Editor’s Note — We are republishing this deep dive essay, which was initially published in October of 2024. If anything, the topic (the importance of balanced BaaS partnerships) has become even more relevant, and the essay has been updated to reflect this. My thanks to Fifth Third Bank for sponsoring this deep dive essay and […] The post Building Sustainable Bank-Fintech Partnerships appeared first on Fintech Takes.| Fintech Takes

I’ll be honest with you. Of all the terms I run across in my job, one of the ones that I understand the least is customer lifetime value, or LTV for short. And yet … the term is essential to understanding the recent past and, more importantly, the future of fintech and banking. Every company […]| Fintech Takes

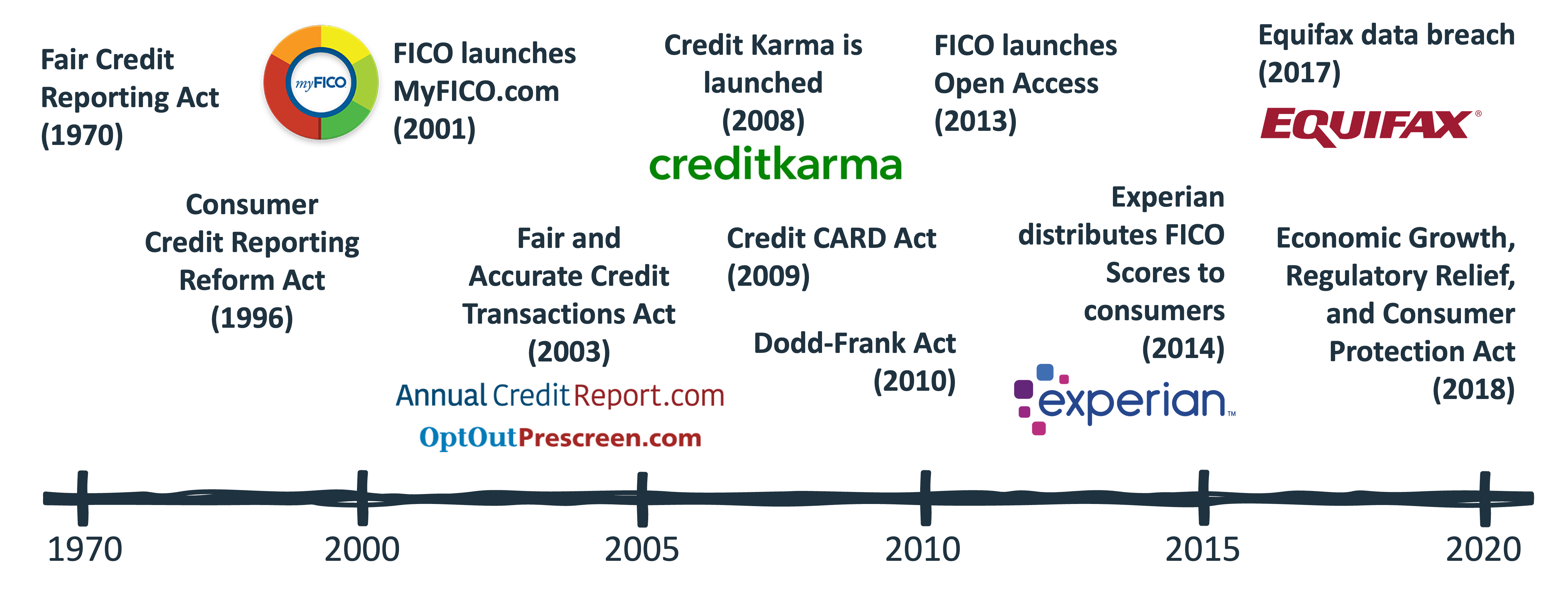

Editor’s Note — This article is sponsored by SOLO (and just so you know, I also do some advising work for them, which is totally unrelated to this piece, but just FYI.) As with all sponsored content in Fintech Takes, this article was written, edited, and published by me, Alex Johnson. I hope you enjoy […] The post How Would You Design a Credit Bureau in 2025? appeared first on Fintech Takes.| Fintech Takes

Editor’s Note — This article is sponsored by Byline Bank. As with all sponsored content in Fintech Takes, this article was written, edited, and published by me, Alex Johnson. I hope you enjoy it! Five years ago, fintech founders treated the search for bank partners the same way that they treated the search for every […]| Fintech Takes

