The GST council, in its forthcoming 57th meeting, may focus on additional revisions to facilitate the procedure and policies. In the 56th meeting of the council held in September, a suggestion was provided to ease refund and registration processes, along with a rate overhaul. The rate exercise has been completed. The upcoming meeting may deliberate […] The post Upcoming 57th GST Council Meeting: Ease of Compliance & Policies first appeared on SAG Infotech Official Tax Blog.| SAG Infotech Official Tax Blog

The Insurance Brokers Association of India (IBAI) has called upon the Ministry of Finance to implement further initiatives, beyond the recent revisions to the Goods and Services Tax (GST), aimed at increasing the penetration rates of health and life insurance across the nation. GST rate cut can exempt individual health insurance premiums to a specific […] The post IBAI Urges Finance Ministry to Go Beyond GST Reforms to Broaden Insurance Coverage first appeared on SAG Infotech Official Tax B...| SAG Infotech Official Tax Blog

The Central Board of Indirect Taxes and Customs (CBIC) has outlined comprehensive guidelines for the provisional approval of GST refund requests through Instruction No. 06/2025-GST, issued on October 3, 2025. This process is guided by a system-driven identification mechanism and a rigorous risk assessment framework. The same complies with the decision of the 56th GST […] The post GST Instruction 06/2025: Risk-Based Provisional Sanction of Refunds first appeared on SAG Infotech Official Tax ...| SAG Infotech Official Tax Blog

If a notice regarding Goods and Services Tax (GST) is sent to an outdated address after a person’s registration has been cancelled, such notice is deemed invalid, the Bombay High Court has recently ruled. The court further stated that making decisions based on a notice not properly served violates fair legal practices. Dipak Metal Industries, […] The post Bombay HC Quashes GST SCN Issued to Old Address, Cites Violation of Natural Justice first appeared on SAG Infotech Official Tax Blog.| SAG Infotech Official Tax Blog

The Delhi Sales Tax Bar Association, a well-established group of tax professionals in India, has approached the Union Finance Minister with an important request. They are asking for the quick setup of the GST Annual Return (Form GSTR-9) and Reconciliation Statement (Form GSTR-9C) for the financial year 2024-25 on the GST online platform. This will […] The post DSTBA Urges FM for Early Release of GSTR-9 and GSTR-9C Forms first appeared on SAG Infotech Official Tax Blog.| SAG Infotech Official Tax Blog

Most of the automobile firms have provided the benefits of the GST reduction to consumers, while the same is slow in other categories like packaged foods and medicines because of retailers’ unwillingness to sell at lower costs without the brands or manufacturers agreeing to make up for their losses, a community survey revealed. Out of| SAG Infotech Official Blog

The government is currently examining e-commerce platforms to ensure that consumers benefit from the recent reductions in Goods and Services Tax (GST) on essential items and Fast-Moving Consumer Goods (FMCG). This initiative aims to guarantee that the tax savings are effectively transferred to buyers, enhancing transparency and fairness in pricing. Even after the GST cut| SAG Infotech Official Blog

GST-related 3000 complaints have been received by the National Consumer Helpline since the inception of the revised rates. For additional action, some of these complaints are being sent to the Central Board of Indirect Taxes and Customs (CBIC). Consumer Affairs Secretary Nidhi Khare stated, "Every day, we are receiving complaints. So far, we have received| SAG Infotech Official Blog

