Federal Reserve Chair Jerome Powell should be applauded for his decision yesterday to disabuse the markets of the notion that another Fed interest rate cut at the Federal Open Market Committee’s (FOMC) scheduled December meeting was a foregone conclusion. The post Three Cheers for Jerome Powell appeared first on American Enterprise Institute - AEI.| American Enterprise Institute – AEI

The U.S. Federal Reserve, other central banks are juggling duelling priorities The post Not stagflation, but ‘stagflationary, potentially’: FTSE Russell appeared first on Investment Executive.| Investment Executive

David Rule Digital currencies and stablecoins have increased interest in how new forms of money are adopted. Looking to three episodes from the 1690s to the First World War, this post considers how…| Bank Underground

We represent AI companies that provide market analysis and trading tools, as well as businesses that utilize these tools in the market. In fact, AI tools are becoming increasingly commonplace within the financial, fintech, and banking industries. Here is what an experienced attorney specializing in Artificial Intelligence would want you to know about this growing […] The post Algorithmic Trading and Regulatory Risk: Why AI Litigation Is Moving Fast first appeared on Traverse Legal.| Traverse Legal

Buy a Paid Subscription The developments in the legal fight between the Federal Reserve Governor Lisa Cook and the second Trump administration have evolved quite rapidly over the past three weeks. It's past time to examine where we’ve been, where we stand as of this writing and what it| Notes on the Crises

Does the Fed have the credibility not only to cut its policy rate next week but also to reduce it further in the following months, to the long-run neutral rate of 3% without stoking inflation?| The Real Economy Blog

Inside the EU, the development in France is particularly dramatic. The post Budget Deficits Globally: Focus on France appeared first on The Globalist.| The Globalist

Recently, there has been renewed attention on the natural rate of interest—often referred to as “r-star”—and whether it has risen from the historically low levels that prevailed before the COVID-19 pandemic. The natural interest rate is the real (inflation-adjusted) interest rate expected to prevail when supply and demand in the economy are in balance and inflation is stable. Some commentators claim that the prior decline in r‑star has reversed, pointing to the recent rise in future...| Liberty Street Economics

The zero lower bound is the concept that the federal funds rate would not be cut below zero percent. This lower bound constraint can limit the effectiveness of monetary policy when rates are at or near the zero lower bound, especially during recessions. In our Economic Letter, The Zero Lower Bound Remains a Medium-Term Risk, […]| San Francisco Fed

President Trump has made no secret of his dislike for Federal Reserve Chair Jerome Powell, repeatedly using sharp, disparaging nicknames such as “Mr. Too Late,” “Numbskull,” and “Knucklehead,” and even branding him “grossly incompetent.” His irritation stems from the Fed’s refusal to heed his calls for US interest rates to be cut to euro-area levels. Yet Trump overlooks a crucial point: US rates have long been higher than those in the euro area because of fundamentally diffe...| Rangvid’s Blog

The following is an excerpt from "Private Finance, Public Power: A History of Bank Supervision in America" by Peter Conti-Brown and Sean H. Vanatta, now out at Princeton University Press.| ProMarket

Philippe Bracke, Matt Everitt, Martina Fazio and Alexandra Varadi The Bank of England Agenda for Research (BEAR) sets the key areas for new research at the Bank over the coming years. This post is an example of issues considered under the Macroeconomic Environment Theme which focuses on the changing inflation dynamics and unfolding structural change … Continue reading When mortgage flexibility meets monetary policy tightening: heterogeneous impacts on spending and debt→| Bank Underground

Charlie Warburton and James Brookes Economists have repeatedly shown that readability of central banking communication matters. But they typically measure readability in a crude way – using th…| Bank Underground

