The concept of financial independence/retire early (FIRE) is all the rage in the personal finance space. The idea is to save a large percentage of your income (50% or more), live as frugally as possible, and retire in a short period of time while continuing to live frugally. Sometimes, fortunate young people with higher incomes can do this and retire in their 30's, and in some cases, their late 20's! In any case, the biggest concern with retiring early is running out of money. The earlier th...| Million Dollar Journey

Moving from the accumulation stage of my professional career, to withdrawing investments in early retirement was more difficult than I would have predicted a few years ago. For those who haven’t been following me since I started writing Million Dollar Journey back in 2005, I have slowly-but-surely detailed my rise from a very average net worth, to building an investment portfolio that allowed me to reach complete financial independence. Here are some of the key articles that I’ve written ...| Million Dollar Journey

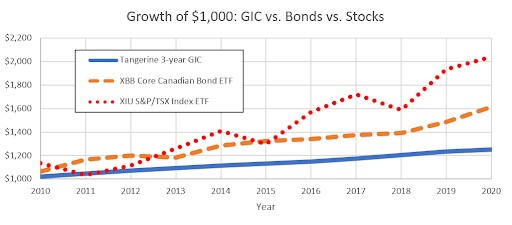

Most Canadians never stop to consider when low risk investments are the most appropriate use of savings versus when higher-risk long-term investments are the better route. The truth is that most Canadians choose their investment by “gut feel.” You likely don’t need me to tell you, that’s not an ideal process. When choosing between higher risk and low risk investments, it’s important to consider your personal goals and risk tolerance. Personally, I think that if you need your money i...| Million Dollar Journey

The concept of a safe withdrawal rate (and the 4% rule) is a key planning tool for Canadians of all ages. After all, if you don’t have a general withdrawal plan, how can you know how much you need to save in the first place? If you have been reading MDJ for years, you already have an idea of how to use a Canadian online broker account to DIY-invest your way to a solid nest egg. Now you’re planning for retirement (whether it’s 20+ years away or next year) and you’re wondering how to ...| Million Dollar Journey

Income splitting is a tax-saving strategy that divides a stream of income between family members (usually two spouses). The goal is to apportion as much of the higher-earning family member’s income to other family members, in an effort to get that higher-earning spouse into a lower tax bracket. Some economists and policy wonks have made the argument that income taxation should be applied to the family unit as a whole, and thus negate the need for fancy income splitting accounting altogether...| Million Dollar Journey

As a former teacher you might think I’d be the last person who would want to learn more about investing in annuities in Canada. But with Rob Carrick over at the Globe and Mail writing about how right now might be the best time to buy Canadian annuities for several years (maybe a decade-plus), I thought it would be be a good time to update our Ultimate Canadian Annuity Guide. Now, it’s common knowledge that teachers enjoy a solid stream of pension income when they reach retirement. In ...| Million Dollar Journey