Division by zero is known as a 'singularity.' It’s the point where equations break down, values become 'indeterminate,' things stop working normally, and variables shoot toward infinity and suddenly collapse on the other side. The current speculative bubble was driven by a singularity. Avoiding the crash on the other side relies on the willingness of investors to accept the lowest long-term return prospects in U.S. history, forever. Extremely high prices may seem like a beautiful thing, but...| Hussman Funds

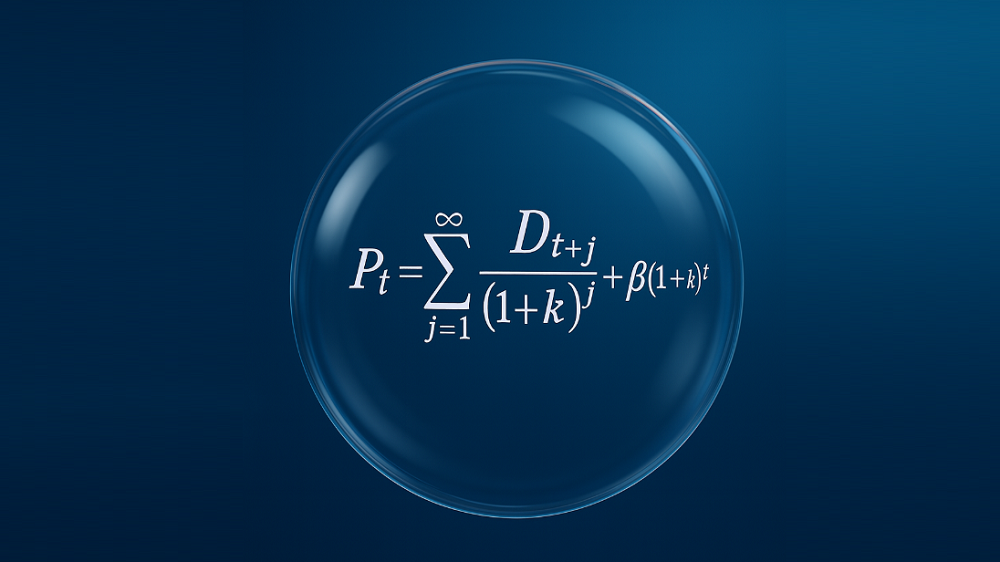

Bubbles are generated when investors drive valuations higher without simultaneously adjusting expectations for future returns lower. In other words, the defining feature of a bubble is inconsistency between expected returns based on price behavior and expected returns based on valuations. The “Bubble Term” measures the gap between the two. Unless the Bubble Term is able to become exponentially larger forever – it shows up as a growing gap between the long-term return that investors expe...| Hussman Funds

With our most reliable stock market valuation measures at the highest extremes in U.S. history, record negative readings on our most reliable 'equity risk premium' gauge (estimated S&P 500 total returns vs. Treasury yields), and the narrowest junk bond risk premiums in history, it’s useful for investors to remember that a market crash is nothing but risk-aversion meeting a market that is not priced to tolerate risk. Emphatically, nothing in our investment discipline relies on a market colla...| Hussman Funds

If you look deeply into a speculative bubble, you can see the market collapse in it. If you look deeply into a market collapse, you can see the bull market in it. Each is a continuation of the other.| Hussman Funds

At its core, a market crash is nothing but risk-aversion meeting a market that's not priced to tolerate risk. We always become concerned about “trap door” outcomes when rich valuations are joined by deterioration in the uniformity of market internals - which is our most reliable gauge of speculation versus risk-aversion among investors. Our concerns about trap door conditions become even more pointed when investor confidence has been destabilized. We are presently on high alert for a poss...| Hussman Funds

In recent years, our most reliable measures of stock market valuation have pushed beyond their 1929 and 2000 peaks, and I’ve described the period since early 2022 as the extended peak of the third great speculative bubble in U.S. history. In my view, that process is now complete. The stock market faces severe downside risk ahead, and the U.S. is constrained in the unsystematic monetary and fiscal expansion that both amplified that bubble and fueled record but wholly impermanent corporate pr...| Hussman Funds

It’s enormously tempting to imagine, at bubble highs, that glorious backward-looking returns, far greater than those previously implied by valuations, demonstrate that historical standards of value are outdated and obsolete. In 1934, Benjamin Graham and David Dodd described the mood surrounding the 1929 market peak, observing that investors had abandoned their attention to valuations because 'the records of the past were proving an undependable guide to investment.' For the moment, neither ...| Hussman Funds

Change is the sum of fundamental trends, the gradual elimination of accumulated extremes, and the random arrival of new shocks. This is true for nearly every process, including economic growth and stock market returns.| Hussman Funds

One of most dangerous habits of a speculative crowd is the tendency to use unconditional averages and unconditional probabilities regardless of how extreme market conditions have become. This is like stepping into a house with two rooms, one with the temperature at 0 degrees and one at 140 degrees, and expecting a temperature of 70 either way.| Hussman Funds