On September 14, I had the opportunity to present a guest lecture to Professor Rich Clarida’s Columbia SIPA course on Global Monetary Policy in the 21st Century. My lecture was entitled, How Aggressively Did the Fed Stabilize the Economy Pre-ZLB? (Here’s a link to the slides.) My talk looked into how aggressively the Fed acted … Continue reading Guest lecture: How Aggressively Did the Fed Stabilize the Economy Pre-ZLB?→| John Roberts Macroeconomics

On March 30, I participated in a very stimulating conference hosted by Kenyon College entitled What’s My Dollar Worth? Inflation’s Causes, Consequences and Cures. The conference included speakers with a broad range of views on the causes of recent high inflation and what policy can do about it. My own contribution compared the current situation … Continue reading Expectations, Then and Now→| John Roberts Macroeconomics

The economy in 2022 was remarkably resilient to higher interest rates and tighter financial conditions. Although residential construction fell, consumer spending continued to expand. The labor mark…| John Roberts Macroeconomics

Stigler Center Assistant Director Matt Lucky reviews Kenneth Rogoff’s new book, Our Dollar, Your Problem: An Insider’s View of Seven Turbulent Decades of Global Finance, and the Road Ahead, which reflects on the rise and ongoing fall of the American dollar’s global dominance. Rogoff discusses his book with Bethany McLean and Luigi Zingales on this week’s Capitalisn’t episode, which you can listen to here.| ProMarket

Deposits are often perceived as a stable funding source for banks. However, the risk of deposits rapidly leaving banks—known as deposit flightiness—has come under increased scrutiny following the failures of Silicon Valley Bank and other regional banks in March 2023. In a new paper, we show that deposit flightiness is not constant over time. In particular, flightiness reached historic highs after expansions in bank reserves associated with rounds of quantitative easing (QE). We argue th...| Liberty Street Economics

Interest rates have fluctuated significantly over time. After a period of high inflation in the late 1970s and early 1980s, interest rates entered a decline that lasted for nearly four decades. The federal funds rate—the primary tool for monetary policy in the United States—followed this trend, while also varying with cycles of economic recessions and expansions.| Liberty Street Economics

Hannah Copeland, Lennart Brandt, Natalie Burr and Boromeus Wanengkirtyo Emissions Trading Schemes (ETS) are an increasingly popular market-based policy to impose a price on carbon emissions (previously costless to the emitter) (World Bank Group (2025), DESNZ (2025)). With carbon prices expected to increase steadily, and sectoral coverage broadening, these schemes have gained the attention of … Continue reading What happens to inflation when we put a price on carbon?→| Bank Underground

Investors betting on a near-term plunge in interest rates may be mistaking political theater for monetary policy reality. President Donald Trump’s renewed pressure on Federal Reserve Chair Jerome Powell has stirred speculation in the bond and futures markets. But history — and Powell’s own posture — suggest that such expectations are misplaced. Past confrontations between […]| CFA Institute Enterprising Investor

Banks use central bank reserves for a multitude of purposes including making payments, managing intraday liquidity outflows, and meeting regulatory and internal liquidity requirements. Data on aggregate reserves for the U.S. banking system are readily accessible, but information on the holdings of individual banks is confidential. This makes it difficult to investigate important questions like: “Which types of banks hold reserves?” “How concentrated are they?” and “Does the distribu...| Liberty Street Economics

The yield curve looks pretty good. Long term rates still are recovering. The expected date of the first short term rate hike also appears to be coming closer. This all seems like good news to me. All in all, pretty good monetary management for the COVID-19 recession, I think.It seems to me that a short position in early 2023 Eurodollar contracts has a nice risk/reward balance. Not much room for downside (declining interest rates), but quite a bit of room to run higher (higher intere...| Idiosyncratic Whisk

I haven't updated the inflation numbers for a while. Covid-19 has probably made it difficult to say too much, because there are so many compositional shifts in the demand basket. But I think it is worth taking a look at what is happening in rent inflation.| Idiosyncratic Whisk

