Your data model is your destiny - Matt Brown's Notes

Your product's core abstractions determine whether new features compound into a moat or just add to a feature list. Here's how to get it right.| notes.mtb.xyz

Your product's core abstractions determine whether new features compound into a moat or just add to a feature list. Here's how to get it right.| notes.mtb.xyz

What do airline loyalty plans, tractor loans, and iPhone insurance tell us about the future of financial services and the evolving role of fintech in software?| notes.mtb.xyz

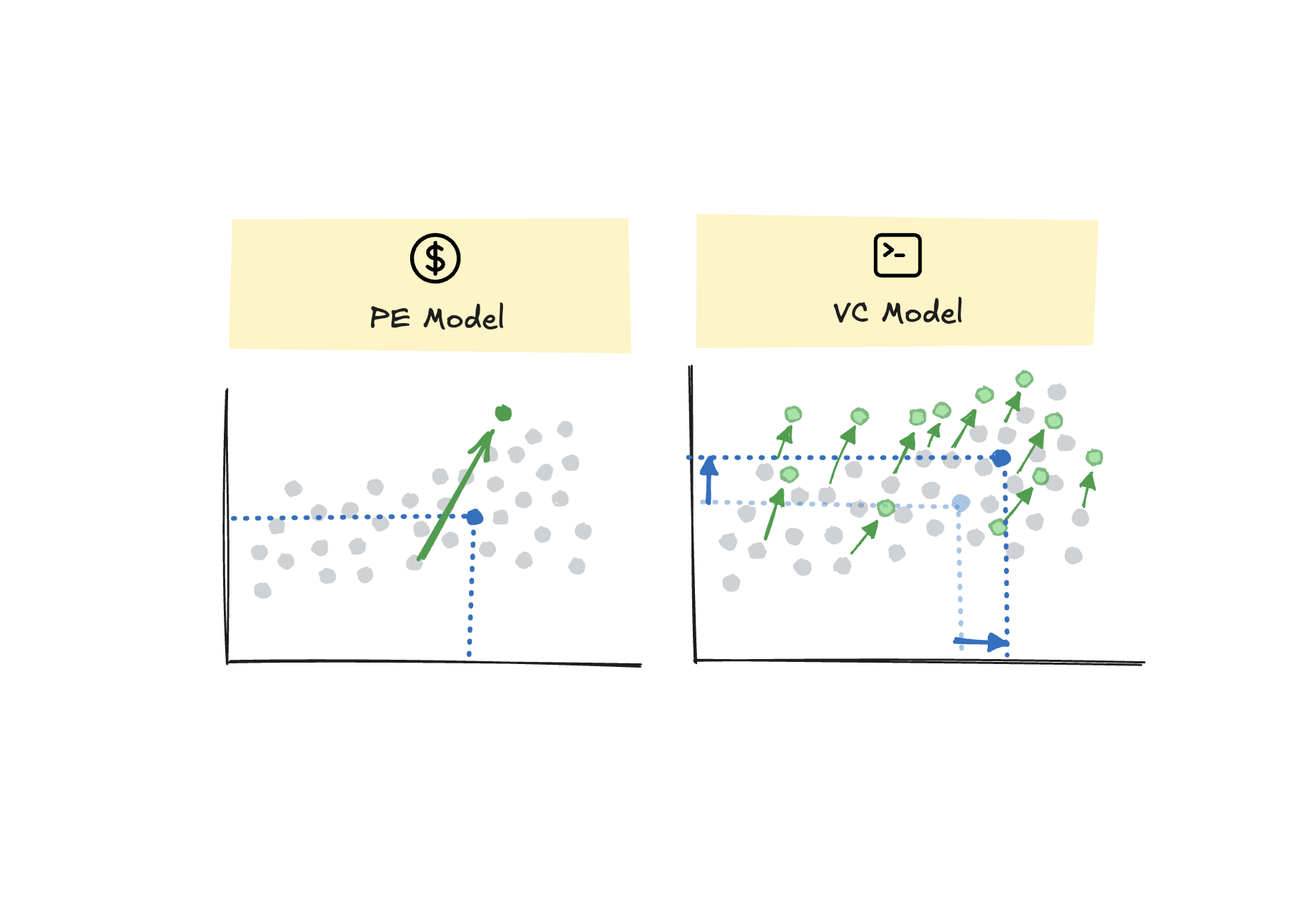

Gone are the days of minority investments in high-growth, asset-light, software-led startups. Why do so many VCs and VC-backed companies seem to be acting like PE firms these days?| Matt Brown's Notes

Payments are the secret weapon of the best vertical software companies. It’s not uncommon to see 2-5x increases in revenue, retention, and other metrics once a platform successfully embeds payments. It’s easier than ever to start with payments, but it’s more difficult than ever to succeed.| Matt Brown's Notes

A new community-driven list of 450+ vertical software companies, along with embedded financial products and other info, now available at verticalsoftware.fyi| Matt Brown's Notes

Why the canonical startup advice of "make something people want" doesn't apply to fintechs, who are ultimately in the business of pricing risk and "selling money".| Matt Brown's Notes

I’m excited to announce that I’ve led a $20M Series A investment into Rainforest on behalf of Matrix and joined the board. Rainforest enables software platforms to offer and monetize exceptional embedded payment experiences for end users. There’s a famous saying from the 2000s: "Advertising is the business model of the Internet.” In a few years, we’ll look back and say that| Matt Brown's Notes

Why open source is a powerful strategy — how to determine where open source is most and least effective — where open source is best suited in fintech| Matt Brown's Notes

On Toast's product and fintech strategy, how AI complements full stack products, trends in embedded fintech, and more| Matt Brown's Notes

How we describe something affects how we think about and interact with it. It's especially potent and dangerous in startup descriptions, and worth remembering for the companies building "with AI".| Matt Brown's Notes

Financial services is one of the oldest, largest, and most complex markets. “Oldest” is measured in millennia: the first coined currency is over 5,000 years old and many of the earliest written records are commercial in nature. “Largest” is measured in trillions: financial services has the largest gross profit pool of any major sector, 3.4x greater than ecommerce and 9.2x greater than software (see chart below).| Matt Brown's Notes

What matters in early-stage investing (and why I think "why now" is the most important thing).| notes.mtb.xyz

