I’m fortunate enough to be participating in a lecture series at work that covers deep learning and its applications in finance. This will be a series of posts documenting what I learn and implementing the ‘homework’ (I’m 32, how am I still getting homework?) using Julia and Flux.| Dean Markwick

Crypto is making finance democratic. My PhD was originally going to be on the limit order book and modeling events that can change its state. However, I just couldn’t get the data. Now, anyone can access different exchanges limit orders books with simple API calls. My Julia package CoinbasePro.jl does exactly that and you can get full market data without even having to sign up.| Dean Markwick

QuestDB is a timeseries database that is well suited for financial data. It is built with timestamps in mind both when storing the data and also when getting the data out. This makes it the ideal candidate as a storage system for crypto trades.| Dean Markwick

A big part of market microstructure is price impact and understanding how you move the market every time you trade. In the simplest sense, every trade upends the supply and demand of an asset even for a tiny amount of time. The market responds to this change, then responds to the response, then responds to that response, etc. You get the idea. It’s a cascading effect of interactions between all the people in the market.| Dean Markwick

A new paper hit my feed Choosing trading strategies in electronic execution using importance sampling. I’ve only encountered sampling as part of a statistical computing course as part of my PhD, and I had never strayed away from Monte Carlo sampling, but this practical example provided an intuitive understanding of its importance and utility.| Dean Markwick

People are never short of a trade idea. There is a whole industry of researchers, salespeople and amateurs coming up with trading ideas and making big calls on what stock will go up, what country will cut interest rates and what the price of gold will do next. Alpha capture is about systematically assessing ideas and working out who has alpha and generates profitable ideas and who is just making it up as they are going along.| Dean Markwick

The Almgren Chris model from Optimal Execution of Portfolio Transactions is the most well known optimal execution model and provides the foundational math about how to think about trading some quantity of an asset. This blog post goes through the math and how we set the problem up and arrived at the various solutions.| Dean Markwick

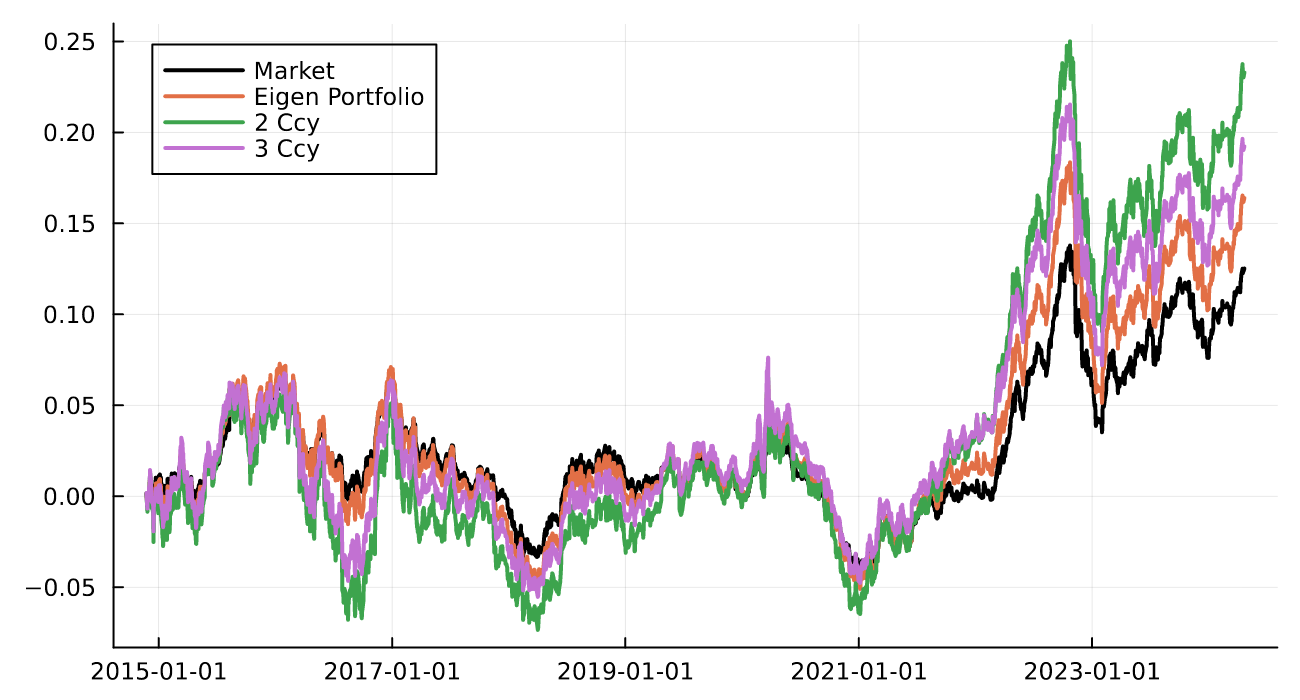

Principal component analysis (PCA) reduces a dataset to its main components. When we apply it to a dataset of different currencies it helps us understand how each currency drives the overall portfolio and what currency might be a common factor.| Dean Markwick

Read enough quant finance papers or books and you’ll come across the Ornstein–Uhlenbeck (OU) process. This is a post that explores the OU process, the equations, how we can simulate such a process and then estimate the parameters.| Dean Markwick