The yield curve has taken a strong bullish move as a result of the election and the Covid-19 vaccine progress. The long end of the Eurodollar curve is nearly back to the pre-Covid level.The date of the first rate hike remains in mid-2021, but the escape velocity has increased significantly. Forward inflation breakevens remain level at about 1.6%, which suggests that the recent improvement has been due to real shocks. The Fed probably still has room for more traditional accommodation.| Idiosyncratic Whisk

Inflation breakevens continue to rise, slowly. After really flattening out last month, the yield curve perked up in August, somewhat, especially helped by recent Fed discussion about allowing for more catch-up inflation and a more of a symmetrical 2% inflation target.| Idiosyncratic Whisk

The Fed is failing us. It started out great. The initial reaction to the pandemic was timely and forceful. The yield curve on March 18 was signaling confidence. But, since then, we have been slowly sinking into stagnation. The long end of the Eurodollar curve is barely over 1% now. It is true that forward inflation expectations have continued to slowly rise, though they are still well under 2%.| Idiosyncratic Whisk

The yield curve (using Eurodollar futures) has undergone a series of shifts with the coronavirus pandemic. In the first graph, we can see that starting from the end of January, the whole curve shifted down by early March. It shifted down more by March 10, as the extent of the pandemic became worse. Then, it steepened over the next week as, across the US, cities, states, and citizens took action.| Idiosyncratic Whisk

Well, so much has happened, I hardly need to update the yield curve. Coronavirus has given us one big push into the recessionary outcome th...| www.idiosyncraticwhisk.com

Monetary policy is a primary lever for stimulating consumption and economic growth. However, when central banks hit their limits—whether it’s the lower bound on interest rates, political constraints, or other barriers—fiscal policy must often assume a greater role. But how much fiscal stimulus is needed to offset reduced monetary accommodation? In new research (link), co-authors […]| Rangvid’s Blog

Unlikely. Also, it´s likely not worse and suffers from the same shortcoming of inflation targeting, being based on the false premise of the existence of a Phillips Curve. I plan to show, hopefully convincingly, that the New Keynesian model (the centerpiece of which is the New Keynesian Phillips Curve) is grossly unsuitable for monetary policy […]| Historinhas

The first thing to note is that inflation is not a price phenomenon (don´t reason from a price change is relevant here), but a monetary phenomenon. For example, changes in relative prices (due to a…| Historinhas

image source: Karthikeyan Perumal China has a history of implementing high levels of a monetary policy known as sterilization to manage its increasing foreign exchange reserves and crawling peg exc…| The Economics Review