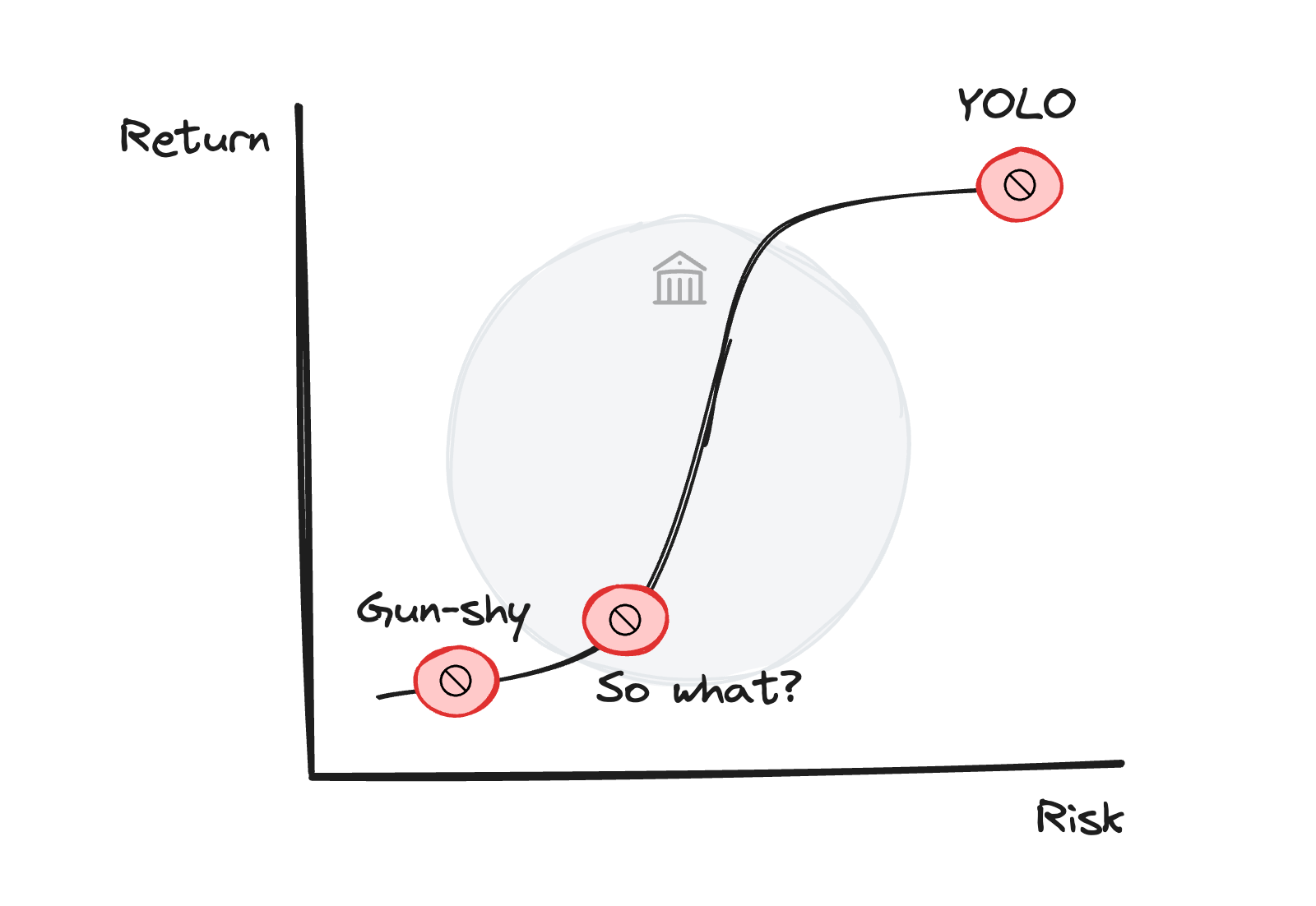

Fintech startups must grow fast but manage risk. Most fintechs get good enough it by limiting the downside of risk, but cap their upside in doing so. However, the best fintechs find ways to turn that risk into core IP and leverage for the business.| notes.mtb.xyz

