Flat Tax Revolution: State Income Tax Reform | Tax Foundation

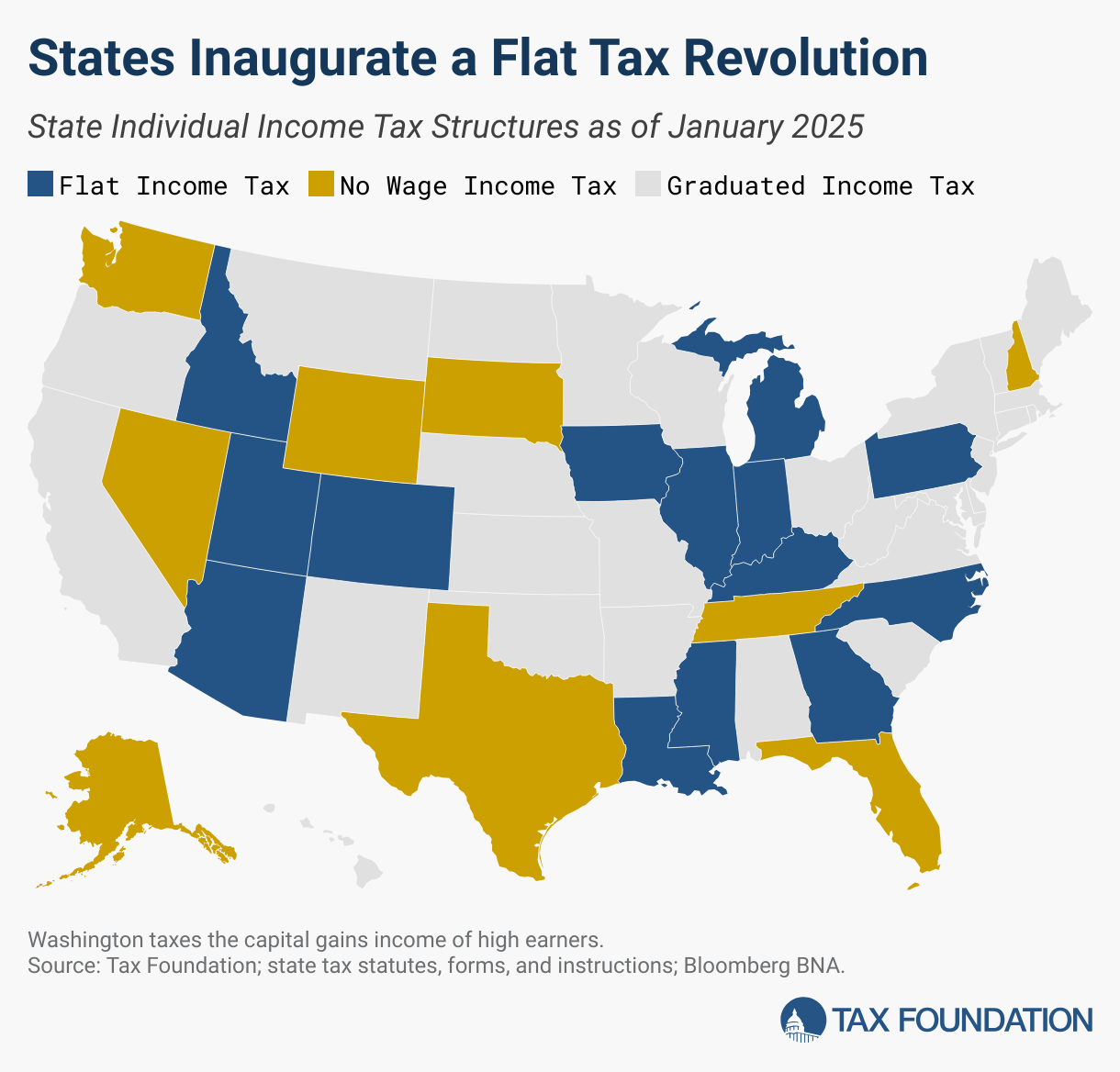

The past four years have brought significant focus on state income tax reform and relief, and with that, something of a flat tax revolution.| Tax Foundation

The past four years have brought significant focus on state income tax reform and relief, and with that, something of a flat tax revolution.| Tax Foundation

The One Big Beautiful Bill Act (OBBBA) significantly alters the Inflation Reduction Act (IRA) green energy subsidies.| Tax Foundation

Despite the potential of consumption taxes as a neutral and efficient source of tax revenues, many governments have implemented policies that are unduly complex and have poorly designed tax bases that exclude many goods or services from taxation, or tax them at reduced rates.| Tax Foundation

Backfilling forgone local property tax revenue through new state taxes is difficult because it dramatically shifts overall tax burdens, undermines local accountability, and cannot easily adjust for changing population mixes.| Tax Foundation

Universal savings accounts could be a simpler solution to many countries’ systems of private retirement savings investment tax treatment.| Tax Foundation

The US Supreme Court will hear oral arguments on November 5, to determine whether the President’s emergency powers under the International Emergency Economic Powers Act (IEEPA) include the power to impose tariffs.| Tax Foundation