Last month, I spoke at an event hosted by the Federal Reserve. The theme of the event was “Unleashing a Financially Inclusive Future”. Within the first 15 minutes of my panel, we hit upon a key idea: “inclusion” might not be the right word to describe the problem that we are dealing with. After all, […]| Fintech Takes

Editor’s Note — This article is sponsored by Marqeta. As with all sponsored content in Fintech Takes, this article was written, edited, and published by me, Alex Johnson. I hope you enjoy it! The interesting thing about embedded finance is that not all aspects of embedded finance are created equal. Take payments as an example. […]| Fintech Takes

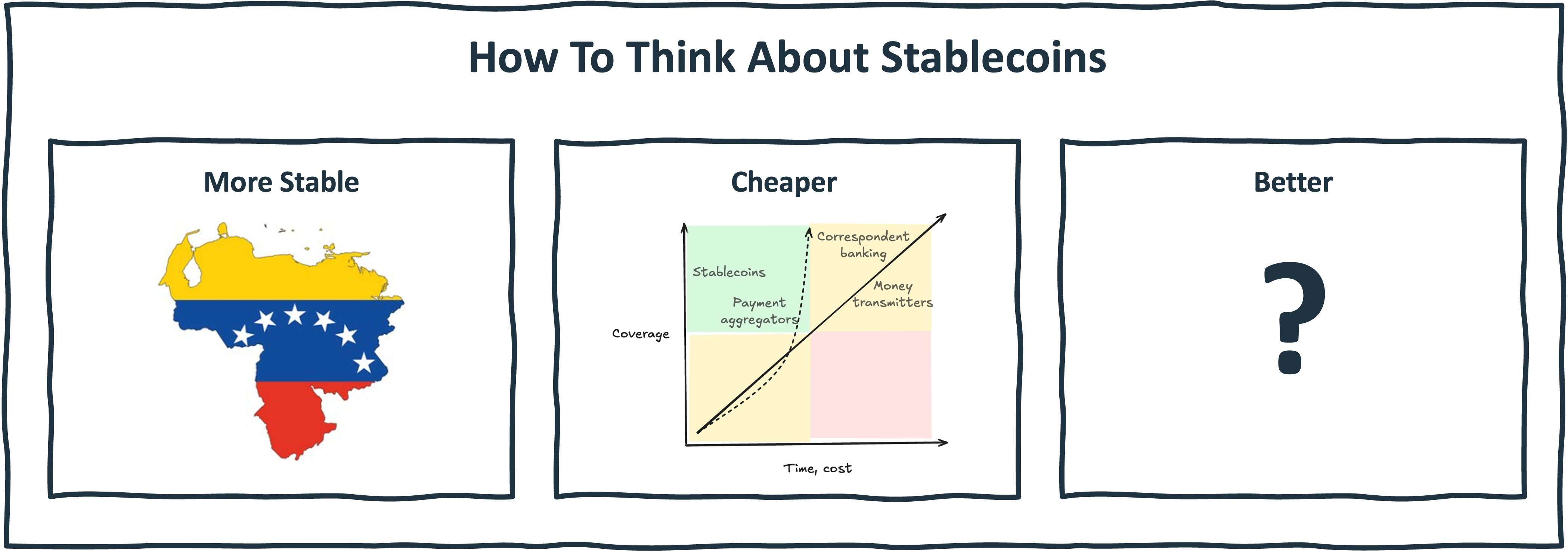

Stablecoins are the topic du jour in fintech (or the topic du semestre, to be more precise). I usually try not to follow the crowd when it comes to topic selection for the newsletter. However, as I wrote about a month ago, crypto enthusiasts are starting to use the reputation of stablecoins (safe! low cost!) […]| Fintech Takes