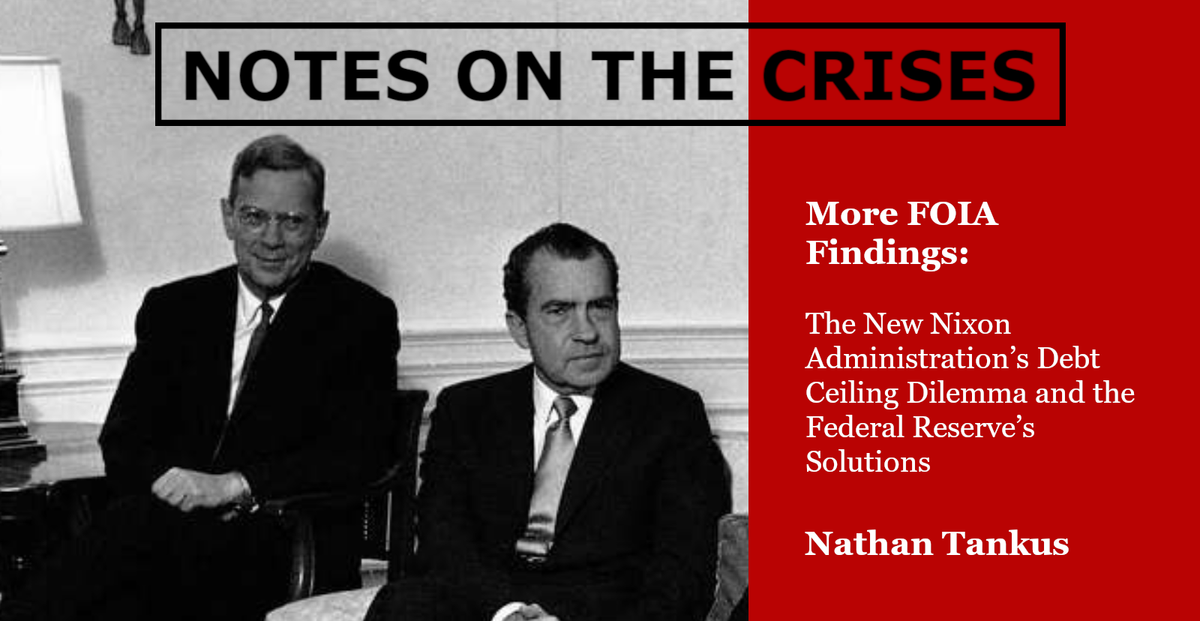

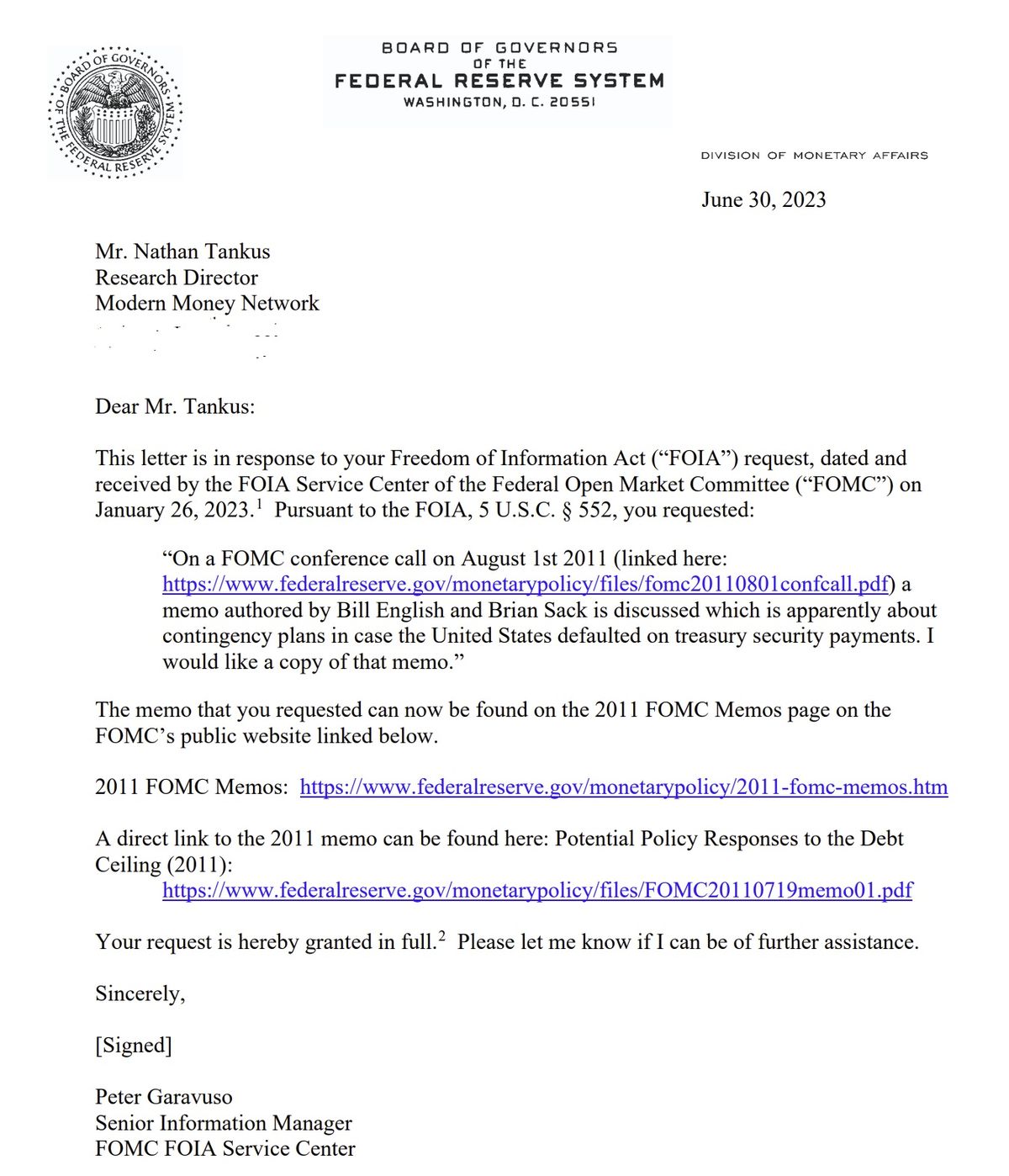

For the past year and a half I’ve increasingly focused on using FOIA to scrutinize the Federal Reserve. Before I unveil the crown jewel of what I’ve accomplished so far, I think it's worth stepping back and saying why I’ve undertaken such a broad project.| Notes on the Crises

Nobel Prize-winning economist Eugene Fama argues that Bitcoin is fundamentally flawed and predicts it has a near-certain chance of becoming worthless within a decade. In a conversation with Luigi Zingales and Bethany McLean, Fama explains why Bitcoin’s extreme volatility, lack of intrinsic value, and violation of basic monetary principles make its long-term survival unlikely. Eugene […]| ProMarket

The authors review how to gauge the ampleness of reserves in the banking system using a new Reserve Demand Elasticity measure, to be published monthly by the New York Fed.| Liberty Street Economics

A look at how well central banks and market participants understand each other’s expectations, featuring a model with a dynamic game.| Liberty Street Economics

Over the coming year, the Fed will be reviewing its framework for setting monetary policy. In their previous policy review, which wrapped up in August 2020, the Fed adjusted its framework to address the low-interest-rate environment of the 2010s. The past few years have of course presented the different set of challenges related to high … Continue reading Toward a more robust Federal Reserve policy framework→| John Roberts Macroeconomics

