Flat Tax Revolution: State Income Tax Reform | Tax Foundation

The past four years have brought significant focus on state income tax reform and relief, and with that, something of a flat tax revolution.| Tax Foundation

The 2017 Tax Cuts and Jobs Act (TCJA) simultaneously increased tax progressivity and decreased redistribution in the tax code. Our estimates suggest the OBBBA similarly combines a more progressive tax system with a lower degree of tax redistribution.| Tax Foundation

New evidence shows the scale and distribution of compliance costs for EU firms affected by Pillar Two, i.e., the “Global Minimum Tax."| Tax Foundation

Amidst a government shutdown, healthcare subsidies have metastasized into a major threat to the nation’s fiscal and economic health.| Tax Foundation

Sean Bray interviewed Dr. Sérgio Vasques, Professor of Tax Law at the Catholic University of Lisbon and former Portuguese Secretary of State for Tax Affairs, about the future of the EU tax mix.| Tax Foundation

The most effective way to tax alcoholic beverages is to tax according to alcohol content, rather than beverage type.| Tax Foundation

Several goods have experienced notably large price increases, including apparel, coffee and tea, cameras, and furniture.| Tax Foundation

While there are many factors that affect a country's economic performance, taxes play an important role. A well-structured tax code is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities.| Tax Foundation

Since digital services taxes deliver limited revenue, shift the burden to European consumers, and risk provoking trade disputes, it’s time for policymakers to rethink their approach.| Tax Foundation

When property values soar, homeowners can end up paying significantly higher taxes for basically the same services. Thankfully, there is a solution.| Tax Foundation

Join us on Thursday, 19 March 2026 for Tax Foundation Europe’s inaugural Conference and Gala.| Tax Foundation

The past four years have brought significant focus on state income tax reform and relief, and with that, something of a flat tax revolution.| Tax Foundation

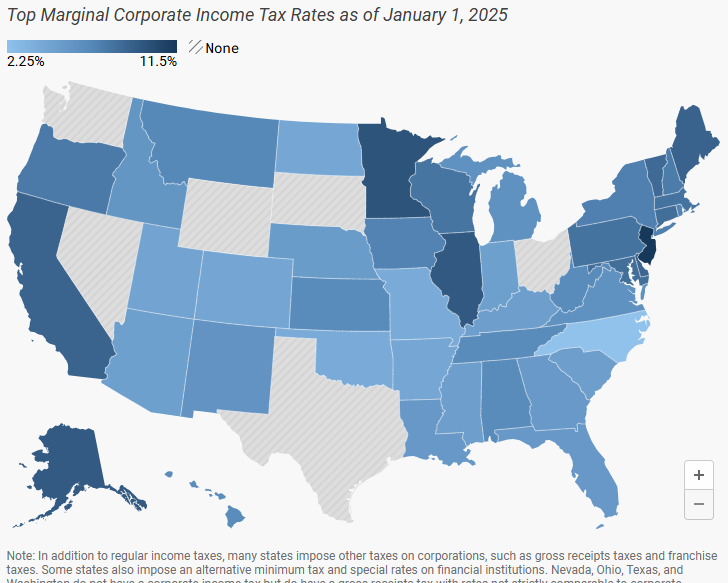

Forty-four states levy a corporate income tax, with top rates ranging from a 2.25 percent flat rate in North Carolina to a 11.5 percent top marginal rate in New Jersey.| Tax Foundation

The One Big Beautiful Bill Act (OBBBA) significantly alters the Inflation Reduction Act (IRA) green energy subsidies.| Tax Foundation

A regressive tax is one where the average tax burden decreases with income. Low-income taxpayers pay a disproportionate share of the tax burden, while middle- and high-income taxpayers shoulder a relatively small tax burden.| Tax Foundation

Rather than relying on damaging corporate tax hikes, policymakers should consider user fees and consumption taxes as options for financing new infrastructure to ensure that a compromise does not end up being a net negative for the U.S. economy.| Tax Foundation

Taxing cannabis is brand-new territory. While many states see recreational cannabis as a potential gold mine for tax revenue, the reality is more complicated.| Tax Foundation

A carbon tax is levied on the carbon content of fossil fuels. The term can also refer to taxing other types of greenhouse gas emissions, such as methane| Tax Foundation

