Are you curious about how investing taxes are calculated on capital gains, dividends, and interest in Canada? I’m not a tax expert, but with tax loss harvesting season coming out, I figured it might be a good time to review some of the basics between how Canadian investment returns are taxed in your RRSP, TFSA, and non-registered accounts. Investing Taxes in an RRSP Let’s start with RRSPs. As you probably know, RRSP contributions and investment growth are taxable only upon withdrawal. A...| Million Dollar Journey

After writing a deep dive article on whether the 4% safe withdrawal rate still works for retirement at various ages, I received a lot of questions basically asking: “Ok, so 4% is a good rule of thumb, but when I actually go to withdraw money from my various investment accounts, to put into my chequing account & high interest savings account in order to pay for day-to-day expenses, what is the best way to avoid taxes?” Upon reading many of these types of questions, I realized that I wasn...| Million Dollar Journey

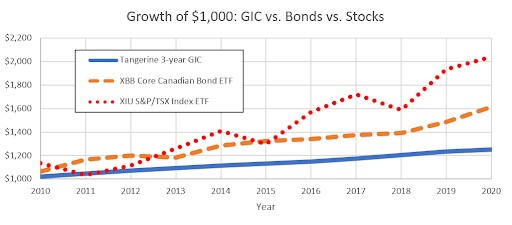

Most Canadians never stop to consider when low risk investments are the most appropriate use of savings versus when higher-risk long-term investments are the better route. The truth is that most Canadians choose their investment by “gut feel.” You likely don’t need me to tell you, that’s not an ideal process. When choosing between higher risk and low risk investments, it’s important to consider your personal goals and risk tolerance. Personally, I think that if you need your money i...| Million Dollar Journey

Long-term investing is one of the most powerful ways to grow your wealth. As the name implies, long-term investing means that an investor buys an asset with the intent to hold it for some time. The time frame can be years or even decades. Over time, long-term investing has the potential to produce excellent returns due to the magic of compound interest. While this strategy might not appeal to everyone, especially those with a high risk tolerance, it has historically proven to be an effectiv...| Million Dollar Journey

Because I’ve written a lot about the Best Canadian ETFs and the top dividend ETFs, I tend to get a lot of questions and comments asking me about the MER and taxes on ETFs that hold equities from other countries. Obviously when you’re asking those types of in-depth questions you already understand the value of index investing, and instant diversification. Personally, I like to balance my love of Canadian dividend stocks, with non-Canadian ETFs to get super-convenient international exposure...| Million Dollar Journey

Given the realities of skyrocketing interest rates it’s no wonder that interest in Canada’s Best Cash ETFs, high interest savings account (HISA ETFs), and money market ETFs has significantly increased as well. While Cash ETFs aren’t exactly the same thing as money market ETFs, the two are very similar. The terms high interest savings account ETF and Cash ETF on the other hand, mean exactly the same thing. While cash ETFs are a solid investment (more on that below), you really need to c...| Million Dollar Journey

The best short term investments in Canada continue to reward GIC customers, as well as those interested in the new EQ Notice Account. It’s tough to beat a zero-risk guaranteed 3.65%+ return on your cash! Of course GICs aren’t the only safe, short term investment option in Canada. If you can’t stomach putting your money away for a full year to make use of a GIC, then Canada’s best high interest savings accounts are where you would want to look. So, what makes a short term investment d...| Million Dollar Journey

Is now the time to lock in Canada’s Best GIC Rates? With the Bank of Canada suggesting a potential rate cuts in 2025, and with Trump’s tariffs knocking on the door, the best GIC rates in Canada may be hovering at their peak -which could mean now’s a great time to snag something above 3.3%. A Guaranteed Investment Certificate (GIC) is essentially the Canadian counterpart to an American CD (Certificate of Deposit), offering a stable way to grow your money. GICs shine when you’re aiming ...| Million Dollar Journey

EQ Bank Account Options and Interest Rates Account TypeInterest RateBest ForDaily High Interest Account1.25%* (Plus 2.75% if you direct deposit your pay)People who want the highest consistent interest rate in Canada + free e-transfers + super cheap international money conversion + FREE BANKING + USD Accounts for Canadians EQ GICs2.60% - 3.60%Folks looking to get a high ultra-safe return EQ TFSA Account3.60%The highest guaranteed rate of return in a TFSA in Canada.EQ RRSP Account3.60%The hig...| Million Dollar Journey