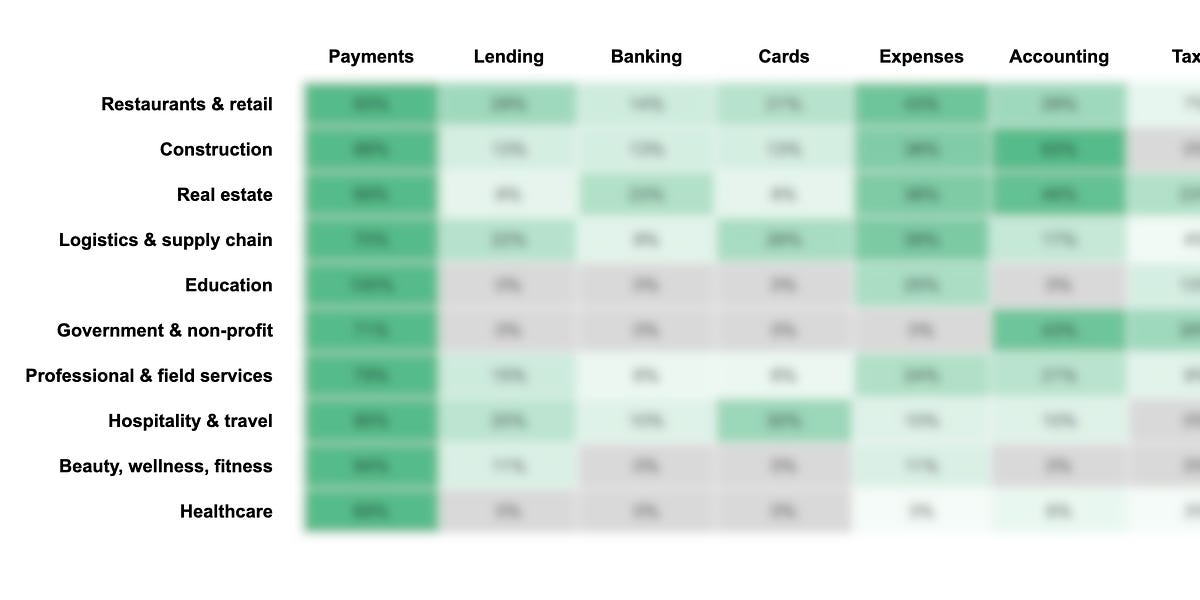

This is part 2 of a 3-part series on Vertical ERPs (VERPs).| notes.mtb.xyz

B2B payments is a ghost market because everyone focuses on the “payments” part. The real problem is in the workflows and data that precede the actual payment.| notes.mtb.xyz

Forget being dismissed as a ChatGPT wrapper. Anyone building vertical AI should fear being a wrapper around a system of record.| notes.mtb.xyz

Stablecoins are an exciting and powerful upgrade to financial technology, both in their own right and complementing traditional fiat money movement. This explains how stablecoins work, what they're used for, and how stablecoin businesses may evolve.| notes.mtb.xyz

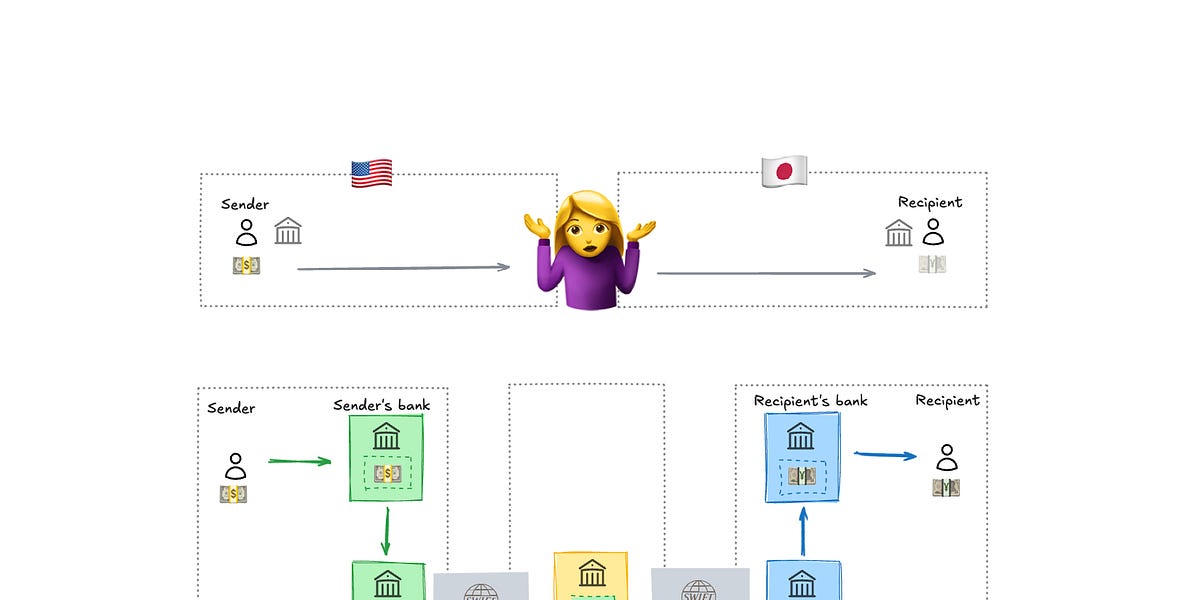

A gentle introduction to correspondent banking, money transmission, payment aggregation, and stablecoins, as well as cross-border payment business models and product strategies.| notes.mtb.xyz