Despite the potential of consumption taxes as a neutral and efficient source of tax revenues, many governments have implemented policies that are unduly complex and have poorly designed tax bases that exclude many goods or services from taxation, or tax them at reduced rates.| Tax Foundation

Designing tax policy in a way that sustainably finances government activities while minimizing distortions is important for supporting a productive economy.| Tax Foundation

The fiscal fight that resulted in the current federal government shutdown is, at its core, about the healthcare sector, spiraling healthcare costs, and federal subsidies.| Tax Foundation

Explore the IRS inflation-adjusted 2026 tax brackets, for which taxpayers will file tax returns in early 2027.| Tax Foundation

Sean Bray interviewed Professor of Tax Law at the Lisbon School of Law of the Catholic University of Portugal, Dr. Miguel Correia, about the future of the EU tax mix.| Tax Foundation

With property tax bills on the rise, homeowners are searching for answers—and some even want to abolish the tax altogether. In this episode, we break down why property taxes are increasing, common but flawed solutions, and why the property tax remains an economically efficient revenue source.| Tax Foundation

Excise taxes generate more than two trillion dollars worldwide each year. While tying an excise tax revenue source to a specific expenditure program can be a best practice, the efficiency depends on the revenue source, the spending program, and why the excise tax was implemented in the first place.| Tax Foundation

Taxing carbon emissions could leave decisions about reducing greenhouse gases to the market.| Tax Foundation

Backfilling forgone local property tax revenue through new state taxes is difficult because it dramatically shifts overall tax burdens, undermines local accountability, and cannot easily adjust for changing population mixes.| Tax Foundation

Public health organizations continue to push for excise taxes on sugar-sweetened beverages (SSBs). Several governments around the globe already levy an excise tax on sugary beverages.| Tax Foundation

Canada has the power to shape its own competitiveness by making itself an attractive destination for investment this 2025 budget season.| Tax Foundation

High property taxes levied not only on land but also on buildings and structures can discourage investment in infrastructure, which businesses would have to pay additional tax on.| Tax Foundation

With inflation continuing to skyrocket, especially for food, which reached 10.4 percent in June, it is worth examining how the ongoing U.S. trade war with China and U.S. tariff policy overall has impacted U.S. agriculture and food prices.| Tax Foundation

In each of its main research areas, the Tax Foundation produces timely and high-quality data, research, and analysis that influence the tax debate toward policies that are simple, transparent, neutral, and stable. Meet Our Experts Our experts are continuously analyzing the day’s most relevant tax policy topics and are relied upon routinely for presentations, […]| Tax Foundation

Universal savings accounts could be a simpler solution to many countries’ systems of private retirement savings investment tax treatment.| Tax Foundation

The US Supreme Court will hear oral arguments on November 5, to determine whether the President’s emergency powers under the International Emergency Economic Powers Act (IEEPA) include the power to impose tariffs.| Tax Foundation

A tax refund is a reimbursement to taxpayers who have overpaid their taxes, often due to having employers withhold too much from paychecks. The U.S. Treasury estimates that nearly three-fourths of taxpayers are over-withheld, resulting in tax refunds. Overpaying taxes can be viewed as an interest-free loan to the government.| Tax Foundation

Payroll taxes are taxes paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance.| Tax Foundation

The Earned Income Tax Credit (EITC) is a refundable tax credit targeted at low-income working families. The credit offsets tax liability, and can even generate a refund, with EITC amounts calculated on the basis of income and number of children.| Tax Foundation

Adjusted gross income (AGI) is a taxpayer’s total income minus certain “above-the-line” deductions. It is a broad measure that includes income from wages, salaries, interest, dividends, retirement income, Social Security benefits, capital gains, business, and other sources, and subtracts specific deductions.| Tax Foundation

The Earned Income Tax Credit (EITC) is a refundable tax credit targeted at low-income workers. Learn more about the EITC and Child Tax Credit.| Tax Foundation

Wireless consumers continue to be burdened with high taxes, fees, and government surcharges in many states and localities throughout the country.| Tax Foundation

