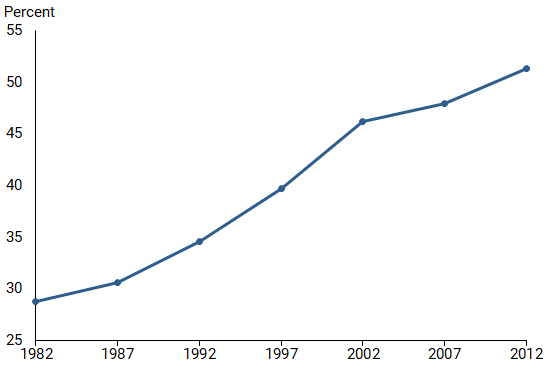

U.S. productivity is growing slower than in the past. Meanwhile, sales have become increasingly concentrated in the largest businesses. Analysis suggests that IT innovation may have facilitated the rise in concentration by reducing the cost for large firms to enter new markets. This contributed to booming productivity growth from 1995 to 2005. Though large firms are more profitable, their expansion may have increased competition and reduced profit margins within markets. Lower profit margins ...| Federal Reserve Bank of San Francisco

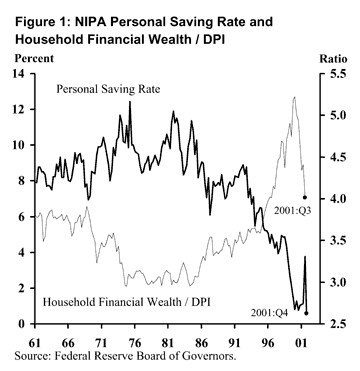

In recent years, the personal saving rate in the United States has fallen sharply, and it is now at a very low level compared either to U.S. historical experience or to the savings behavior of many other industrialized countries. From 1980 through 1994, the U.S. saving rate averaged 8%; thereafter, it fell steeply, and since mid-2000, with allowance made for the tax rebates that boosted household saving in the months of July, August, and September 2001, it has averaged approximately 1%.| Federal Reserve Bank of San Francisco

State-level unemployment claims can provide a real-time measure of national labor market conditions and the overall state of the economy. A rapid and widespread buildup of stress in state labor markets usually signals the start of a recession. In mid-2024, some widely followed indicators of recession risk flashed red. However, analysis of state-level data indicates that labor market declines were not as widespread as they had been in previous recessions. Applying this analysis to the latest d...| Federal Reserve Bank of San Francisco

The unemployment rate has risen over half a percentage point since the second quarter of 2023. Individual survey data underlying the unemployment rate can help in assessing which labor market transitions account for this rise. One dominant factor appears to be a fall in the job-finding rate—the share of unemployed individuals finding employment. The duration of unemployment has also increased recently. In past decades, these patterns have frequently occurred during the onset of recessions, ...| Federal Reserve Bank of San Francisco

U.S. households accumulated significantly more wealth following the pandemic onset than would have been expected without the pandemic shock. Overall excess household wealth—measured as households’ inflation-adjusted net worth beyond pre-pandemic projections—peaked in late 2021 at $13 trillion, then rapidly fell to zero in late 2022, where it broadly remained through the third quarter of 2023. This rise and fall can be attributed mainly to financial assets, particularly equity holdings. ...| Federal Reserve Bank of San Francisco

U.S. households built up savings at unprecedented rates following the strong fiscal response and lower consumer spending related to the pandemic. Despite recent rapid drawdowns of those funds, estimates suggest a substantial stock of excess savings remains in the aggregate economy. Since 2020, households across all income levels have held a historically large share of savings in cash or other easily accessible forms. Estimates suggest that those funds could be available to support personal sp...| Federal Reserve Bank of San Francisco