One of the main decisions that every Canadian retiree has to make is in regards to at what age they want to convert their RRSP to a RRIF. Consequently, questions such as: What is the maximum age to convert my RRSP to a RRIF? Is there a penalty for not converting my RRSP to a RRIF before 71? Do I pay tax when I rollover my RRSP to RRIF? Are some of the most common ones that we get in regards to retirement planning. Ultimately the RRSP vs RRIF debate comes down to the age of you and your partn...| Million Dollar Journey

Moving from the accumulation stage of my professional career, to withdrawing investments in early retirement was more difficult than I would have predicted a few years ago. For those who haven’t been following me since I started writing Million Dollar Journey back in 2005, I have slowly-but-surely detailed my rise from a very average net worth, to building an investment portfolio that allowed me to reach complete financial independence. Here are some of the key articles that I’ve written ...| Million Dollar Journey

Are you curious about how investing taxes are calculated on capital gains, dividends, and interest in Canada? I’m not a tax expert, but with tax loss harvesting season coming out, I figured it might be a good time to review some of the basics between how Canadian investment returns are taxed in your RRSP, TFSA, and non-registered accounts. Investing Taxes in an RRSP Let’s start with RRSPs. As you probably know, RRSP contributions and investment growth are taxable only upon withdrawal. A...| Million Dollar Journey

Since the inception of this blog, I've received numerous emails from readers asking where to put larger deposits. Most know about CDIC (Canada Deposit Insurance Corporation) and how it protects most accounts up to $100,000, but what about amounts greater than $100,000? What do you do then? What exactly happens to your money if a bank or brokerage goes bankrupt? Since I haven't written about them yet, lets take a look at the two major account insurances in Canada, CDIC and CPIF. Canada D...| Million Dollar Journey

After writing a deep dive article on whether the 4% safe withdrawal rate still works for retirement at various ages, I received a lot of questions basically asking: “Ok, so 4% is a good rule of thumb, but when I actually go to withdraw money from my various investment accounts, to put into my chequing account & high interest savings account in order to pay for day-to-day expenses, what is the best way to avoid taxes?” Upon reading many of these types of questions, I realized that I wasn...| Million Dollar Journey