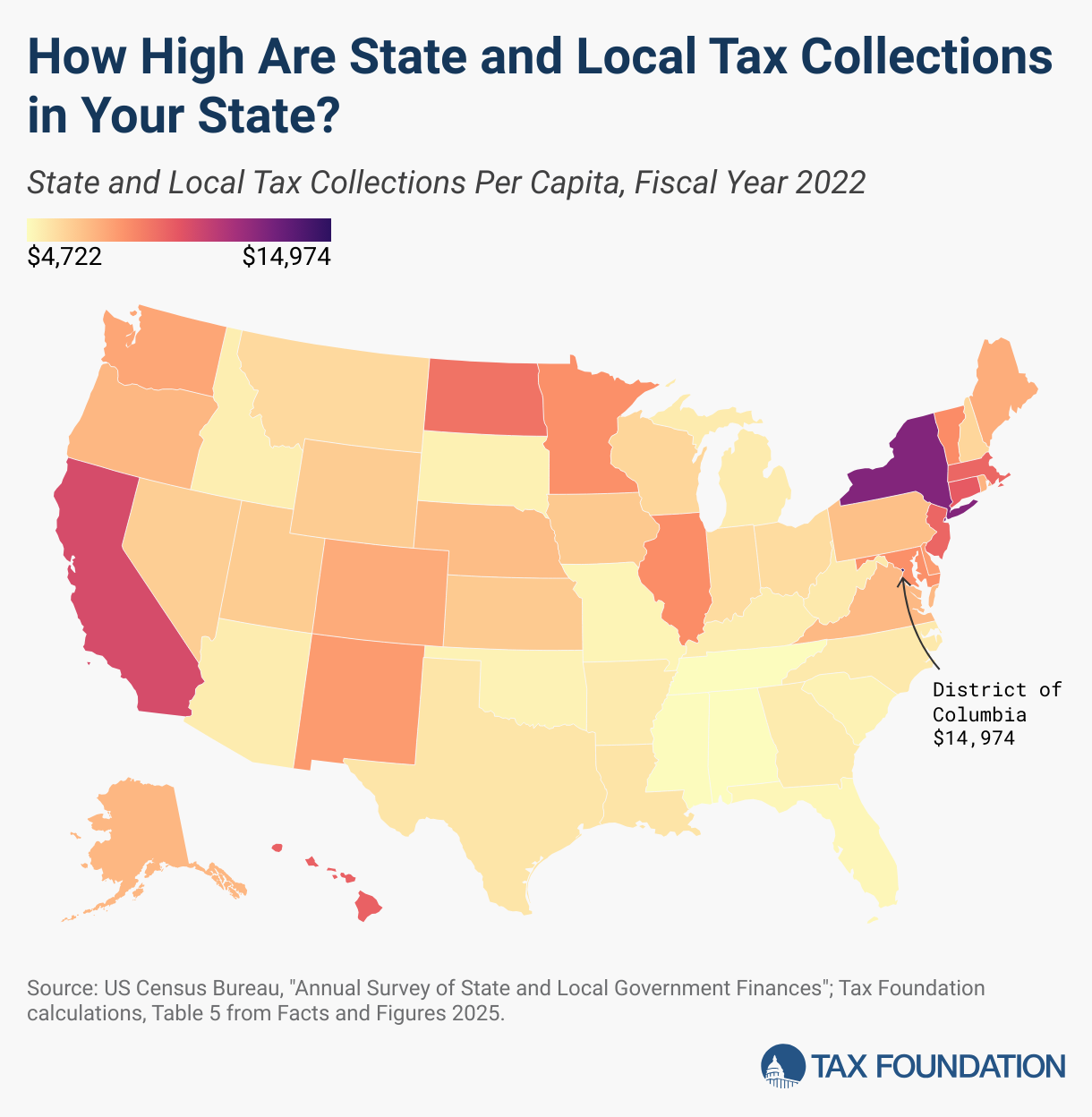

According to the latest economic data from the US Census Bureau, the average per capita state and local tax burden is $7,109. However, collections vary widely by state, reflecting differences in tax rates and bases, natural resource endowments, the scale and scope of taxable economic activity in each state, and residents’ political preferences.| Tax Foundation

The US fiscal trajectory is on an unsustainable path over the next 35 years, regardless of whether the IEEPA tariffs are struck down or maintained.| Tax Foundation