A tax refund is a reimbursement to taxpayers who have overpaid their taxes, often due to having employers withhold too much from paychecks. The U.S. Treasury estimates that nearly three-fourths of taxpayers are over-withheld, resulting in tax refunds. Overpaying taxes can be viewed as an interest-free loan to the government.| Tax Foundation

The Earned Income Tax Credit (EITC) is a refundable tax credit targeted at low-income workers. Learn more about the EITC and Child Tax Credit.| Tax Foundation

Wireless consumers continue to be burdened with high taxes, fees, and government surcharges in many states and localities throughout the country.| Tax Foundation

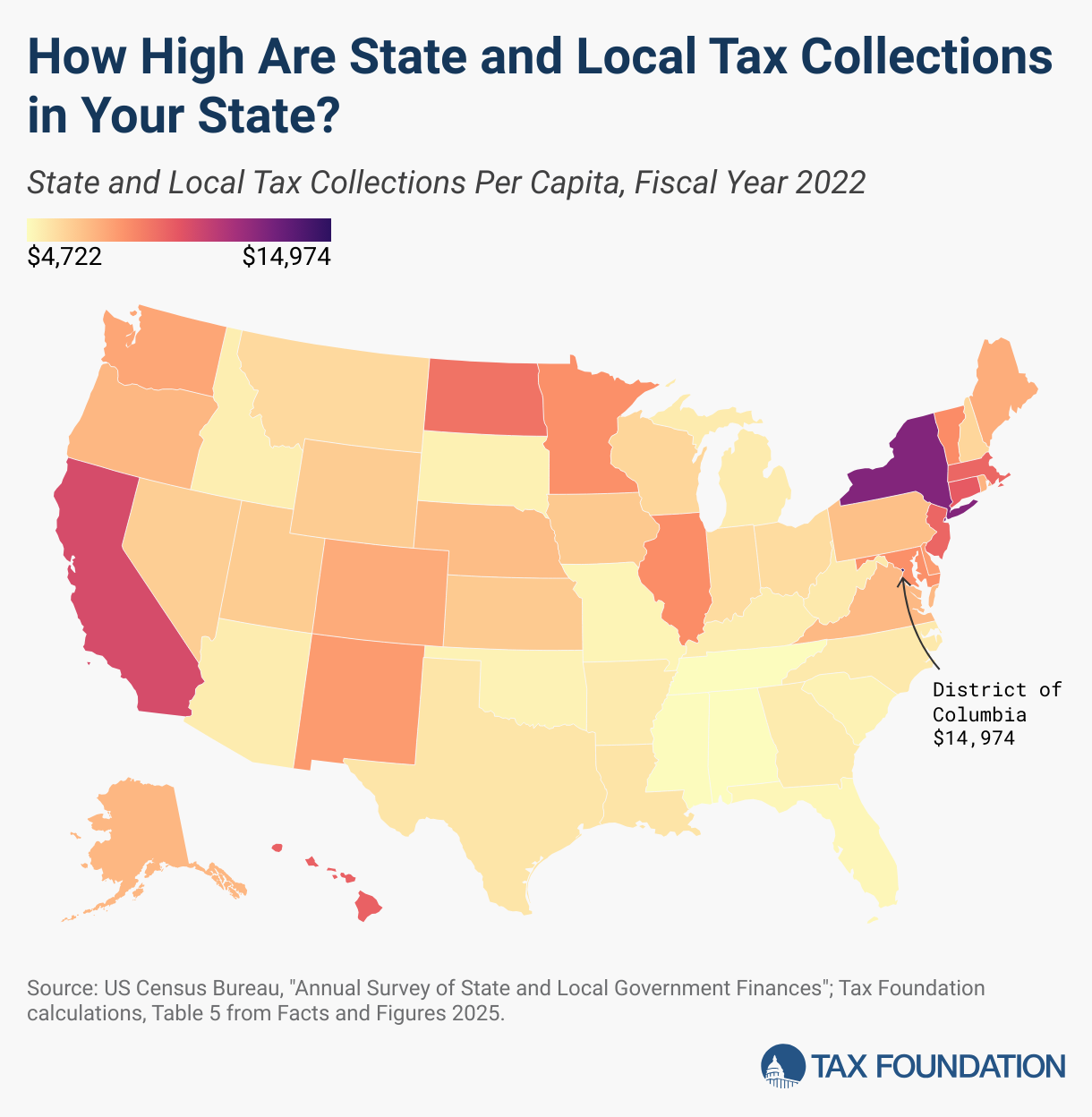

According to the latest economic data from the US Census Bureau, the average per capita state and local tax burden is $7,109. However, collections vary widely by state, reflecting differences in tax rates and bases, natural resource endowments, the scale and scope of taxable economic activity in each state, and residents’ political preferences.| Tax Foundation

The US fiscal trajectory is on an unsustainable path over the next 35 years, regardless of whether the IEEPA tariffs are struck down or maintained.| Tax Foundation

Football players facing off in Brazil will owe an estimated $1.04 million in nonresident income tax on the share of income they earned there.| Tax Foundation