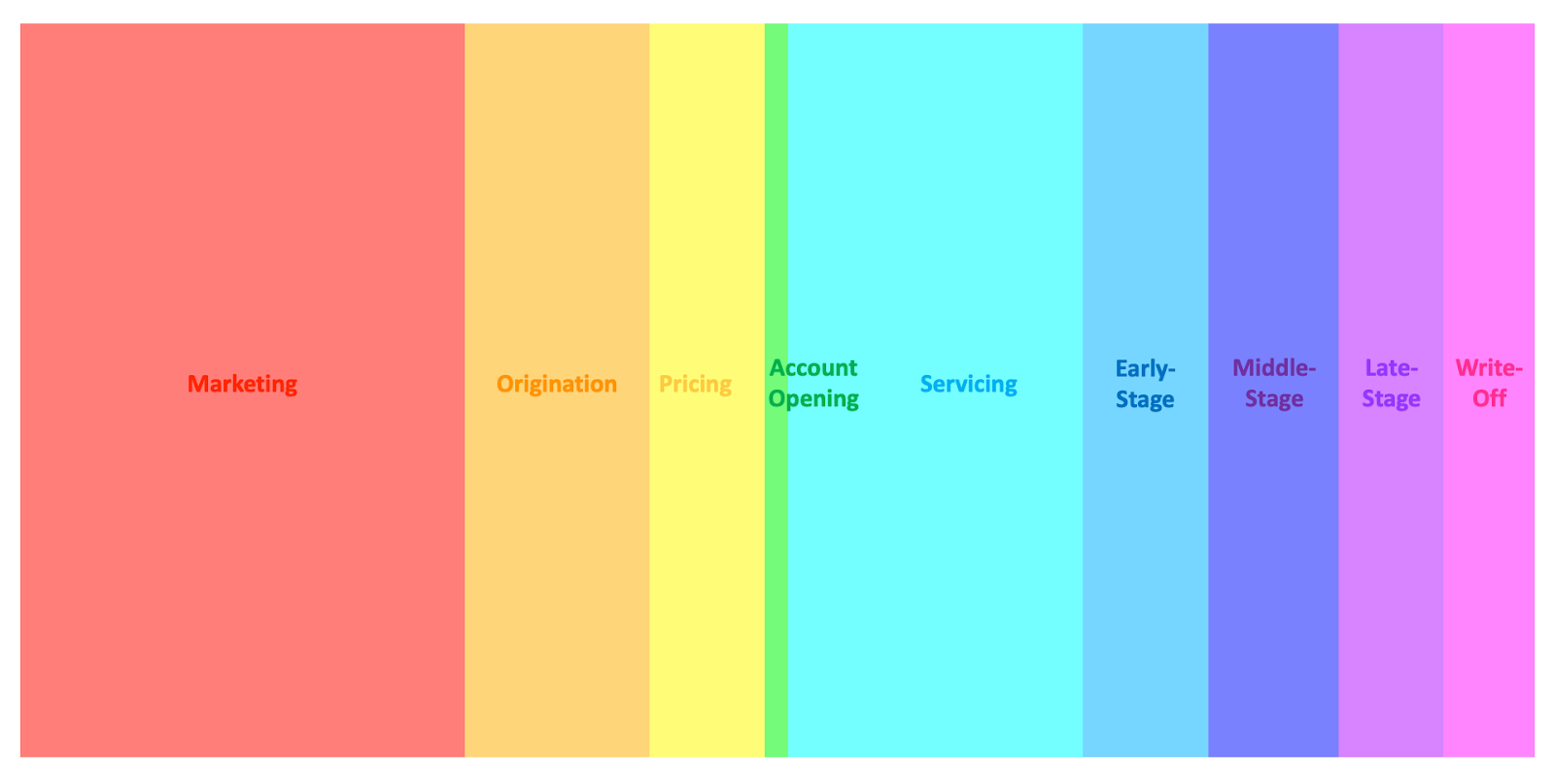

Lending is a relationship business. However, I believe one of the enduring frustrations in lending is that consumers and lenders are rarely in the same place in the relationship at the same time. Think about the consumer credit lifecycle. You start out in marketing. Consumers sift through a range of similar-looking options via comparison sites […]| Fintech Takes

We should start by saying the use of cash flow data in lending is not new. Perhaps the two most obvious questions to ask when considering whether or not to loan someone money are, “How much money do you have today?” and “How much money will you have in two weeks?” Lenders have been asking […]| Fintech Takes

3 Fintech News Stories #1: Bilt isn’t a Unicorn What happened? Bilt is in talks to raise a new round of funding at a $10 billion valuation. Lucinda Shen at Axios reports: Rent rewards startup Bilt is in talks to raise at a roughly $10 billion valuation, in a round likely to be led by […] The post Bilt isn’t a Unicorn appeared first on Fintech Takes.| Fintech Takes

I love disaster movies. I love them so much. I love them to the degree that my wife mocks me for it, which is fair because some of them are truly terrible (looking at you, Moonfall). But many of them are good! And very entertaining! And one has become an annual tradition in my household: […] The post Independence Day appeared first on Fintech Takes.| Fintech Takes

There’s something poetic about Chime’s newest commercial, featuring former NBA star, coach, and TV announcer Mark Jackson. Depending on your point of view, you might think of Mark Jackson as an indelible part of recent basketball history; a great player with a sneakily influential style, an important coach who helped nudge the Warriors towards their […]| Fintech Takes