Football players facing off in Brazil will owe an estimated $1.04 million in nonresident income tax on the share of income they earned there.| Tax Foundation

Republican policymakers in Congress are considering options to raise revenue as part of their expected legislative package in 2025. One such option involves raising the tax rate on university endowments first put in place as part of the TCJA in 2017.| Tax Foundation

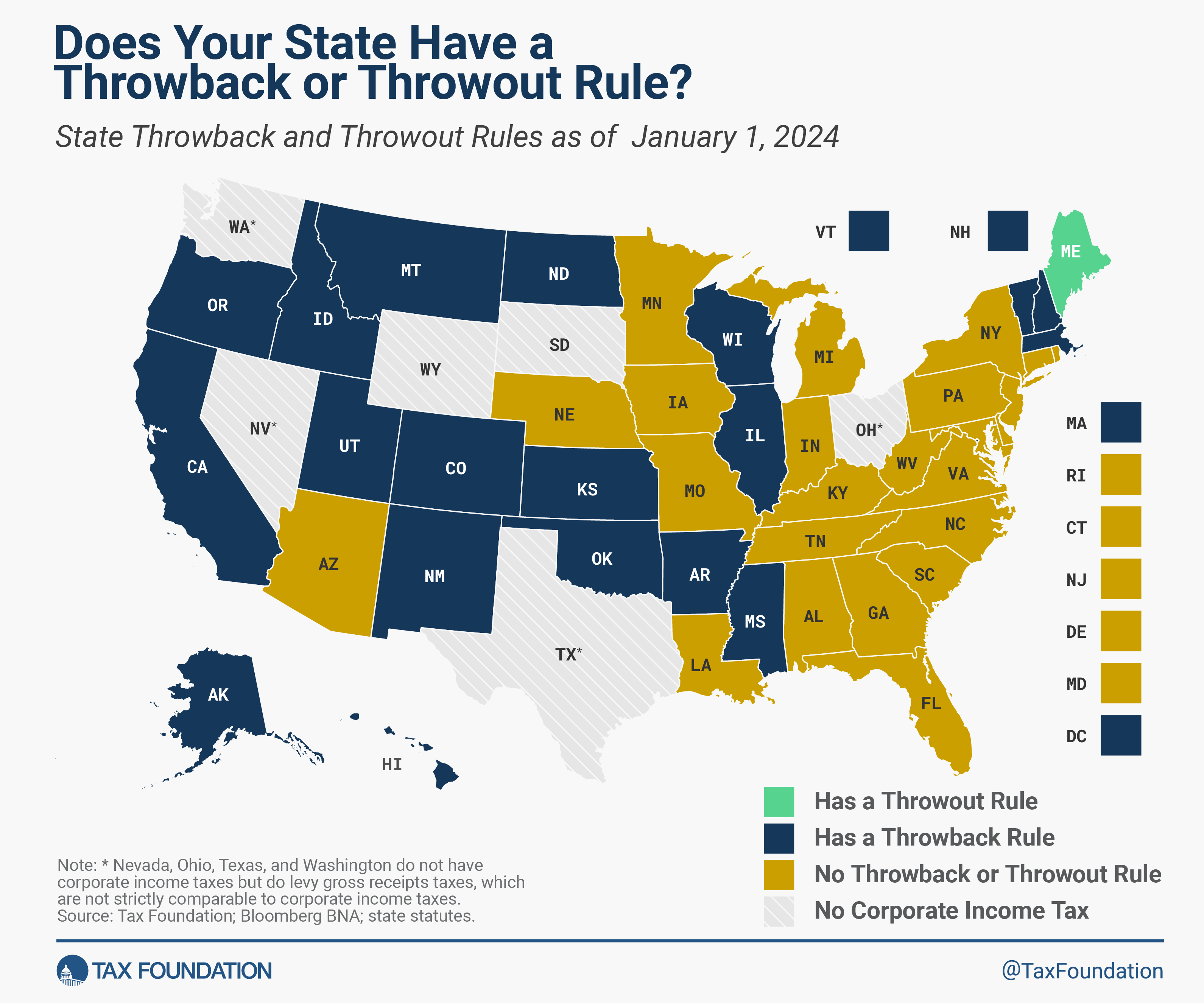

States have generally tried to encourage capital investment. Throwback and throwout rules are an unfortunate example of penalizing it.| Tax Foundation