I recently listened to S7E3 of Flirting with Models which had Nick Baltas talking about Multi Asset and Multi-Strategy portfolios. Nick highlighted his work on cross-asset skew and how it can compliment your typical equity factors (momentum, growth, value etc.) and is an under-explored topic in portfolio construction. After reading the original paper, Cross-Asset Skew, I decided to try and replicate the results and see whether skew comes out in the wash and produces any alpha.| Dean Markwick

A good prediction model isn’t necessarily a good causal model. You could be missing a key variable in your dataset that is driving the underlying behavior so you end up with a good predictive model but not the correct explanation as to why things behave that way. Taking a causal approach is a tougher problem and needs an understanding of whether we have access to the right variables or we are making the right link between variables and an outcome. Causal regularisation is a method that uses...| Dean Markwick

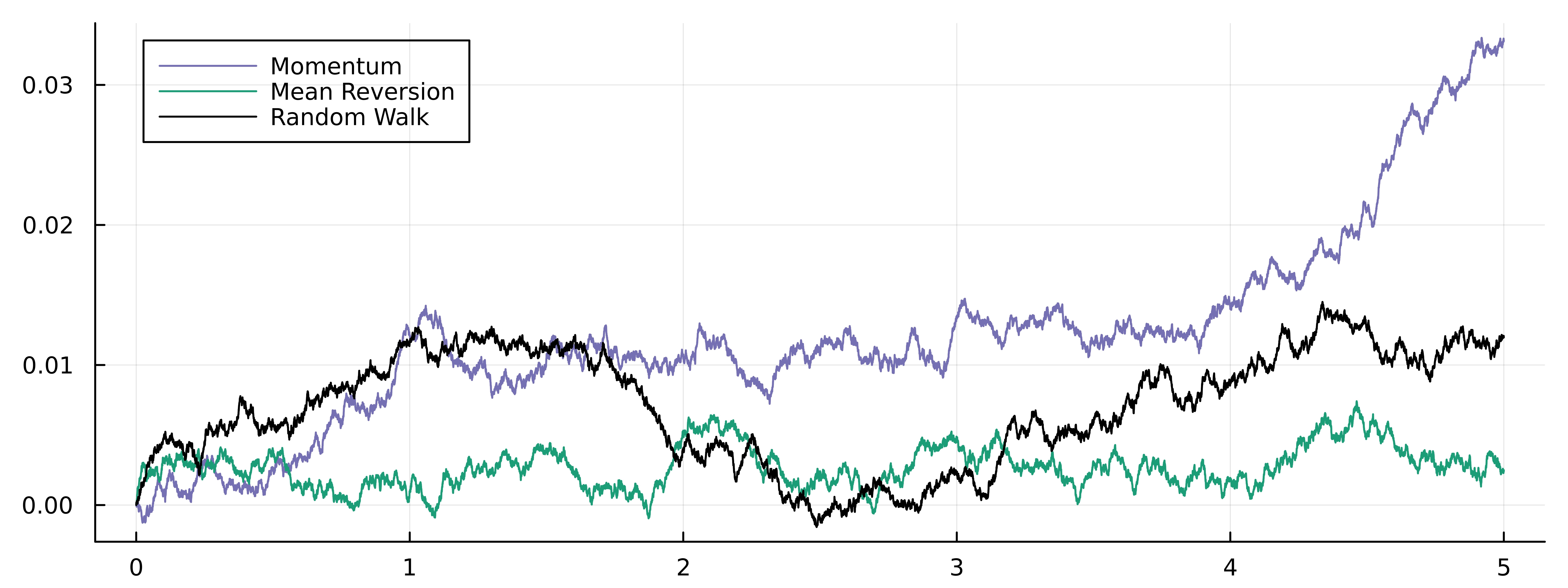

Statistical arbitrage (stat arb) is a pillar of quantitate trading that relies on mean reversion to predict the future returns of an asset. Mean reversion believes that if a stock has risen higher it’s more likely to revert in the short term which is the opposite of a momentum strategy that believes if a stock has been rising it will continue to rise. This blog post will walk you the ‘the’ statistical arbitrage paper Statistical Arbitrage in the US Equities Market apply it to a stock/ET...| Dean Markwick

Climbing Mount Everest is a true test of human endurance with a real risk of death. The Himalayan Database is a data repository, available for free, that records various details about the peaks, people, and expeditions to climb the different Nepalese Himalayan mountains and provides the data for this analysis. In this blog post, I’ll show you how to load the database and explore some of the features before building a model that tries to predict how you can successfully climb Mount Everest.| Dean Markwick

Golf became the only thing you could do in the COVID times and given my interest in sports modeling I made sure to start recording my scores and different stats about each of my rounds. This post outlines a specific model used in golf called Strokes Gained and relates the number of strokes required at a given distance to get the golf ball in the hole. It is a simple model but can describe someones golfing, or lack of in my case, ability.| Dean Markwick

Trend following is a rebranded name for momentum trading strategies. It looks at assets where the price has gone up and buying them because it believes the price will continue to rise and likewise for falling prices where it sells.| Dean Markwick