The dominant view of inflation holds that it is macroeconomic in origin and must always be tackled with macroeconomic tightening. In contrast, we argue that the US COVID-19 inflation is predominantly a sellers’ inflation that derives from microeconomic origins, namely the ability of firms with market power to hike prices. Such firms are price makers, but they only engage in price hikes if they expect their competitors to do the same. This requires an implicit agreement which can be coordina...| Elgar Online: The online content platform for Edward Elgar Publishing

I have a new note, co-authored with fellow Fed alum Steve Kamin, that asks “How Will the Interaction of Wages and Prices Play Out in the Last Mile of Disinflation?” We estimate a model of wage-pric…| John Roberts Macroeconomics

A look at the consequences of an aggressive policy response to inflation using a Heterogeneous Agent New Keynesian (HANK) model.| Liberty Street Economics

A look at the distributional effects of inflation and inflation stabilization using a Heterogeneous Agent New Keynesian (HANK) model.| Liberty Street Economics

SCOPING THE COMING CRISIS As you may know, the central contention of the Surplus Energy Economics thesis is the absolute necessity of thinking in terms of two economies. These are the “real” econom…| Surplus Energy Economics

Since taking office, the new government has replaced quite a number of chairs of government entities. I’m sure there are many others but NZTA, Health NZ, Pharmac, and the FMA are just the exa…| croaking cassandra

Nathan Tankus reveals seven secret books authored by a very important Federal Reserve general counsel that he unearthed through a Freedom of Information Act request| Notes on the Crises