An hour before a scheduled procedural vote in the U.S. Senate on the GENIUS Act, which would establish a federal regulatory framework for stablecoins, the President and CEO of the Independent Community Bankers of America (ICBA), Rebeca Romero Rainey, issued a statement. The statement begins: On behalf of the nation’s community bankers, ICBA urges the […]| Fintech Takes

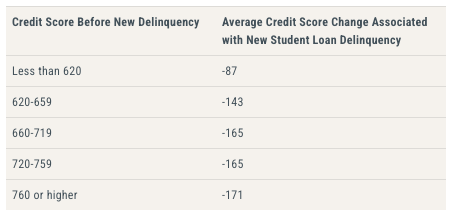

According to the New York Fed’s Liberty Street Economics blog, more than 9 million student loan borrowers will soon start to see substantial declines in their credit scores. Those declines will be larger for higher-score segments, with those in the 760 – 850 range seeing an average drop of 171 points: That’s a big deal. […]| Fintech Takes

Lawyers and accountants might disagree with this statement, but I’ve always thought that the process of becoming a public company is, primarily, a storytelling exercise. You are trying to engineer the best possible response from public market investors while complying with all the regulatory requirements for accurate business and financial reporting, which requires a very […]| Fintech Takes

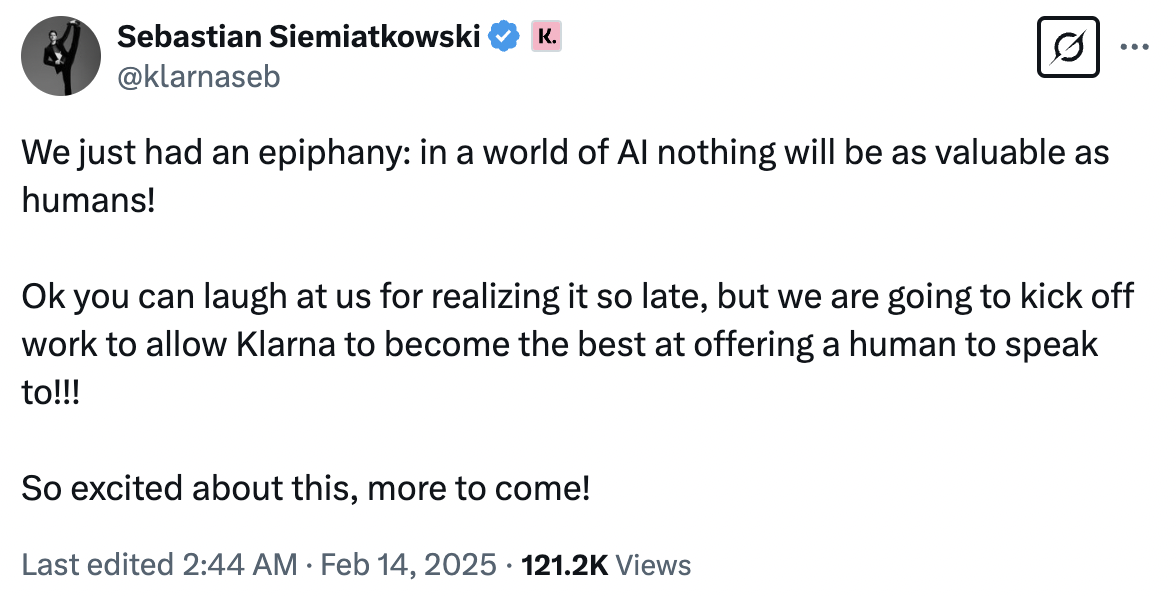

3 Fintech News Stories #1: $KLAR What happened? Exciting times for Klarna! The company has filed the paperwork to go public: Klarna, a provider of buy now, pay later loans filed its IPO prospectus on Friday, and plans to go public on the New York Stock Exchange under ticker symbol KLAR. Klarna, headquartered in Sweden, […]| Fintech Takes