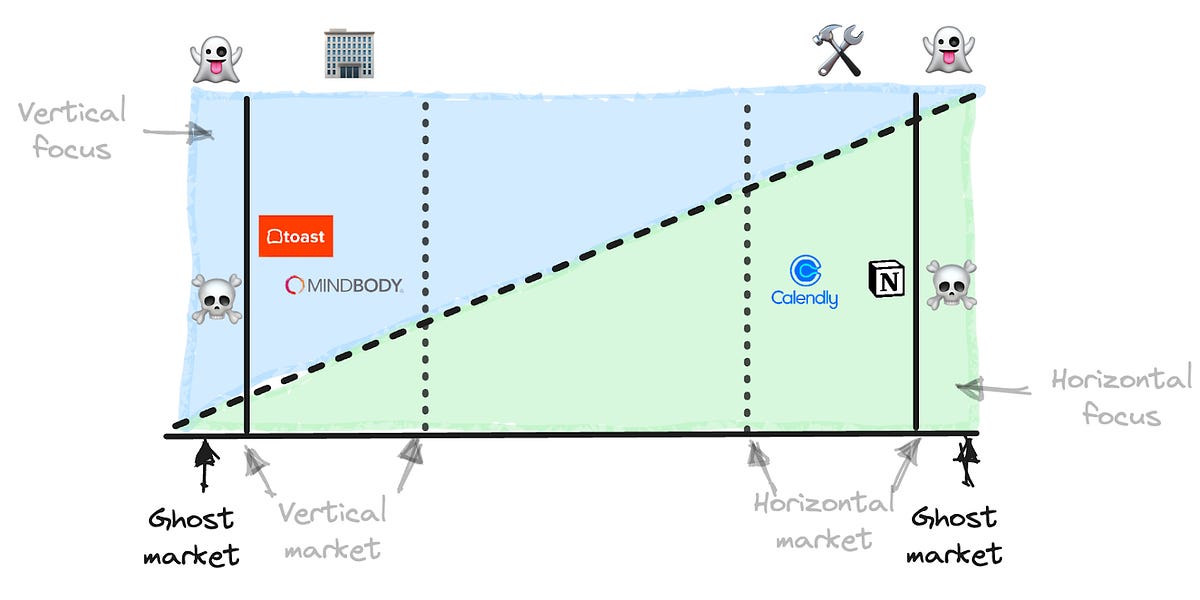

Vertical software is a great category to build and invest in. But the label and strategies behind it are quickly becoming irrelevant. The opportunity to build vertically focused companies is larger than ever, but the winners and their strategies won’t look like today’s vertical software.| notes.mtb.xyz

Real-time payments are a critical but often misunderstood trend in global payments. This note explains how they work, what catalyzed their recent growth, and why some networks are more successful than others.| notes.mtb.xyz