Republican policymakers in Congress are considering options to raise revenue as part of their expected legislative package in 2025. One such option involves raising the tax rate on university endowments first put in place as part of the TCJA in 2017.| Tax Foundation

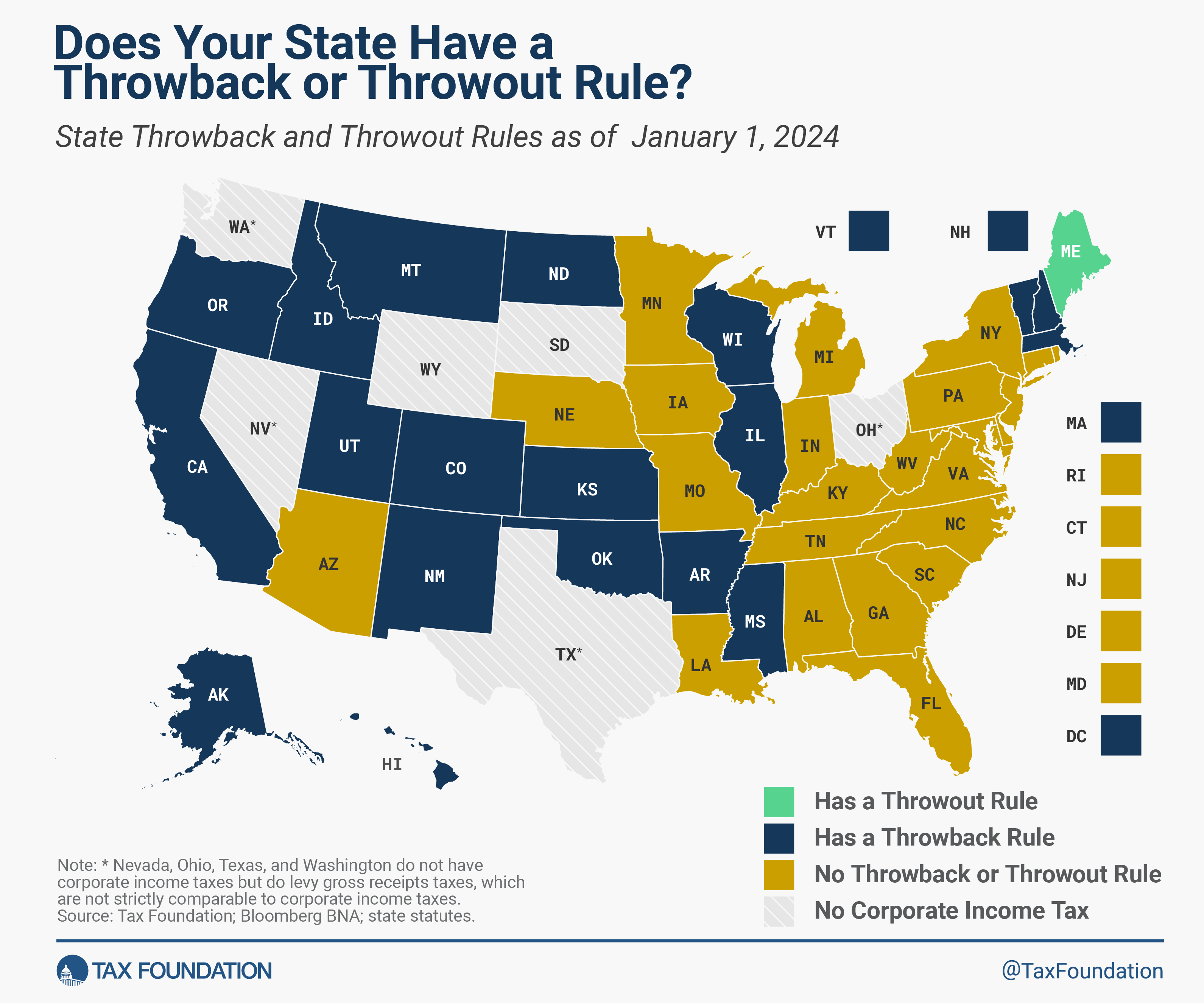

States have generally tried to encourage capital investment. Throwback and throwout rules are an unfortunate example of penalizing it.| Tax Foundation

Individual income taxes are a major source of state government revenue, accounting for more than a third of state tax collections. How do income taxes compare in your state?| Tax Foundation

With state tax revenues receding from all-time highs, there’s been a great deal of handwringing about whether states can afford the tax cuts adopted over the past few years. Given that 27 states reduced the rate of a major tax between 2021 and 2023, is there reason for concern?| Tax Foundation

Former President Donald Trump would like to push for a reduction in the federal corporate tax rate from 21 percent to 15 percent if reelected.| Tax Foundation

In a surprising tax code alteration that has frustrated Americans who enjoy gambling, a provision in the One Big Beautiful Bill Act limits gambling losses that can be used to offset gambling winnings to 90 percent of their value. This provision introduces a steep tax penalty for professional gamblers and certain casual bettors.| Tax Foundation

Gross receipts taxes, by their very design, lack transparency. Our report explores the pros and cons of a turnover tax, also known as a gross receipts tax.| Tax Foundation

