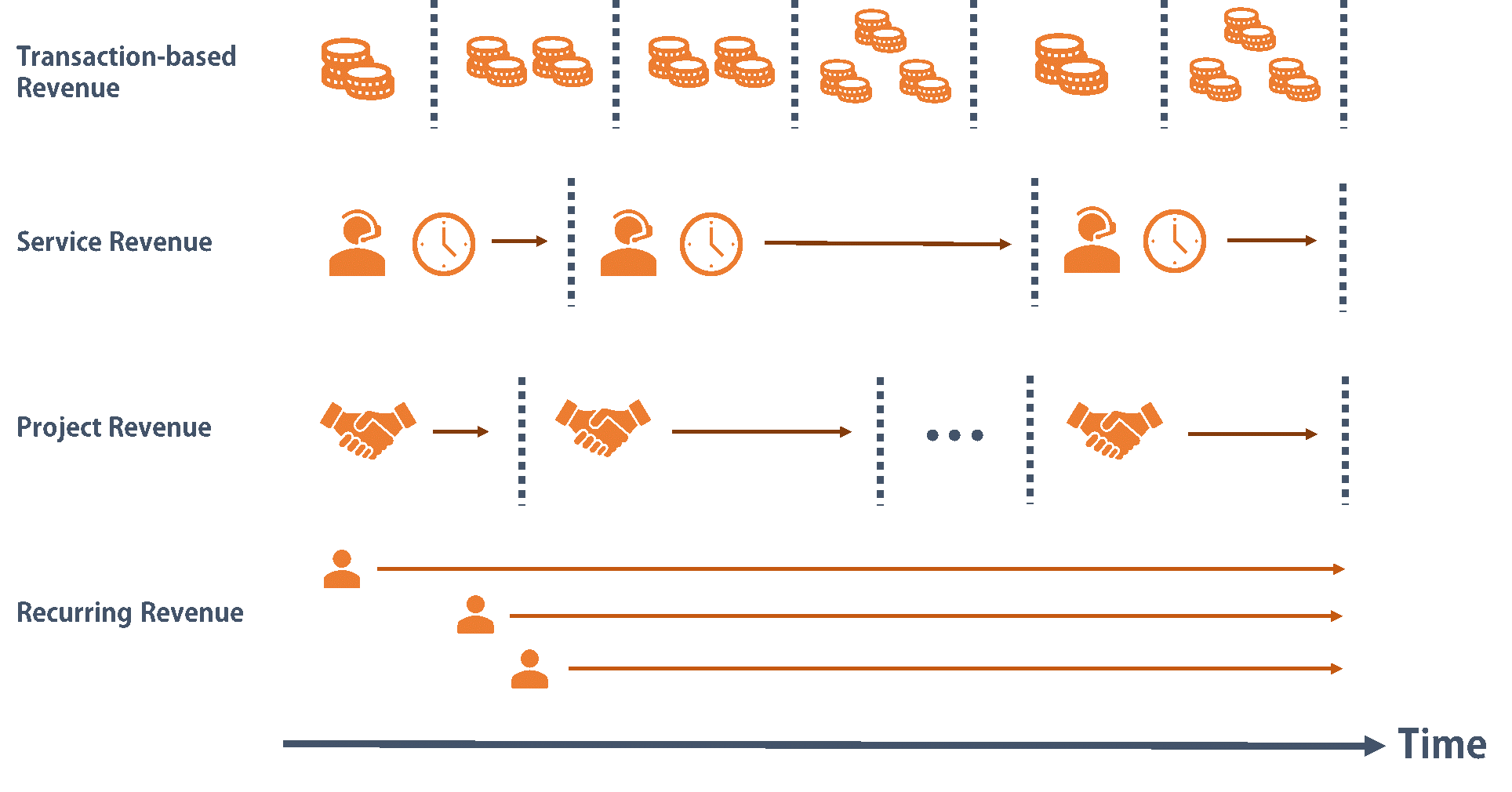

Revenue Streams are the various sources from which a business earns money from the sale of goods or provision of services. The types of| Corporate Finance Institute

The last two decades saw some of the worst accounting scandals in history. Billions of dollars were lost as a result of these financial disasters.| Corporate Finance Institute