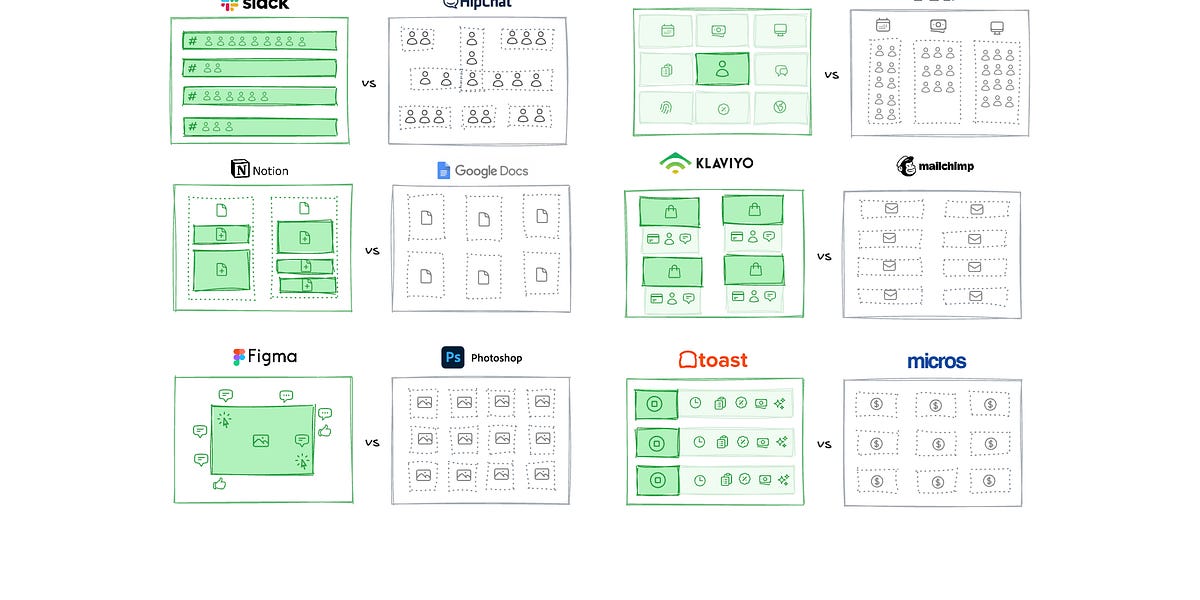

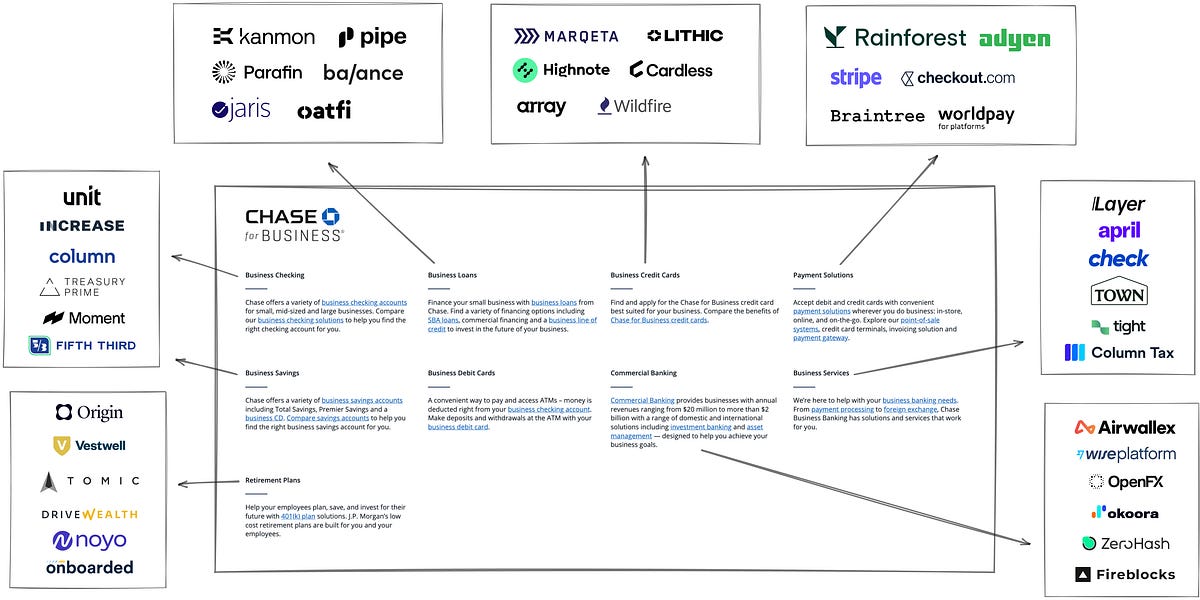

The two trends I’m most bullish on are vertical software and embedded fintech. Businesses of all sizes and industries rely heavily on software increasingly built for specific verticals. Within verticals, businesses increasingly prefer the convenience of integrated, all-in-one suites over multiple disconnected vendors. These software suites have started embedding financial products to provide more value, monetize at a higher rate, and increase customer retention.| notes.mtb.xyz