New IRS data shows the US federal income tax system continues to be progressive as high-income taxpayers pay the highest average income tax rates. Average tax rates for all income groups remain lower after the Tax Cuts and Jobs Act (TCJA).| Tax Foundation

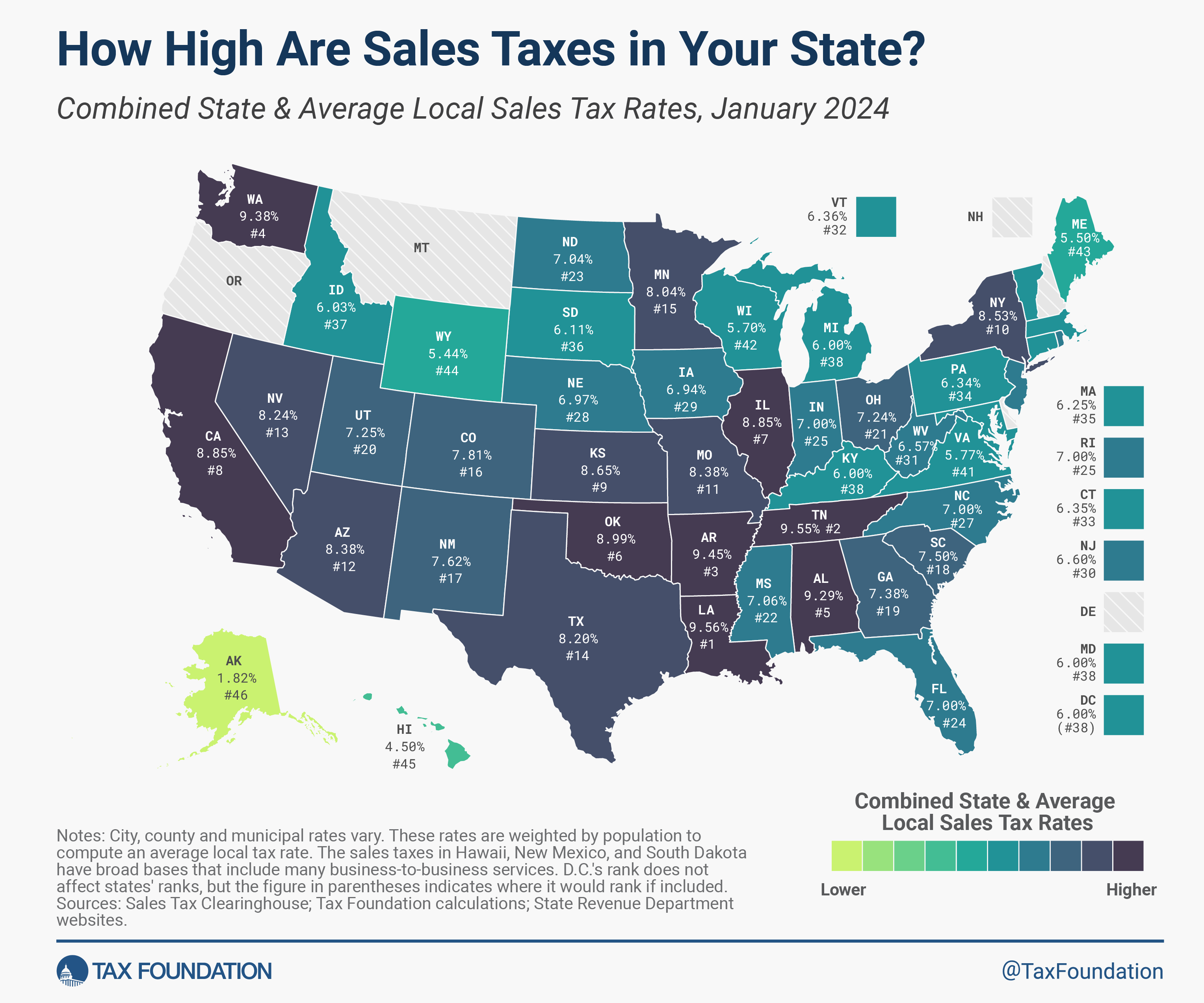

The sales tax is the second-largest source of state tax revenue and an important source of local tax revenue, but decades of base erosion threaten the tax’s share of overall revenue and have prompted years of countervailing rate increases.| Tax Foundation

Across all individual tax filers throughout the US, the average tax cut per taxpayer will be over $3,700 in 2026.| Tax Foundation

The Joint Committee on Taxation (JCT) is a nonpartisan congressional committee in the United States that assists both the House and Senate with tax legislation.| Tax Foundation

How have federal tax expenditures changed since passage of the Tax Cuts and Jobs Act? We compare 2017 and 2018 Joint Committee on Taxation estimates.| Tax Foundation

The poor revenue performance of Philadelphia’s soda tax, 24 times the rate on beer, threatens the education programs it was intended to fund.| Tax Foundation

Nebraska has an opportunity to revise the property tax package enacted in 2024 to ensure that Nebraskans enjoy meaningful property tax relief.| Tax Foundation