Individual income taxes are a major source of state government revenue, accounting for more than a third of state tax collections. How do income taxes compare in your state?| Tax Foundation

With state tax revenues receding from all-time highs, there’s been a great deal of handwringing about whether states can afford the tax cuts adopted over the past few years. Given that 27 states reduced the rate of a major tax between 2021 and 2023, is there reason for concern?| Tax Foundation

Former President Donald Trump would like to push for a reduction in the federal corporate tax rate from 21 percent to 15 percent if reelected.| Tax Foundation

In a surprising tax code alteration that has frustrated Americans who enjoy gambling, a provision in the One Big Beautiful Bill Act limits gambling losses that can be used to offset gambling winnings to 90 percent of their value. This provision introduces a steep tax penalty for professional gamblers and certain casual bettors.| Tax Foundation

The tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.| Tax Foundation

A consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an income tax where all savings is tax-deductible.| Tax Foundation

Explore United States tax data, including tax rates, collections, burdens, and more.| Tax Foundation

Gross receipts taxes, by their very design, lack transparency. Our report explores the pros and cons of a turnover tax, also known as a gross receipts tax.| Tax Foundation

New IRS data shows the US federal income tax system continues to be progressive as high-income taxpayers pay the highest average income tax rates. Average tax rates for all income groups remain lower after the Tax Cuts and Jobs Act (TCJA).| Tax Foundation