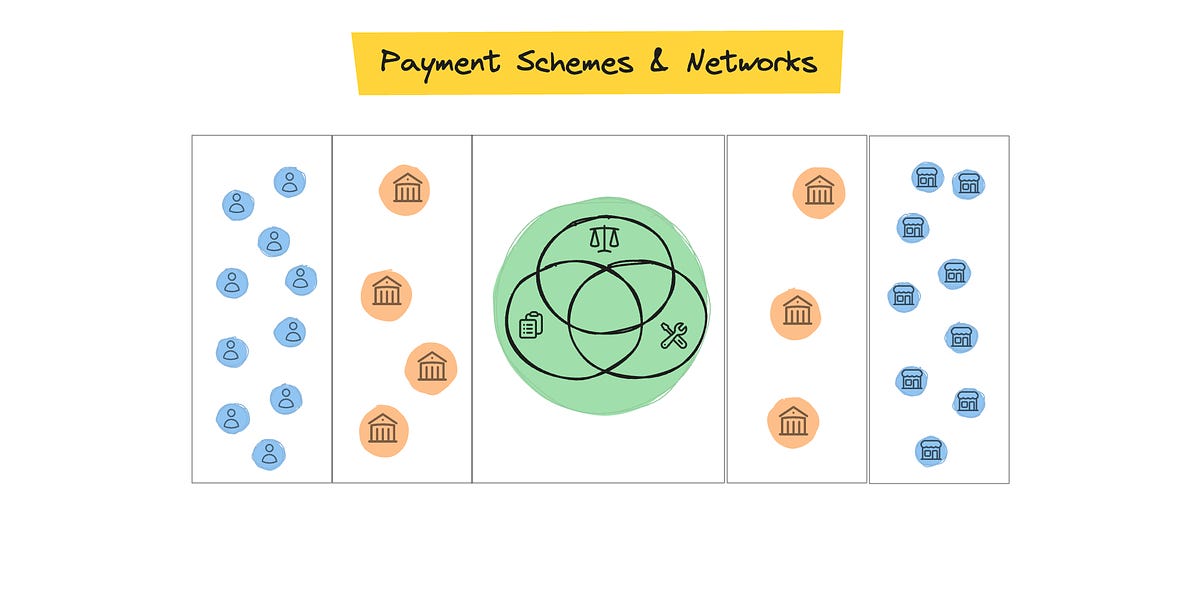

Payfac is the model behind fintech’s biggest successes, from Stripe and Square, to Shopify, Uber, and more. It's a critical but misunderstood topic, so here's an explainer in 1,000 words.| notes.mtb.xyz

How the SaaS and fintech models are breaking down, why food delivery and dark kitchens provide an alternative model, and what the future of software may look like as a result| notes.mtb.xyz

Ghost markets seem real. They have an enormous TAM and a clear need for new solutions. So a wave of companies go after the opportunity, and then… it vanishes into thin air.| notes.mtb.xyz

Fintech infra and embedded fintech are so unique that much of the generalist fundraising advice out there doesn't apply to them. Here's what I've learned from many pitches for infra opportunities.| notes.mtb.xyz

The next big fintechs will win with novel distribution, not novel products. In the 2010s the biggest fintechs were product innovators. They closed the gap between the poor UX of traditional financial institutions and the great UX of digital-first products. They combined new tech, regulatory frameworks, and business models to create genuinely novel products: Chime’s branchless bank, Robinhood’s fun fee-free trading, innovative consumer credit products like Earnin’s earned-wage-access or ...| notes.mtb.xyz

Interchange is a complex but critical topic for fintech operators.| notes.mtb.xyz

This is part 1 of a 3-part series on Vertical ERPs (VERPs).| notes.mtb.xyz