With such an important change to Iowa’s property tax system, it’s important that lawmakers get the details right.| Tax Foundation

The mix of tax sources states choose can have important implications for both revenue stability and economic growth, and the many variations across states are indicative of the different ways states weigh competing policy goals.| Tax Foundation

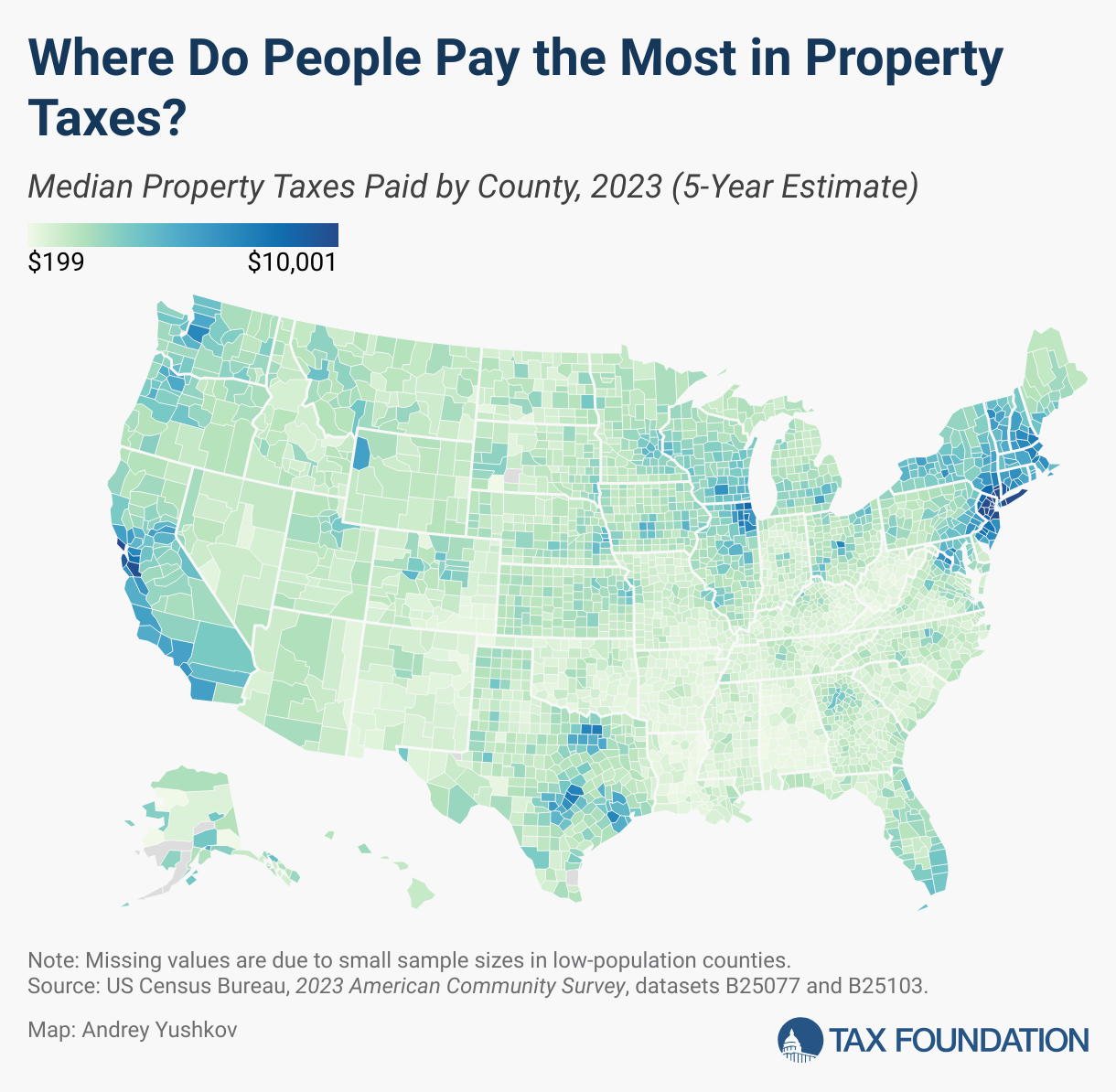

Property taxes are the primary tool for financing local governments. While no taxpayers in high-tax jurisdictions will be celebrating their yearly payments, property taxes are largely rooted in the benefit principle of taxation: the people paying the property tax bills are most often the ones benefiting from the services.| Tax Foundation

Montana’s 2025 legislative session has seen a flurry of property tax reform proposals, a response to the surge in property valuations in the state. Unfortunately, hasty decision-making can result in suboptimal policy outcomes.| Tax Foundation

This legislative session, local taxes are a major topic of debate in Indiana. Although the state’s property tax system is already nationally competitive, dramatic increases in assessed values have created discontent in recent years.| Tax Foundation

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.| Tax Foundation

If the federal government really wanted to make saving more accessible for taxpayers, it would swap the proposal for Trump Accounts to replace the complicated mess of savings accounts currently available with universal savings accounts.| Tax Foundation