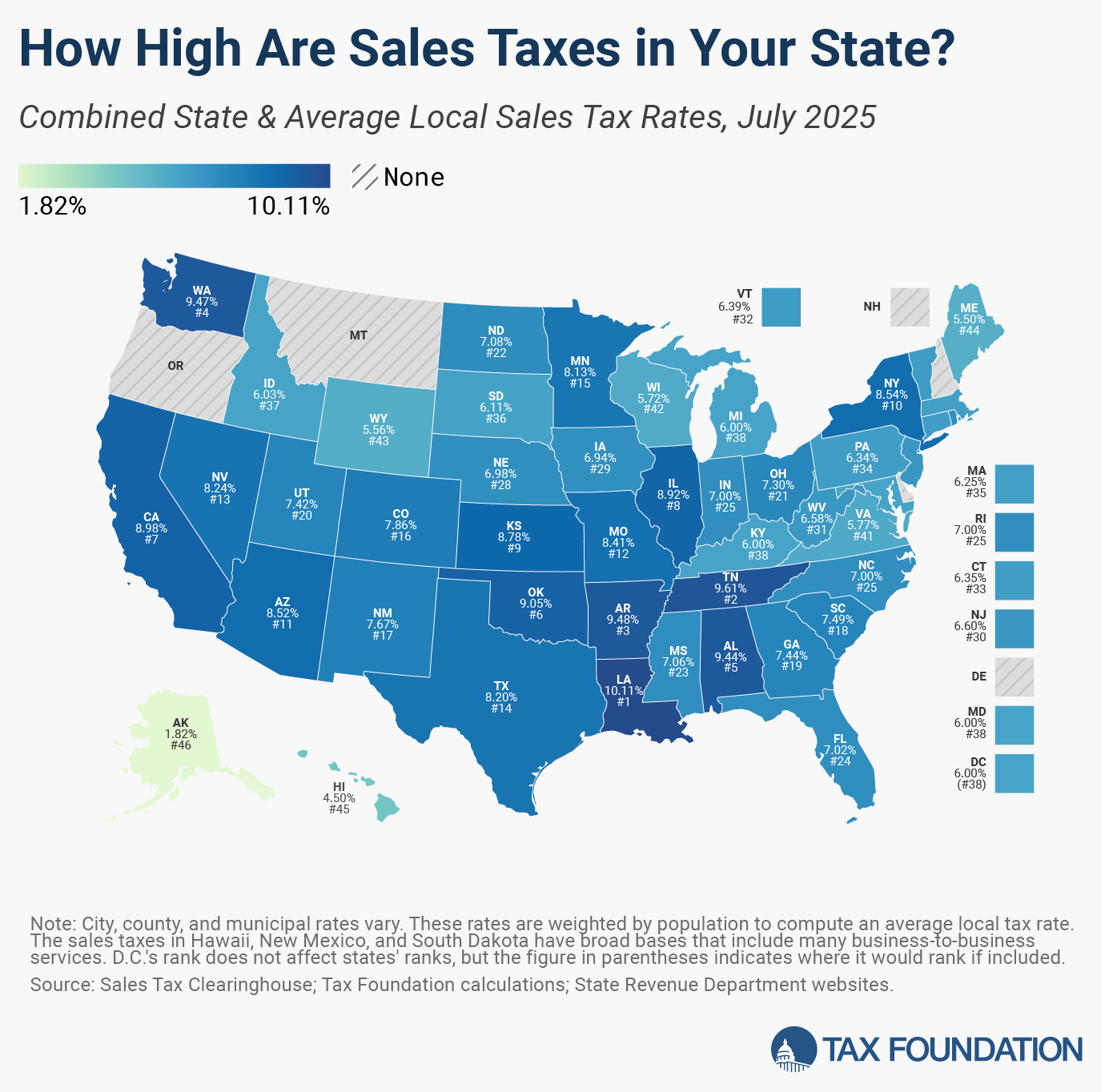

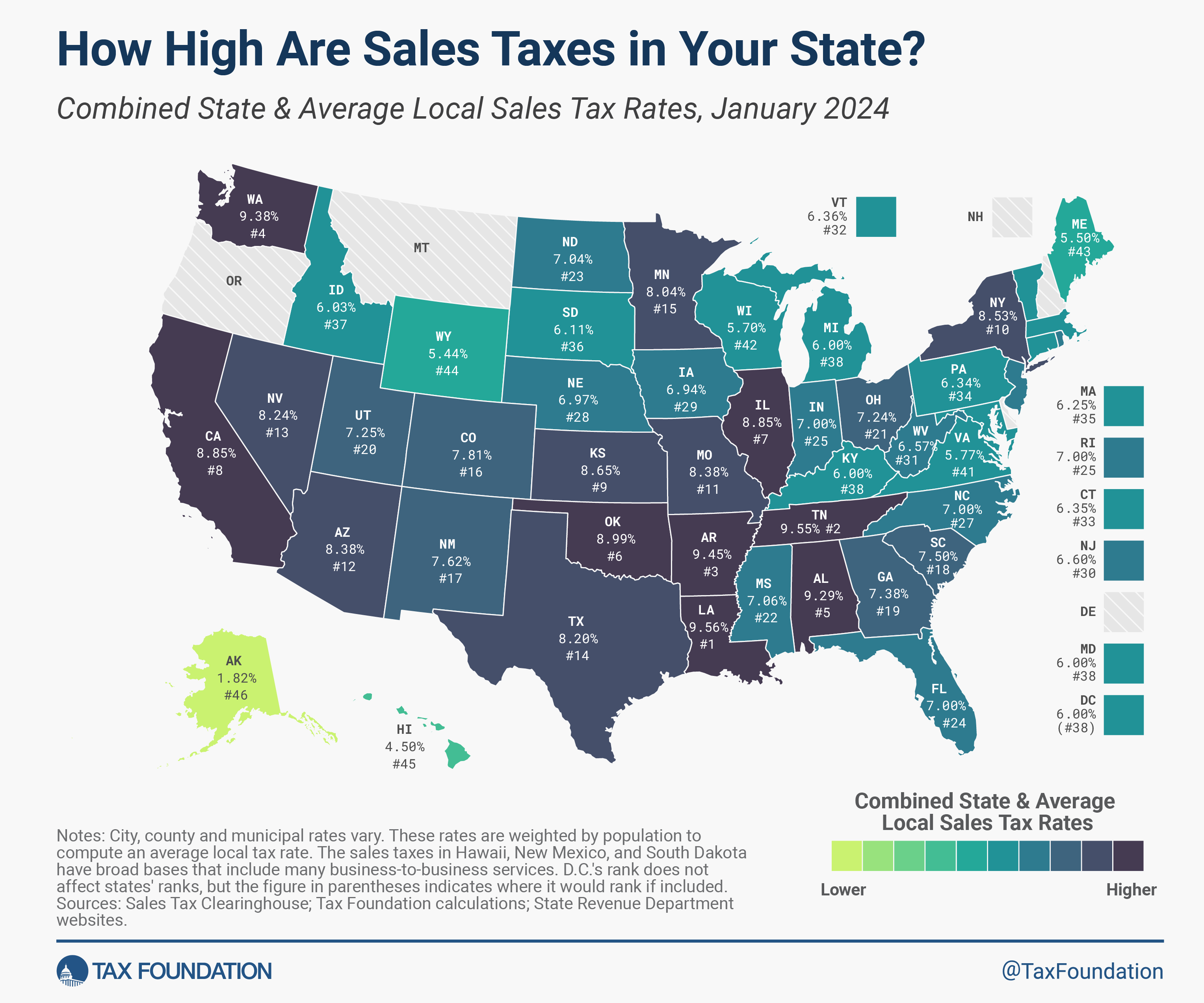

The sales tax is the second-largest source of state tax revenue and an important source of local tax revenue, but decades of base erosion threaten the tax’s share of overall revenue and have prompted years of countervailing rate increases.| Tax Foundation

Explore Wisconsin tax data, including tax rates, collections, burdens, and more.| Tax Foundation

Explore Washington tax data, including tax rates, collections, burdens, and more.| Tax Foundation

Explore Tennessee tax data, including tax rates, collections, burdens, and more.| Tax Foundation

Explore Louisiana tax data, including tax rates, collections, burdens, and more.| Tax Foundation

Explore Florida tax data, including tax rates, collections, burdens, and more.| Tax Foundation

Inflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. Inflation is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.| Tax Foundation

Gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.”| Tax Foundation

Explore our latest tax policy research, analysis, and commentary of the One Big Beautiful Bill Act (OBBB). Learn more from Tax Foundation's experts.| Tax Foundation

Across all individual tax filers throughout the US, the average tax cut per taxpayer will be over $3,700 in 2026.| Tax Foundation

Growing cigarette tax levels and differentials have made cigarette smuggling both a national problem and a lucrative criminal enterprise.| Tax Foundation

Our Center for Federal Tax Policy promotes policies that lead to greater U.S. competitiveness, economic growth, and improved quality of life.| Tax Foundation

The Joint Committee on Taxation (JCT) is a nonpartisan congressional committee in the United States that assists both the House and Senate with tax legislation.| Tax Foundation

How have federal tax expenditures changed since passage of the Tax Cuts and Jobs Act? We compare 2017 and 2018 Joint Committee on Taxation estimates.| Tax Foundation