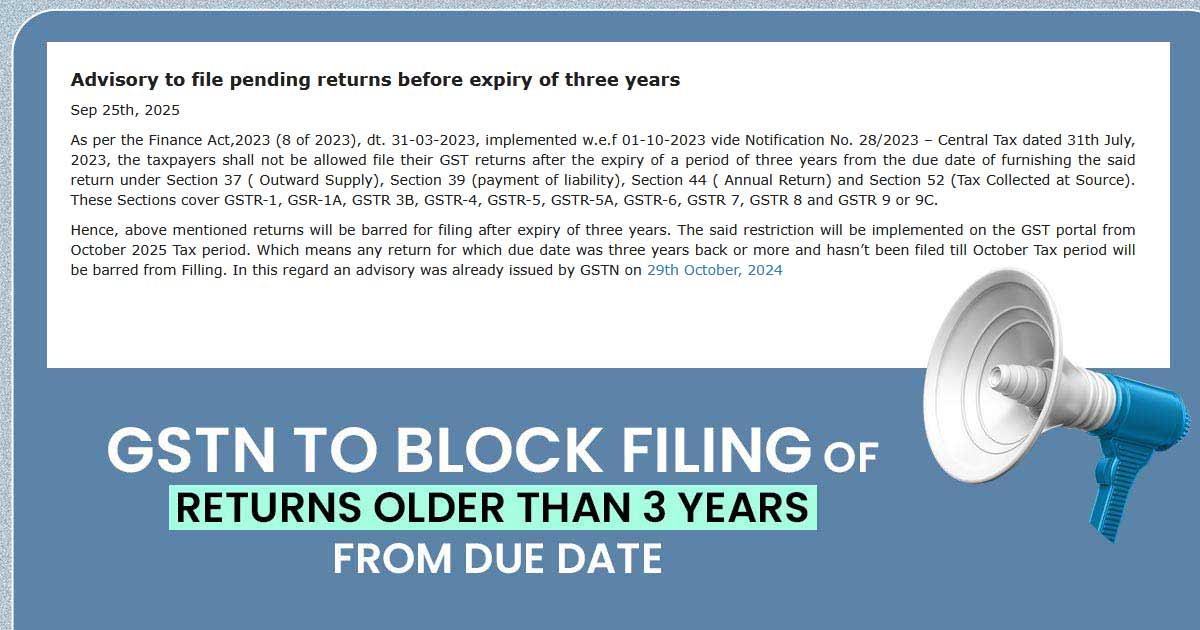

A crucial update will be implemented on the GST portal by the Goods and Services Tax Network (GSTN). This amendment could permanently block your Input Tax Credit (ITC). Let’s find out how. Three years after the due date for filing GST returns, the GSTN declared that taxpayers would be unable to furnish their GST returns. Taxpayers have not| SAG Infotech Official Blog