A user fee is a charge imposed by the government for the primary purpose of covering the cost of providing a service, directly raising funds from the people who benefit from the particular public good or service being provided. A user fee is not a tax, though some taxes may be labeled as user fees or closely resemble them.| Tax Foundation

Different taxes have different economic effects, so policymakers should always consider how tax revenue is raised and not just how much is raised.| Tax Foundation

Exempting overtime would unnecessarily complicate the tax code, increase compliance and administrative costs, and reduce neutrality by favoring certain work arrangements over others.| Tax Foundation

We estimate the One Big Beautiful Bill Act would increase long-run GDP by 1.2 percent and reduce federal tax revenue by $5 trillion over the next decade on a conventional basis.| Tax Foundation

The House "One Big Beautiful Bill" includes a new 3.5 percent tax on remittances, or non-commercial transfers of money that people in the US send to people abroad.| Tax Foundation

Our preliminary analysis finds the tax provisions increase long-run GDP by 0.8 percent and reduce federal tax revenue by $4.0 trillion from 2025 through 2034 on a conventional basis before added interest costs.| Tax Foundation

Policymakers have passed legislation to extend many provisions of the 2017 Tax Cuts and Jobs Act (TCJA) alongside dozens of new tax provisions.| Tax Foundation

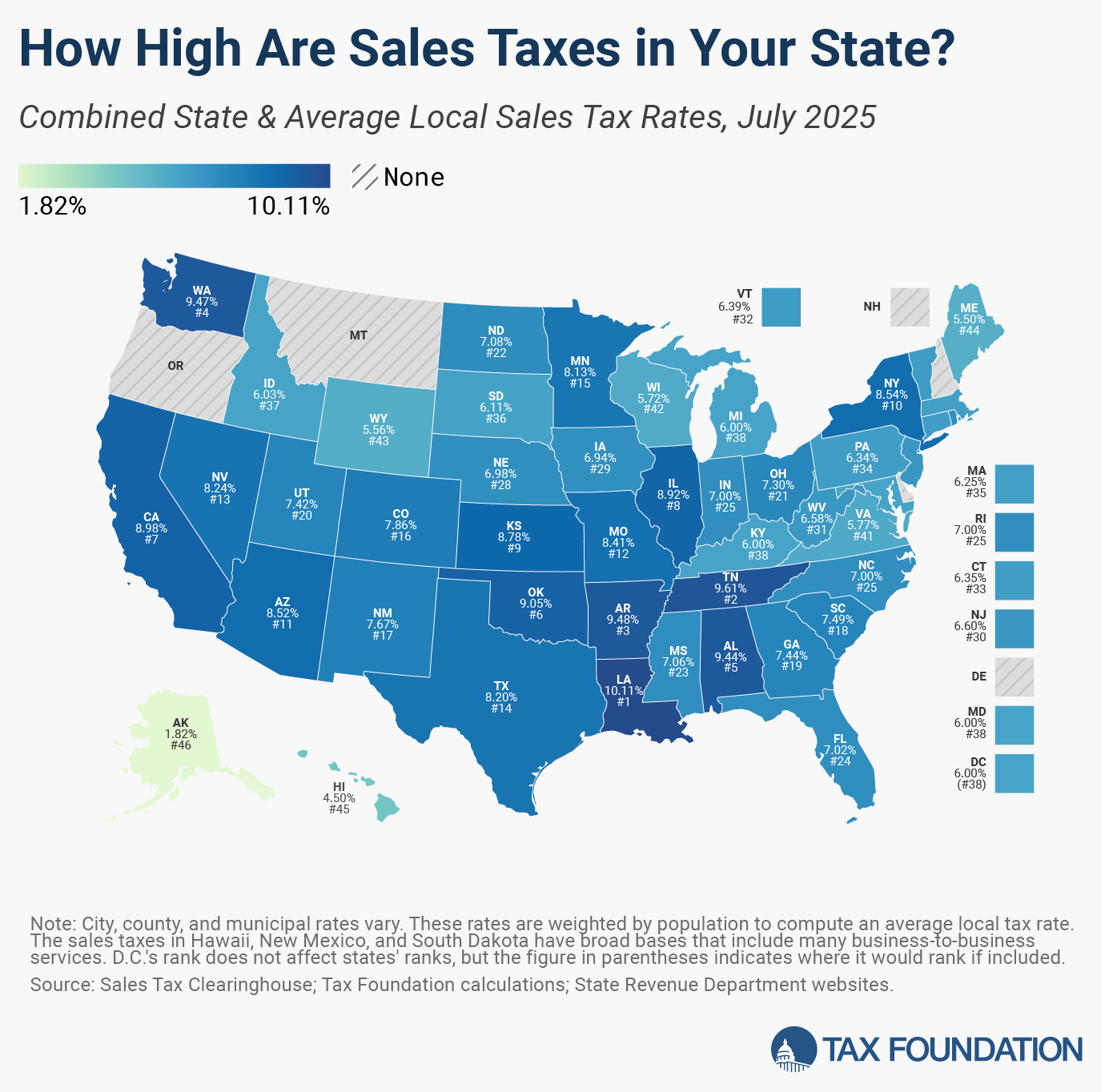

Retail sales taxes are an essential part of most states’ revenue toolkits, responsible for 24 percent of combined state and local tax collections.| Tax Foundation