The Tax Cuts and Jobs Act created a deduction for households with income from sole proprietorships, partnerships, and S corporations, which allows taxpayers to exclude up to 20 percent of their pass-through business income from federal income tax. For upper-income taxpayers, the deduction is subject to several limits.| Tax Foundation

Tax Foundation experts regularly testify before the US Congress, in US statehouses, and in government institutions throughout Europe.| Tax Foundation

The poor revenue performance of Philadelphia’s soda tax, 24 times the rate on beer, threatens the education programs it was intended to fund.| Tax Foundation

A property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment.| Tax Foundation

Nebraska has an opportunity to revise the property tax package enacted in 2024 to ensure that Nebraskans enjoy meaningful property tax relief.| Tax Foundation

With such an important change to Iowa’s property tax system, it’s important that lawmakers get the details right.| Tax Foundation

The mix of tax sources states choose can have important implications for both revenue stability and economic growth, and the many variations across states are indicative of the different ways states weigh competing policy goals.| Tax Foundation

Property taxes are the primary tool for financing local governments. While no taxpayers in high-tax jurisdictions will be celebrating their yearly payments, property taxes are largely rooted in the benefit principle of taxation: the people paying the property tax bills are most often the ones benefiting from the services.| Tax Foundation

Montana’s 2025 legislative session has seen a flurry of property tax reform proposals, a response to the surge in property valuations in the state. Unfortunately, hasty decision-making can result in suboptimal policy outcomes.| Tax Foundation