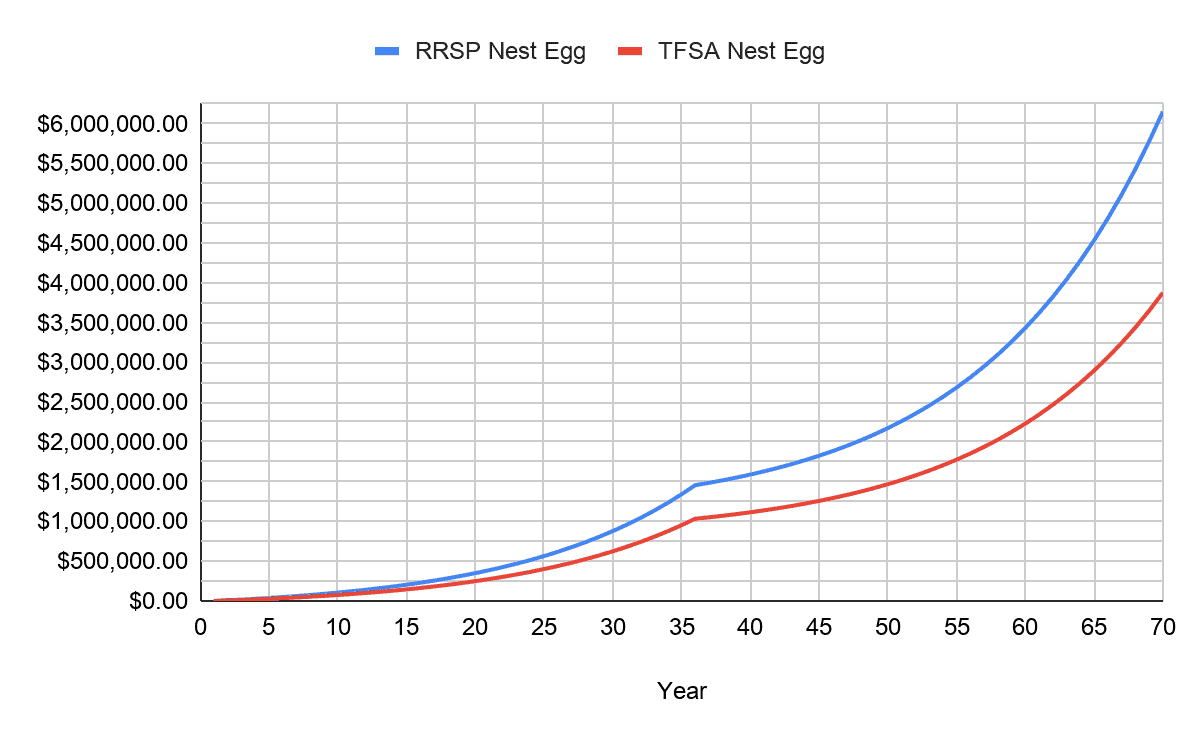

Canadians have fantastic options when it comes to registered accounts. Registered accounts are beneficial for many reasons, the main reason being that they are tax advantaged. Tax advantage accounts are those that allow you to grow your money tax-free or allow you to defer paying taxes until later. However, all registered accounts are not created equal, and before you invest, you want to read our detailed TFSA vs RRSP guide to better understand what these two registered accounts can do for yo...| Million Dollar Journey

There is a TON of investment advice out there. Some should only be taken into consideration after a thorough investigation and planning. Some - like contributing to a TFSA - is just sound advice that should be acted on quickly. The reason? Two words: tax free. That is not something you hear often, and that’s why we want to help you start contributing to your TFSA as quickly as possible to achieve maximum money saving and investment earning results. If you turned 18 on or before 2009...| Million Dollar Journey

Long-term investing is one of the most powerful ways to grow your wealth. As the name implies, long-term investing means that an investor buys an asset with the intent to hold it for some time. The time frame can be years or even decades. Over time, long-term investing has the potential to produce excellent returns due to the magic of compound interest. While this strategy might not appeal to everyone, especially those with a high risk tolerance, it has historically proven to be an effectiv...| Million Dollar Journey

The best Canadian high interest savings accounts for 2024 combine a mix of high interest rates, with no-fee banking, and elite user-friendly platforms. One thing to note right off the top: If your savings goal is more than 6 months in the future, you should likely be checking out our Best GIC Rates in Canada Comparison instead of using a high interest savings account. That said, our top HISAs are an excellent short term investment option when it comes to saving for a trip, storing an emergenc...| Million Dollar Journey

Because I’ve written a lot about the Best Canadian ETFs and the top dividend ETFs, I tend to get a lot of questions and comments asking me about the MER and taxes on ETFs that hold equities from other countries. Obviously when you’re asking those types of in-depth questions you already understand the value of index investing, and instant diversification. Personally, I like to balance my love of Canadian dividend stocks, with non-Canadian ETFs to get super-convenient international exposure...| Million Dollar Journey

You’d think it’d be a relatively easy quest to answer the question: How much will a Canadian spend in retirement? When I set out to create the first retirement course for Canadians looking to retire in the next 25 years (or in the early stages of retirement) I figured that determining how much the average Canadians spent in retirement would be pretty straightforward. You can check out what that course has to offer by clicking here. I also knew that it was quite important to get this infor...| Million Dollar Journey

If you’ve been following MDJ for a while, you will come to learn that I’m a fan of two investing strategies, index investing and investing for income through Canada’s best dividend stocks. I like index investing (also known as passive investing) for its ease, low cost, and ability to beat most active mutual fund returns over the long term. I use this strategy for: my spousal RRSP; the international portion of my RRSP; and, the education fund (RESP) that I set up for my two kids. Divid...| Million Dollar Journey

The concept of a safe withdrawal rate (and the 4% rule) is a key planning tool for Canadians of all ages. After all, if you don’t have a general withdrawal plan, how can you know how much you need to save in the first place? If you have been reading MDJ for years, you already have an idea of how to use a Canadian online broker account to DIY-invest your way to a solid nest egg. Now you’re planning for retirement (whether it’s 20+ years away or next year) and you’re wondering how to ...| Million Dollar Journey

You likely already know that investing in an RRSP is one of the best, most tax efficient ways to save for retirement. The good news is that if you or your common-law partner or spouse have unequal incomes, you can open and contribute to a spousal RRSP account. In doing so, you can maximize the benefits of an RRSP account for you and your spouse, no matter if one of you is not earning an income or earning much less. Read on to learn more about how a spousal RRSP account works, what the tax i...| Million Dollar Journey

Investing in Canadian Dividend Kings (sometimes known as Dividend Aristocrats) tends to come back into fashion when bond yields and GIC rates start to go down. With safer assets generating so little income, dependable dividend payers begin to look more and more attractive. Of course, staying committed to dividends can be a challenge when stocks like Nvidia are soaring. The real test for any dividend investor is sticking to the plan through thick and thin. Click here to jump directly to my 202...| Million Dollar Journey