Retail sales taxes are an essential part of most states’ revenue toolkits, responsible for 32 percent of state tax collections and 13 percent of local tax collections (24 percent of combined collections).| Tax Foundation

Gov. Pillen is searching for tax burden relief. But his plan, which reportedly involves a two-tiered sales tax and the state’s assumption of most school funding responsibility, would have profound implications that even those most convinced of the urgency of property tax relief may find unworkable and unpalatable.| Tax Foundation

The home mortgage interest deduction currently allows itemizing homeowners to deduct mortgage interest paid on up to $750,000 worth of principal.| Tax Foundation

The Tax Cuts and Jobs Act increased the standard deduction and reduced the value of certain itemized deductions. How many taxpayers now itemize in 2019?| Tax Foundation

While tariffs are often presented as tools to enhance US competitiveness, a long history of evidence and recent experience shows they lead to increased costs for consumers and unprotected producers and harmful retaliation, which outweighs the benefits afforded to protected industries.| Tax Foundation

Estimating the economic effects of different types of taxes informs policymakers about the trade-offs of raising revenue in a given way.| Tax Foundation

The economic literature overwhelmingly suggests that an income tax increase of this magnitude would negatively affect economic growth and opportunity in Rhode Island.| Tax Foundation

Policymakers can and should address taxpayers’ legitimate grievances about out-of-control property tax bills, but they should do so without upending a system of taxation that is more efficient, fair, and pro-growth, and better suited to municipal finance, than any of the alternatives.| Tax Foundation

Marijuana taxation is one of the hottest policy issues in the United States. Twenty-one states have implemented legislation to legalize and tax recreational marijuana sales.| Tax Foundation

Many states regulate and tax legal marijuana sales and consumption, despite the ongoing federal prohibition. Explore the data here.| Tax Foundation

As the property tax debate continues in Kansas, two new proposals have emerged that are much better structured, and would be more effective, than the assessment limits. However, policymakers should consider additional modifications.| Tax Foundation

Permanently extending the expiring individual, estate, and business tax provisions would boost long-run economic output by 1.1 percent, the capital stock by 0.7 percent, wages by 0.5 percent, and hours worked by 847,000 full-time equivalent jobs.| Tax Foundation

“No tax on tips” might be a catchy idea on the campaign trail. But it could create plenty of headaches, from figuring out tips on previously untipped services to an unexpectedly large loss of federal revenue.| Tax Foundation

Contrary to President Trump’s claims, Americans will bear the costs of the next trade war in the form of lower incomes as tariffs cause prices of imported goods to rise.| Tax Foundation

The tariffs amount to an average tax increase of nearly $1,300 per US household in 2025.| Tax Foundation

The Trump administration has imposed $42 billion worth of new taxes on Americans by levying tariffs on thousands of products. Tariffs are taxes.| Tax Foundation

The Trump administration appears to be moving in a “reciprocal” policy direction despite the significant negative economic consequences for American consumers of across-the-board tariffs on goods coming into the US. However, the EU’s VAT system should not be used as a justification for retaliatory tariffs.| Tax Foundation

While there are many ways to show how much state governments collect in taxes, the Index evaluates how well states structure their tax systems and provides a road map for improvement.| Tax Foundation

President-elect Trump may want to impose tariffs to encourage investment and work, but his strategy will backfire. Tariffs will certainly create benefits for protected industries, but those benefits come at the expense of consumers and other industries throughout the economy.| Tax Foundation

Lawmakers will need to pursue fiscal responsibility as they address the tax law expirations, but fiscal responsibility requires finding sound ways to pay for spending priorities. Tariffs don’t make the cut.| Tax Foundation

On tax policy, Harris carries forward much of President Biden’s FY 2025 budget, including higher taxes aimed at businesses and high earners. She would also further expand the child tax credit (CTC) and various other tax credits and incentives while exempting tips from income tax.| Tax Foundation

We estimate Trump’s proposed tariffs and partial retaliation from all trading partners would together offset more than two-thirds of the long-run economic benefit of his proposed tax cuts.| Tax Foundation

When the government imposes a tariff, it may be trading jobs and production in one part of the economy for jobs in another part of the economy by increasing production costs for downstream industries.| Tax Foundation

Former President Donald Trump’s proposed 10 percent tariff would raise taxes on American consumers by more than $300 billion a year—a tax increase rivaling the ones proposed by President Biden.| Tax Foundation

A pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates.| Tax Foundation

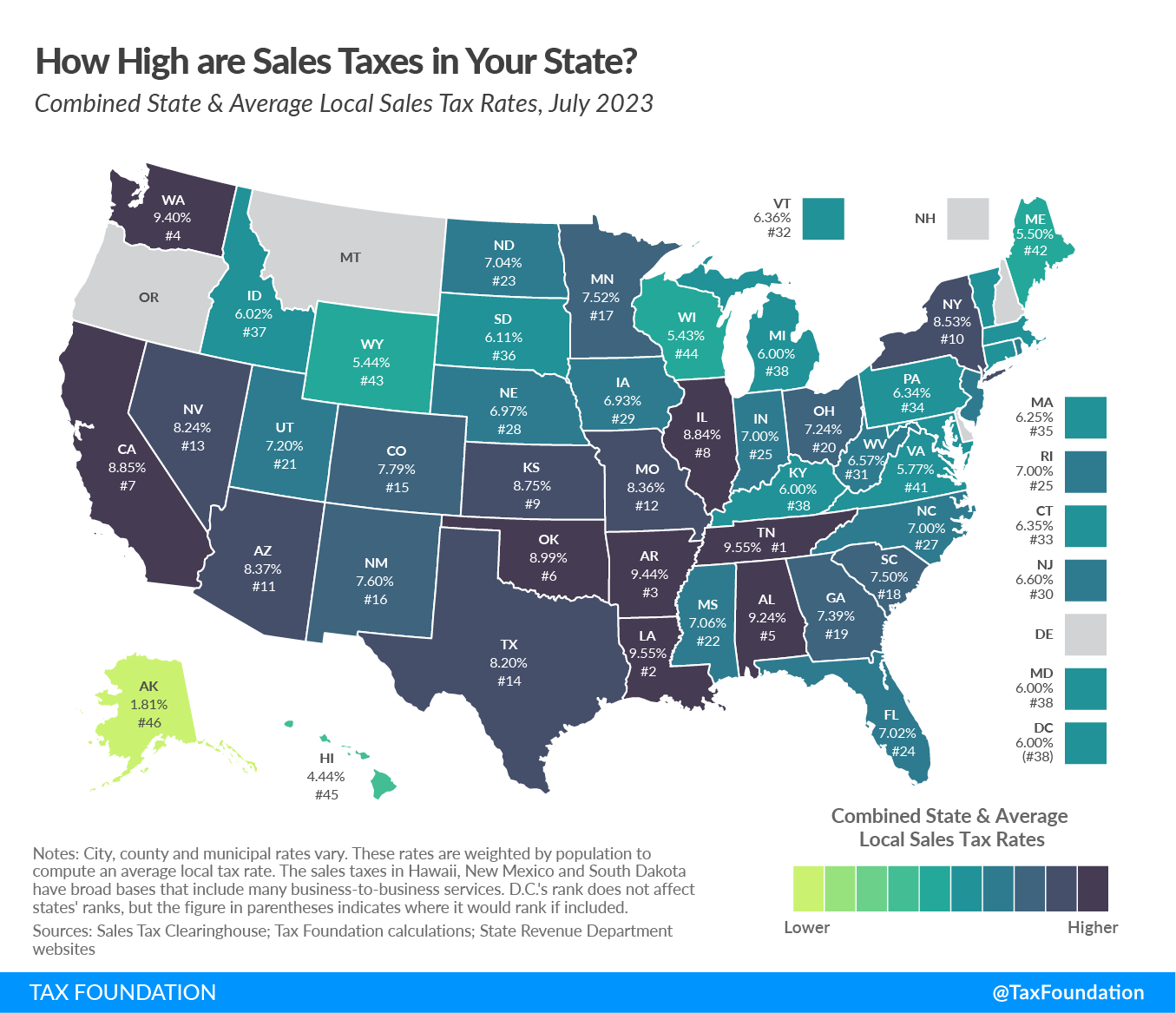

Compare the latest 2023 sales tax rates as of July 1st. Sales tax rate differentials can induce consumers to shop across borders or buy products online.| Tax Foundation

Tax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action.| Tax Foundation

The 2017 Tax Cuts and Jobs Act (TCJA) was the largest corporate tax reform in a generation, lowering the corporate tax rate from 35 percent to 21 percent, temporarily allowing full expensing for short-lived assets (referred to as bonus depreciation), and overhauling the international tax code.| Tax Foundation

A progressive tax is one where the average tax burden increases with income. High-income families pay a disproportionate share of the tax burden, while low- and middle-income taxpayers shoulder a relatively small tax burden.| Tax Foundation

Tax burdens rose across the country as pandemic-era economic changes caused taxable income, activities, and property values to rise faster than net national product. Tax burdens in 2020, 2021, and 2022 are all higher than in any other year since 1978.| Tax Foundation

From 2021-2024, within the span of 3.5 years, more states enacted laws converting graduated-rate individual income tax structures into single-rate income tax structures than did so in the whole 108-year history of state income taxation up until that point.| Tax Foundation

In recognition of the fact that there are better and worse ways to raise revenue, our Index focuses on how state tax revenue is raised, not how much. The rankings, therefore, reflect how well states structure their tax systems.| Tax Foundation

The IRS recently released the new inflation adjusted 2023 tax brackets and rates. Explore updated credits, deductions, and exemptions, including the standard deduction & personal exemption, Alternative Minimum Tax (AMT), Earned Income Tax Credit (EITC), Child Tax Credit (CTC), capital gains brackets, qualified business income deduction (199A), and the annual exclusion for gifts.| Tax Foundation