This legislative session, local taxes are a major topic of debate in Indiana. Although the state’s property tax system is already nationally competitive, dramatic increases in assessed values have created discontent in recent years.| Tax Foundation

Our Center for State Tax Policy promotes policies that lead to higher economic growth and improved quality of life for taxpayers in US states| Tax Foundation

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.| Tax Foundation

Our experts explain how this major tax legislation may affect you and how policymakers can better improve the tax code.| Tax Foundation

Oklahoma can continue to enhance its competitiveness by pursuing a variety of reforms to the corporate and individual income tax, but it should avoid policies that would negatively impact the economy, like enacting a wholesale elimination of the property tax.| Tax Foundation

Explore Georgia tax data, including tax rates, collections, burdens, and more.| Tax Foundation

If the federal government really wanted to make saving more accessible for taxpayers, it would swap the proposal for Trump Accounts to replace the complicated mess of savings accounts currently available with universal savings accounts.| Tax Foundation

A user fee is a charge imposed by the government for the primary purpose of covering the cost of providing a service, directly raising funds from the people who benefit from the particular public good or service being provided. A user fee is not a tax, though some taxes may be labeled as user fees or closely resemble them.| Tax Foundation

An externality, in economics terms, is a side effect or consequence of an activity that is not reflected in the cost of that activity, and not primarily borne by those directly involved in said activity. Externalities can be caused by either production or consumption of a good or service and can be positive or negative.| Tax Foundation

Different taxes have different economic effects, so policymakers should always consider how tax revenue is raised and not just how much is raised.| Tax Foundation

A refundable tax credit can be used to generate a federal tax refund larger than the amount of tax paid throughout the year. In other words, a refundable tax credit creates the possibility of a negative federal tax liability. An example of a refundable tax credit is the Earned Income Tax Credit.| Tax Foundation

The federal child tax credit (CTC) is a partially refundable credit that allows low- and moderate-income families to reduce their tax liability dollar-for-dollar by up to $2,000 for each qualifying child.| Tax Foundation

Exempting overtime would unnecessarily complicate the tax code, increase compliance and administrative costs, and reduce neutrality by favoring certain work arrangements over others.| Tax Foundation

We estimate the One Big Beautiful Bill Act would increase long-run GDP by 1.2 percent and reduce federal tax revenue by $5 trillion over the next decade on a conventional basis.| Tax Foundation

The House "One Big Beautiful Bill" includes a new 3.5 percent tax on remittances, or non-commercial transfers of money that people in the US send to people abroad.| Tax Foundation

Our preliminary analysis finds the tax provisions increase long-run GDP by 0.8 percent and reduce federal tax revenue by $4.0 trillion from 2025 through 2034 on a conventional basis before added interest costs.| Tax Foundation

Policymakers have passed legislation to extend many provisions of the 2017 Tax Cuts and Jobs Act (TCJA) alongside dozens of new tax provisions.| Tax Foundation

The principles of sound tax policy should serve as touchstones for policymakers everywhere. See Tax Foundation principles.| Tax Foundation

A gross receipts tax is applied to a company’s gross sales, without deductions for a firm’s business expenses, like costs of goods sold and compensation. Unlike a sales tax, a gross receipts tax is assessed on businesses and apply to business-to-business transactions in addition to final consumer purchases, leading to tax pyramiding.| Tax Foundation

Retail sales taxes are an essential part of most states’ revenue toolkits, responsible for 24 percent of combined state and local tax collections.| Tax Foundation

Retail sales taxes are an essential part of most states’ revenue toolkits, responsible for 32 percent of state tax collections and 13 percent of local tax collections (24 percent of combined collections).| Tax Foundation

Gov. Pillen is searching for tax burden relief. But his plan, which reportedly involves a two-tiered sales tax and the state’s assumption of most school funding responsibility, would have profound implications that even those most convinced of the urgency of property tax relief may find unworkable and unpalatable.| Tax Foundation

The Internal Revenue Service (IRS) is part of the U.S. Department of the Treasury and is responsible for enforcing and administering federal tax laws, processing tax returns, performing audits, and offering assistance for American taxpayers.| Tax Foundation

The home mortgage interest deduction currently allows itemizing homeowners to deduct mortgage interest paid on up to $750,000 worth of principal.| Tax Foundation