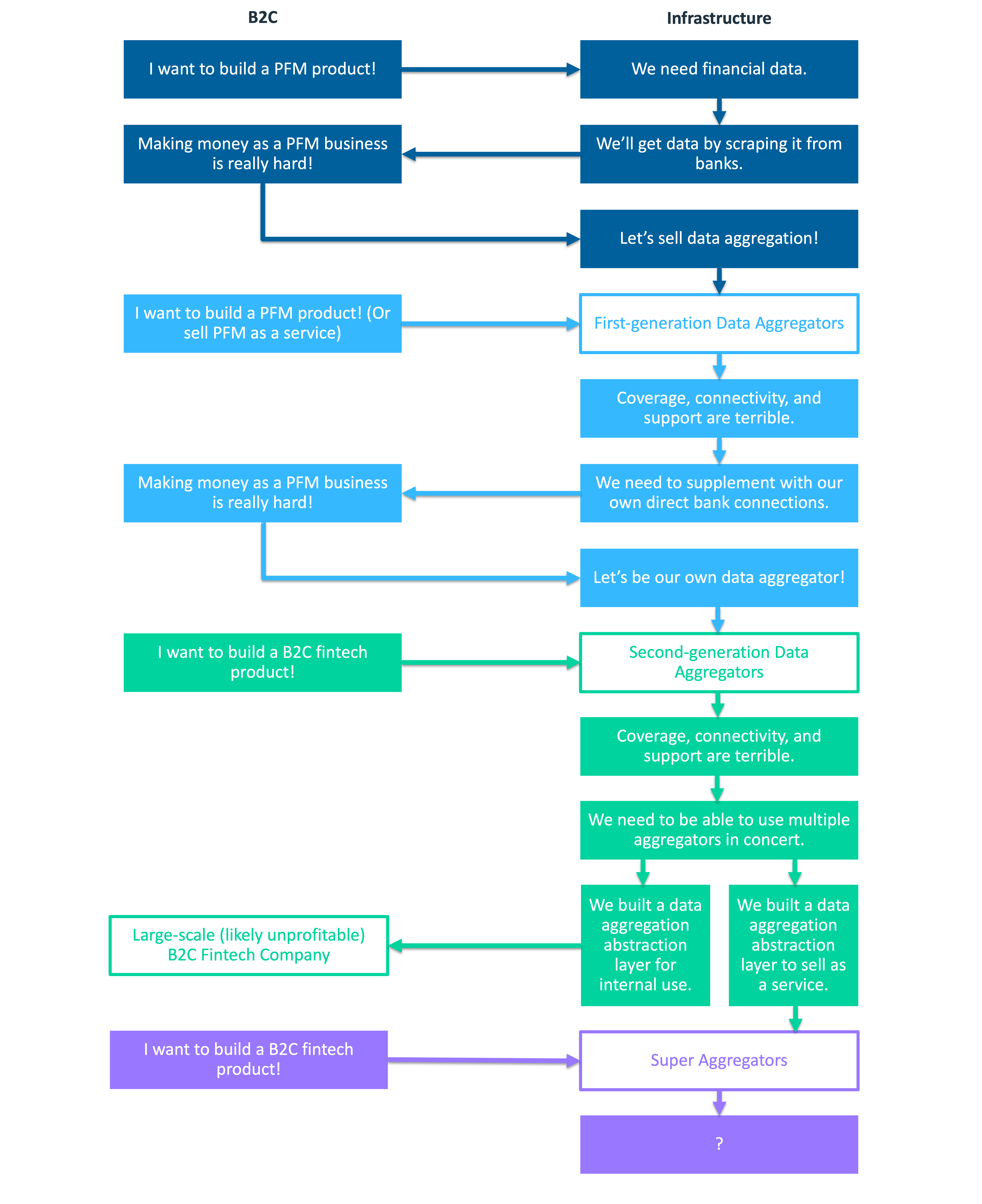

My first job in fintech, which I got 20 years ago this month, was with a company that provided credit decisioning software to banks. One of the features of that software product, which I didn’t give a whole lot of thought to at the time, was data aggregation. When a bank was making a credit […]| Fintech Takes

I have reached a stage in my life where I have very little need for my credit reports. I am paying a mortgage on what I hope is my forever home. I have a minivan that I am planning to drive into the ground (this is a flex … listen to this podcast for the […]| Fintech Takes

The fundamental problem with banking as a service (BaaS) is that in order for it to work, every participant in the value chain needs to do their job with more diligence than they are required to do. For the most part, this hasn’t been an issue. Fintech is filled with founders and operators who care […]| Fintech Takes

3 FINTECH NEWS STORIES #1: The Difference Between a Bank and a Network What happened? Capital One is teaming up with Stripe and Adyen: While Capital One has built models to protect its customers from fraud, it was getting stuck because it just “didn’t have enough data,” said head of fraud strategy Jon Borman. So […]| Fintech Takes