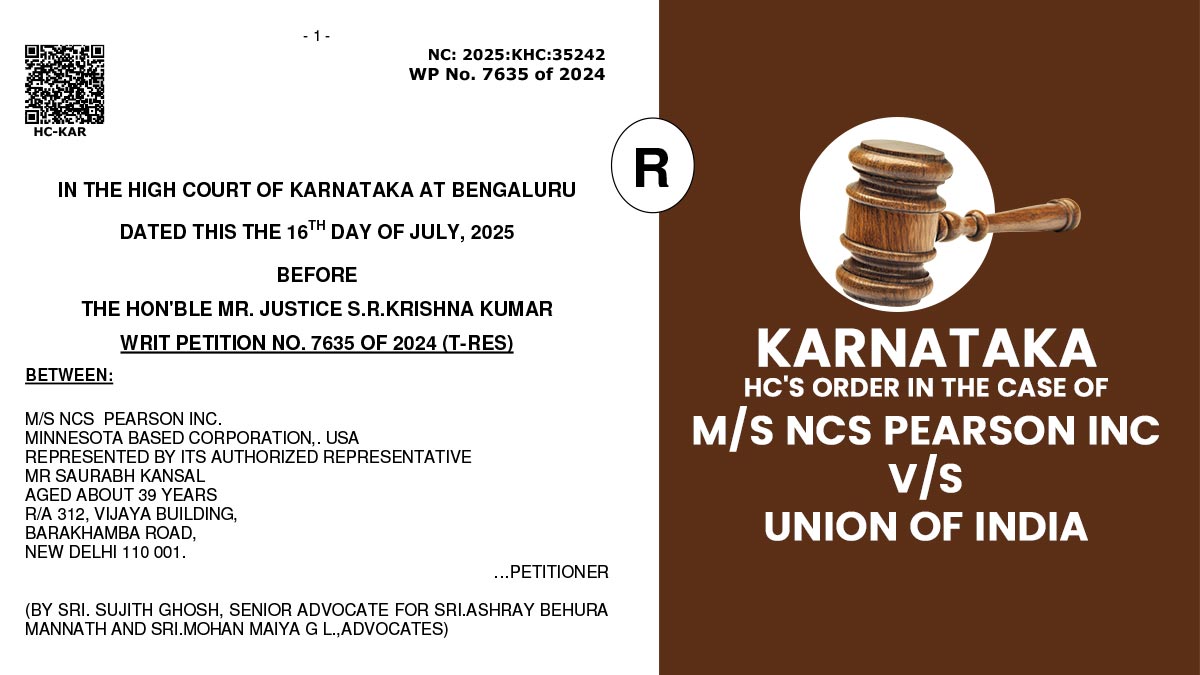

The Karnataka High Court has clarified that not accurately reporting the correct value in tax returns or applying the appropriate Goods and Services Tax (GST) rate does not constitute suppression under Section 74 of the Central Goods and Services Tax (CGST). This ruling emphasises the distinction between honest errors and deliberate suppression in tax reporting.| SAG Infotech Official Blog

Look at how GST software makes RCM compliance easier for businesses by handling complex tax calculations, keeping up with GST rules, and cutting down on errors.| SAG Infotech Official Blog

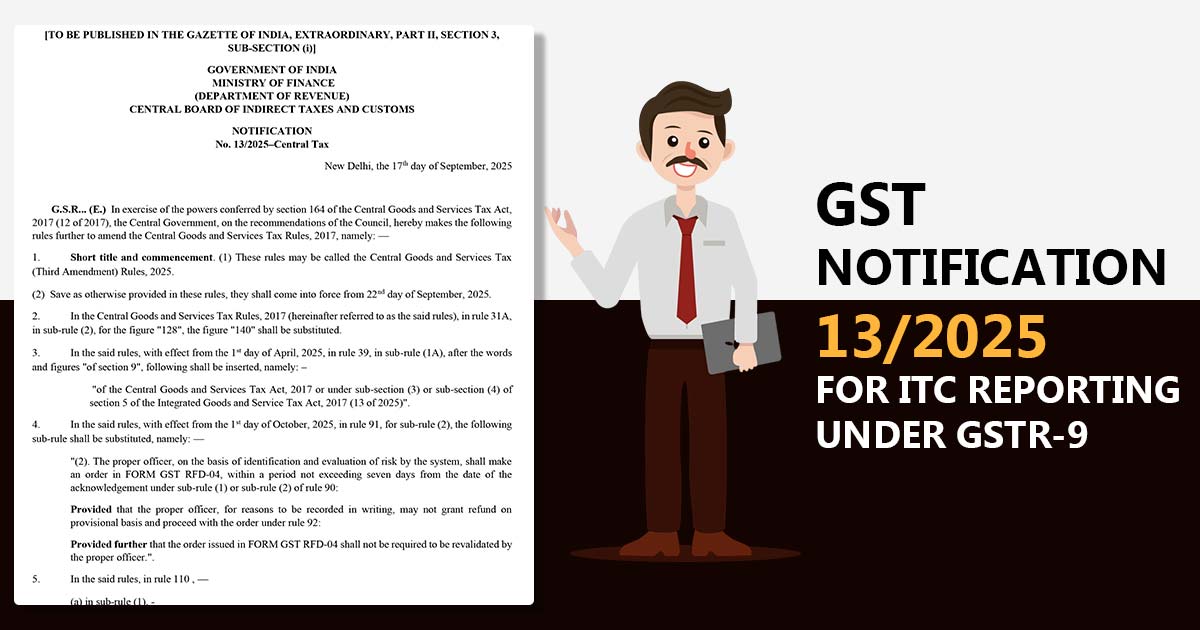

On 17th September 2025, the CBIC announced the CGST 3rd Amendment Rules, 2025, via Notification No. 13/2025. Effective from 22nd September 2025, these amendments introduce key changes in the reporting of Input Tax Credit (ITC) in the Annual Return Form GSTR-9. Key Changes in ITC Reporting Under GSTR-9 The important amendments of ITC disclosure in| SAG Infotech Official Blog

Starting Sept 22, 2025, the CBIC has announced that local delivery services, including those for groceries, food, and essential items ordered online, will be subject to an 18% Goods and Services Tax (GST). This change may lead to increased costs for consumers making online purchases. In its most recent FAQ, the CBIC clarified the application| SAG Infotech Official Blog