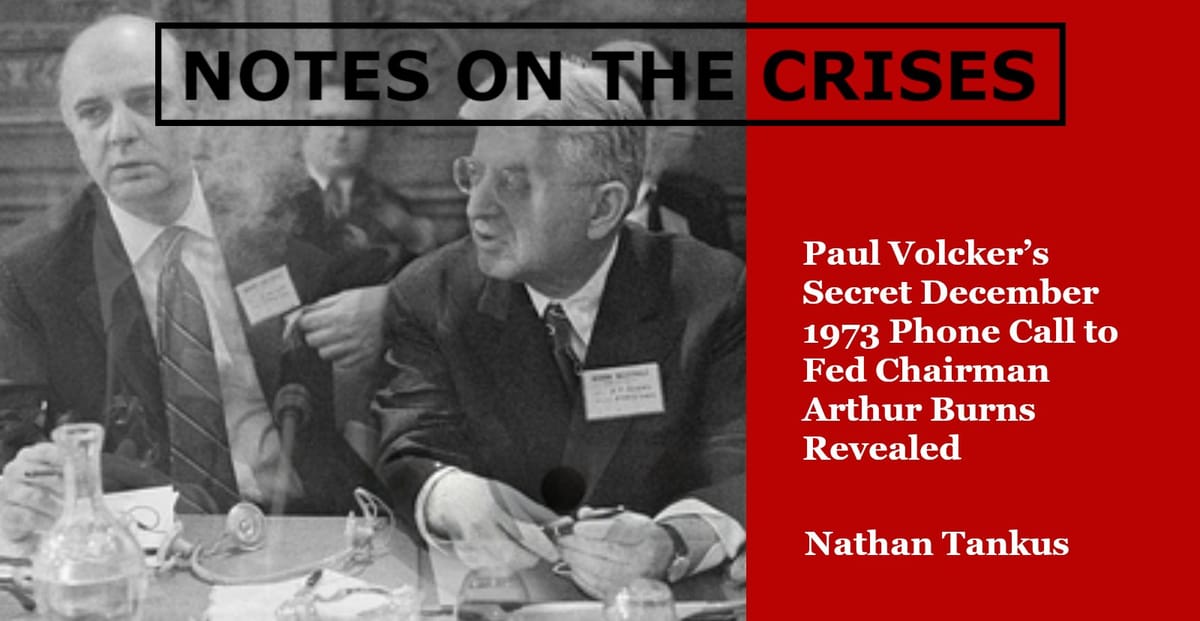

Nathan Tankus writes about a secret phone call between Paul Volcker and Federal Reserve Chairman Arthur Burns to save the Treasury from debt ceiling driven default| Notes on the Crises

In my previous post, I explained how the real-bills doctrine originally espoused by Adam Smith was later misunderstood and misapplied as a policy guide for central banking, not, as Smith understood…| Uneasy Money

This post is the latest of a series that uses a small-scale macroeconomic model to interpret the latest edition of the Federal Open Market Committee’s Summary of Economic Projections; here’s a link…| John Roberts Macroeconomics

Nathan Tankus covers his latest FOIA finding from the Federal Reserve regarding its response to Treasury debt ceiling struggles in 1968| Notes on the Crises

Subscribe Readers may recall that I wrote a Politico Op Ed at a critical moment in the debt ceiling showdown. That piece, was entitled “Biden Can Steamroll Republicans on the Debt Ceiling”, and I aimed squarely at debunking the idea that the Federal Reserve would step on any “unilateral actions”| Notes on the Crises

Line goes down, and up. Last week, I wrote out a post arguing that the inflation problem is largely over, and the Fed had little to do with it. Yesterday, the new CPI numbers were released and they showed a sharp rise in inflation — a 4 percent rate over the past three months, compared with 2 percent when I wrote the piece.| J. W. Mason

The central banking cartel has overseen the greatest hustle in human history. The curtain is about to be pulled back on its consequences.| Hustle Escape