Gross Receipts Taxes: An Assessment of Their Costs and Consequences

Gross receipts taxes, by their very design, lack transparency. Our report explores the pros and cons of a turnover tax, also known as a gross receipts tax.| Tax Foundation

Gross receipts taxes, by their very design, lack transparency. Our report explores the pros and cons of a turnover tax, also known as a gross receipts tax.| Tax Foundation

The sales tax is the second-largest source of state tax revenue and an important source of local tax revenue, but decades of base erosion threaten the tax’s share of overall revenue and have prompted years of countervailing rate increases.| Tax Foundation

The mix of tax sources states choose can have important implications for both revenue stability and economic growth, and the many variations across states are indicative of the different ways states weigh competing policy goals.| Tax Foundation

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.| Tax Foundation

Retail sales taxes are an essential part of most states’ revenue toolkits, responsible for 32 percent of state tax collections and 13 percent of local tax collections (24 percent of combined collections).| Tax Foundation

Policymakers can and should address taxpayers’ legitimate grievances about out-of-control property tax bills, but they should do so without upending a system of taxation that is more efficient, fair, and pro-growth, and better suited to municipal finance, than any of the alternatives.| Tax Foundation

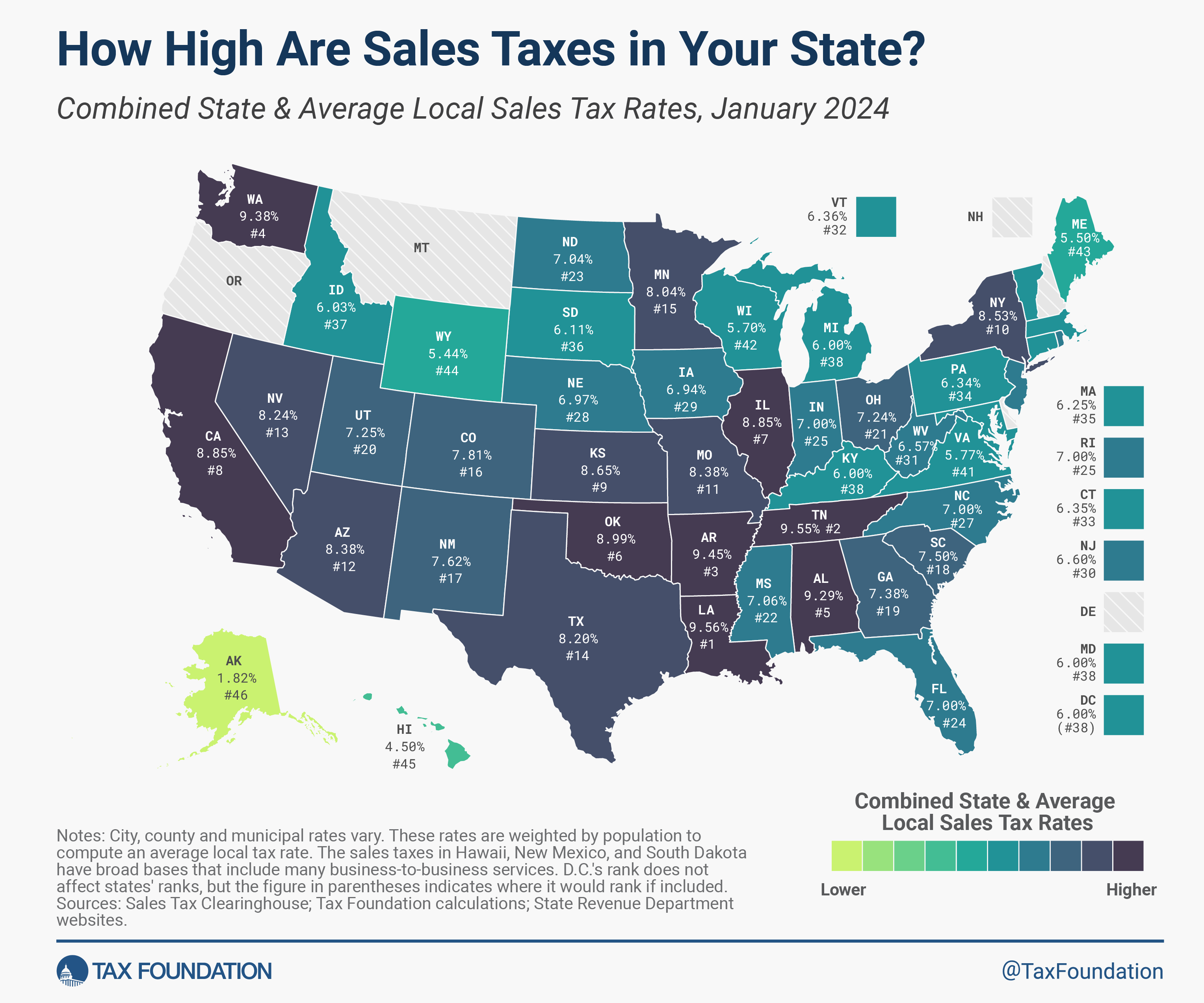

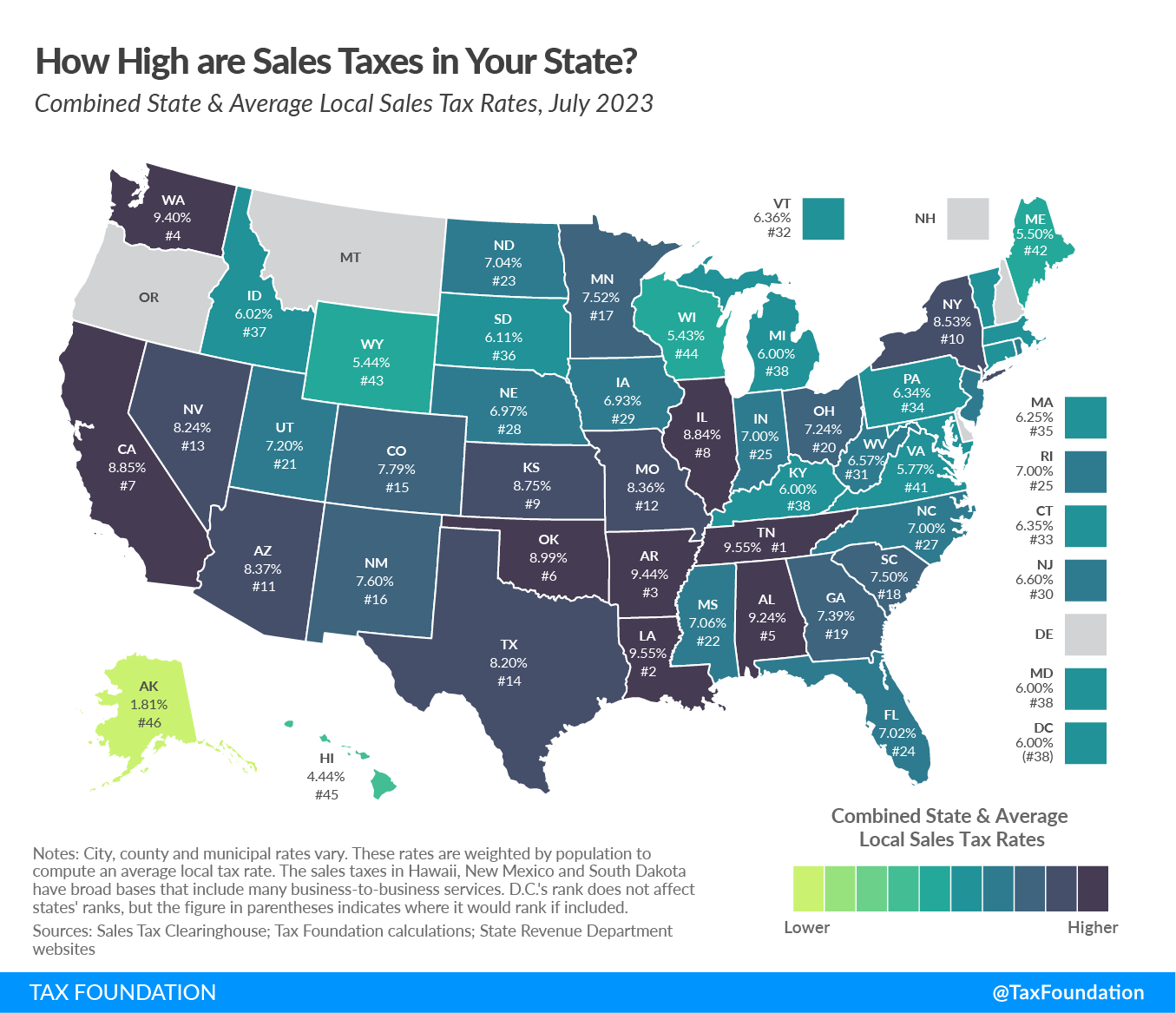

Compare the latest 2023 sales tax rates as of July 1st. Sales tax rate differentials can induce consumers to shop across borders or buy products online.| Tax Foundation

Tax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action.| Tax Foundation